How to Calculate the Employee Retention Credit

Contents

The Employee Retention Credit is a refundable tax credit for eligible employers that retain their employees during the COVID-19 pandemic.

Checkout this video:

What is the Employee Retention Credit?

The Employee Retention Credit (ERC) is a refundable tax credit for eligible employers that retain their employees during the COVID-19 pandemic. The credit is available to employers whose operations have been fully or partially suspended as a result of a governmental order related to COVID-19, or who have experienced a significant decline in gross receipts. Employers are eligible for the credit if they maintain their payroll during the pandemic.

To calculate the employee retention credit, you will need to determine your average number of full-time equivalent employees (FTEs) for 2019 and your payroll costs for 2020. Your payroll costs include wages paid to employees, as well as the cost of health insurance premiums paid by the employer on behalf of employees. Once you have determined your eligibility and calculated your employee retention credit, you can claim the credit on your quarterly employment tax return or annual income tax return.

How do you calculate the Employee Retention Credit?

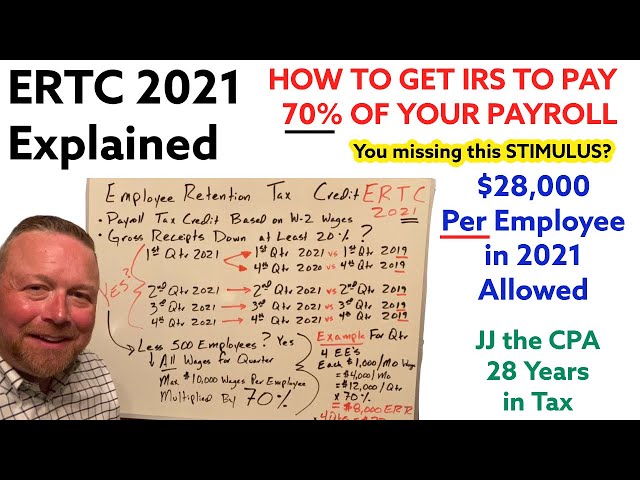

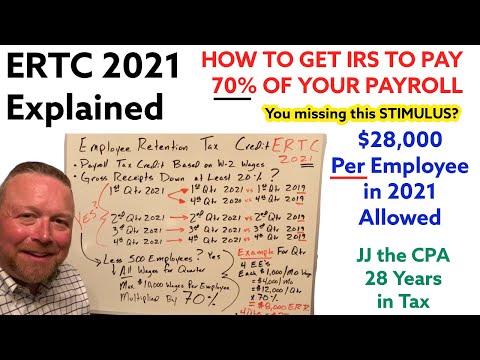

The Employee Retention Credit is a fully refundable tax credit for eligible employers equal to 50% of qualified wages (including allocable qualified health plan expenses) that Eligible Employers pay their employees.

To calculate the credit, you will need to determine your eligible wage base for each employee. The maximum wage base for each employee is $10,000 ($21,000 for an employee who is treated as family for purposes of the earned income tax credit), per calendar quarter. The credit is capped at $5,000 per employee ($10,000 per family member).

If you have 100 or fewer full-time equivalent employees (FTEs), all of your eligible wages (up to the $10,000 per-employee quarterly limit) are qualified wages. If you have more than 100 FTEs, only the first $10,000 of eligible wages paid to each employee during each calendar quarter are qualified wages.

Qualified Wages = (Number of Employees x $10,000 Limit) / 2 {if number of employees > 100}

OR

Qualified Wages = Number of Employees x $10,000 Limit {if number of employees <= 100}

https://www.irs.gov/credits-deductions/businesses/ employee-retention-credit

What are the rules for the Employee Retention Credit?

To be eligible for the Employee Retention Credit, businesses must have:

-Experienced either a full or partial shutdown due to a COVID-19 related Directive from a governmental authority OR

-Experienced a significant decline in gross receipts when comparing 2020 quarterly receipts to 2019 quarterly receipts. A significant decline is defined as follows:

-For corporations and employers who filed Form 941 for the second quarter of 2019, gross receipts in any 2020 calendar quarter are less than 80% of the comparable 2019 calendar quarter.

-For all other employers, including those who did not file Form 941 for the second quarter of 2019, gross receipts in any 2020 calendar quarter are less than 50% of the comparable 2019 calendar quarter.

How do you claim the Employee Retention Credit?

The credit is claimed on Form 941, Employer’s Quarterly Federal Tax Return, for each quarter in which the employer pays qualifying wages. An eligible employer must decreased its gross receipts by more than 50% when comparing the first quarter of 2020 with the first quarter of 2019 to be eligible for the credit. If a seasonal employer’s gross receipts vary by more than 20 percentage points between any two of its consecutive tax quarters, it may elect to compare its gross receipts for a different quarter.

Employers will use their average number of employees in 2019 to determine if they are an eligible small or large employer. A small employer is one that averaged less than 500 employees in 2019. A large employer is one that averaged more than 500 employees in 2019. Once an employer determines whether it is small or large, this designation applies for each subsequent quarter for which the credit is claimed.

For employers that were not in business during all of 2019, their average number of employees during 2020 will be used to determine whether they are a small or large employer.

If an eligible employer received a Paycheck Protection Program loan, it can still claim the Employee Retention Credit for any qualifying wages paid after the PPP loan was forgiven (or after December 31, 2020 if it does not apply for forgiveness).