What is the Difference Between a Subsidized and Unsubsidized Loan?

Contents

If you’re considering taking out a student loan, you may be wondering what the difference is between a subsidized and unsubsidized loan. Here’s a quick rundown of the key differences between these two types of loans.

Checkout this video:

Subsidized Loans

A subsidized loan is a loan on which the interest is reduced by an explicit or hidden subsidy. In the context of student loans in the United States, the interest on a subsidized Stafford Loan is paid by the federal government while the student is enrolled in an eligible degree program and during authorized periods of deferment.

What is a subsidized loan?

A subsidized loan is a type of financial aid that is awarded to students who demonstrate a high financial need. These loans are offered by the federal government and they typically come with lower interest rates and more favorable repayment terms than other types of loans. Subsidized loans are also sometimes referred to as “need-based” loans.

To be eligible for a subsidized loan, you must first fill out the Free Application for Federal Student Aid (FAFSA). Once your financial need has been determined, you will be able to apply for a subsidized loan through the federal student loan program.

If you are approved for a subsidized loan, the federal government will pay the interest on your loan while you are in school and during any periods of deferment or forbearance. This can save you a significant amount of money over the life of your loan.

It’s important to note that not all students who demonstrate financial need will be approved for a subsidized loan. The amount of money that is available for these loans is limited, so it’s important to apply as early as possible.

How does a subsidized loan work?

A subsidized loan is a loan on which the interest is reduced by an explicit or hidden subsidy. The subsidized target group includes students, trainees, unemployed persons, and low-wage earners.[1] In the case of student loans in the United States, the interest rate may be as low as 3.4% per year,[2] which is substantially lower than the 6.8% rate for unsubsidized Stafford Loans for undergraduates.

In economics, a subsidy (also known as a subvention) is a benefit given by the government to groups or individuals in society to relieve them of some burden, often financial.

What are the benefits of a subsidized loan?

A subsidized loan is a federal student loan that offers a lower interest rate and monthly payments while you’re in school. You may also be able to get a subsidized loan if you can’t afford the payments on an unsubsidized loan. The main benefit of a subsidized loan is that you don’t have to pay any interest while you’re in school or during your grace period.

Unsubsidized Loans

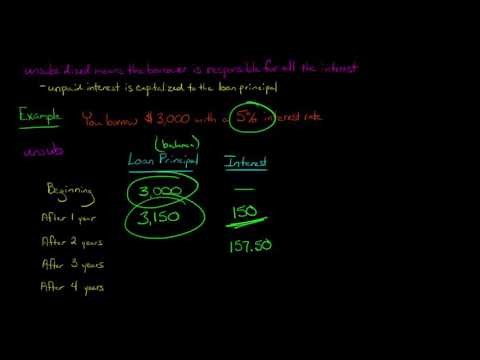

An unsubsidized loan is a loan that is not backed by the government. This means that the interest on the loan will accrue while you are in school and will be added to the principal balance of the loan. You are responsible for paying the interest on the loan while you are in school and during any periods of deferment or forbearance.

What is an unsubsidized loan?

An unsubsidized loan is a type of financial aid that you have to pay back. The US government does not pay the interest on your unsubsidized loan while you’re in school or during your grace period. That means the interest will start accruing (adding up) as soon as your loan is dispersed. You’ll owe that interest, along with the principal (the amount of money you borrowed).

How does an unsubsidized loan work?

The main difference between subsidized and unsubsidized loans is who pays the interest while the borrower is in school. With a subsidized loan, the federal government pays the interest while the borrower is in school. With an unsubsidized loan, the borrower is responsible for paying the interest while in school.

Unsubsidized loans are available to undergraduate and graduate students. The interest rate on unsubsidized loans for undergraduate students is 4.53% for the 2019-2020 school year. The interest rate on unsubsidized loans for graduate students is 6.08% for the 2019-2020 school year.

The annual loan limit for an unsubsidized loan is $20,500 for an undergraduate student and $40,500 for a graduate student (minus any subsidized loan amount). There is no limit on how much you can borrow in total with all types of federal student loans.

What are the benefits of an unsubsidized loan?

There are two main types of federal student loans: subsidized and unsubsidized. Subsidized loans are need-based, meaning that the government pays the interest on the loan while you are in school. Unsubsidized loans are not need-based, so the borrower is responsible for the interest from the time the loan is taken out.

There are several benefits to taking out an unsubsidized loan:

-You may be eligible for a larger loan amount than with a subsidized loan.

-You are not required to demonstrate financial need in order to qualify.

-The interest on your loan will accrue (accumulate) during all periods, including during deferment and forbearance. However, you can choose to pay the interest as it accrues, or you can allow it to be capitalized (added to your principal balance).