What Does an Unsubsidized Loan Mean?

Contents

You’re not alone in wondering, “What does an unsubsidized loan mean?” We’ve got the answer, plus information on subsidized loans and how they can save you money.

Checkout this video:

Introduction

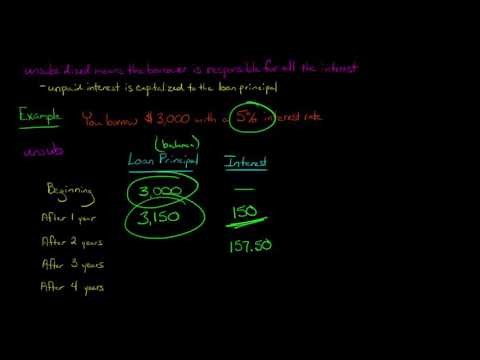

Simply put, an unsubsidized loan is a loan where the borrower is responsible for paying all the interest that accrues on the loan. Most loans are subsidized, which means that the government pays the interest while the borrower is in school and during grace periods and deferment or forbearance periods.

With an unsubsidized loan, the interest starts accruing as soon as the loan is taken out, and it will continue to accrue even if you defer payments. This can make unsubsidized loans more expensive in the long run than subsidized loans, since you’ll end up paying more in interest.

If you have the option of taking out a subsidized or unsubsidized loan, you should always choose the subsidized loan first. If you can’t get a subsidized loan or you need to borrow more money than the maximum amount of a subsidized loan, then you can look into taking out an unsubsidized loan.

What is an Unsubsidized Loan?

An unsubsidized loan is a type of financial aid that is not awarded based on financial need. Instead, the loan is available to any eligible student, and the student is responsible for all interest that accrues on the loan. Unsubsidized loans are sometimes called “self-help” loans because the student must help him or herself by paying the interest while in school.

The federal government offers unsubsidized loans through the Direct Loan Program. The amount you can borrow each year depends on your grade level and whether you are a dependent or independent student. Independent students and students in graduate or professional degree programs can borrow more each year than undergraduates.

If you have questions about unsubsidized loans or need help understanding your options, contact the financial aid office at your school.

How Unsubsidized Loans Work

An unsubsidized loan is a type of financial aid that you have to pay back with interest. The government does not pay the interest for you while you’re in school.

Unsubsidized loans are available to undergraduate and graduate students. The interest rate is fixed and usually lower than the rate on a credit card. You don’t have to start paying the loan back until after you graduate or leave school.

The amount you can borrow depends on your year in school and other financial aid you’re receiving.

If you have any questions, contact the financial aid office at your school.

Interest Rates

Loans that are not subsidized by the government accrue interest from the day they are dispersed until they are paid in full. The government does not pay the interest on unsubsidized loans while the student is enrolled in school at least half-time, during their grace period, or during deferment periods. Interest that accrues during these times will be added to the principal balance of the loan, causing the total amount you have to repay to increase.

Repayment

Repayment of a subsidized loan begins 6 months after the student graduates, withdraws from school, or drops below half-time enrollment. The repayment period for a subsidized loan may not exceed 10 years.

Interest on an unsubsidized loan accrues (accumulates) from the time the loan is disbursed until it is paid in full. The interest rate is variable and will change on July 1st of each year. The borrower may pay the interest while in school and during periods of deferment or forbearance, or may allow the interest to accrue and be capitalized (added to the principal amount of the loan). Capitalization increases the total amount you have to repay because you will be paying interest on the interest that has accumulated.

Pros and Cons of Unsubsidized Loans

There are some major benefits to taking out an unsubsidized loan, including the fact that you don’t have to pay any interest on the loan until you actually start repaying it. This can be a huge advantage if you expect to be in a position where you can pay off the loan relatively quickly.

Another big benefit of an unsubsidized loan is that you don’t have to demonstrate financial need in order to qualify for the loan. This means that more people will be eligible for unsubsidized loans than for other types of loans, such as subsidized loans.

Of course, there are also some drawbacks to taking out an unsubsidized loan. One of the biggest drawbacks is that you will accrue interest on the loan from the day that it is disbursed. This means that your total repayment amount will be significantly higher than the original amount of the loan.

Another potential downside of an unsubsidized loan is that you may have to pay origination fees. These fees can add up, and they can end up increasing your total repayment amount by a significant amount.

Conclusion

In conclusion, an unsubsidized loan is a loan that is not backed by the government and therefore has a higher interest rate. These loans are often used by students who are not eligible for government loans or who need to borrow more money than the government limit. Unsubsidized loans can be a good option for students who need extra money for college, but it’s important to remember that the interest on these loans will accrue while you are in school. If you can, try to get a subsidized loan first and then supplement with an unsubsidized loan if you need to.