Why Is My FICO Score Lower Than My Credit Score?

Contents

If you’re wondering why your FICO score is lower than your credit score, it’s likely because they’re calculated differently. Here’s a look at how each score is determined and why your FICO score may be lower than your credit score.

Checkout this video:

FICO Score vs. Credit Score

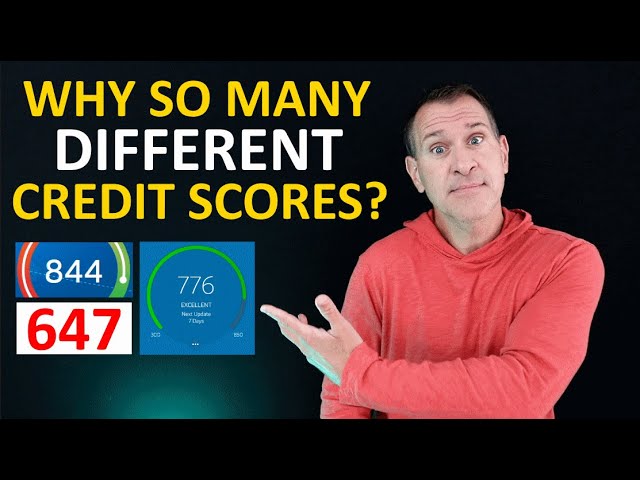

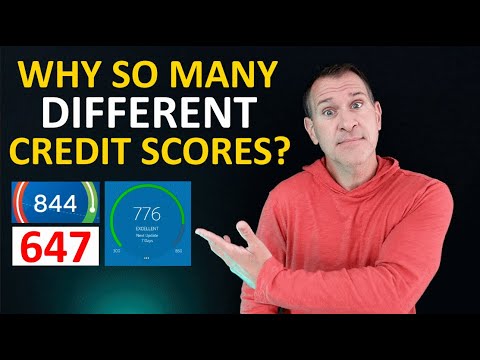

When you’re trying to get a handle on your credit health, you’ll come across two different numbers: your FICO score and your credit score. Though they both relate to your creditworthiness, these numbers are not the same. So why is your FICO score lower than your credit score?

What is a FICO score?

Your FICO score is a three-digit number that lenders use to decide whether or not to give you a loan and what interest rate to charge you.

FICO scores range from 300 to 850, and the higher your score, the better. A high FICO score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan. A low FICO score indicates you’re a high-risk borrower, which could lead to a higher interest rate and possibly being denied for a loan altogether.

There are many factors that go into your FICO score, including your payment history, credit utilization, length of credit history, types of credit accounts, and inquiries for new credit.

You have more than one FICO score because there are multiple versions of the FICO scoring model — each with its own scoring range. The most commonly used FICO scores are:

-FICO Score 8: Ranges from 300-850

-FICO Score 9: Ranges from 300-850

-Banked on FICO Score 2: Ranges from 250-900

-Industry Specific FICOs: Ranges vary depending on the industry (auto loans, credit cards, etc.)

What is a credit score?

A credit score is a number that lenders use to decide whether or not to lend you money. It is based on your credit history, which is a record of how you have handled borrowing and repayment in the past. The higher your score, the more likely you are to be approved for a loan or credit card. The lower your score, the less likely you are to be approved.

Your credit score is not the same as your FICO score. Your FICO score is a specific type of credit score that is used by many lenders. It is calculated using information from your credit report, but it is not the only type of credit score available. There are other companies that create their owncredit scores, and each one uses different criteria.

The Difference Between FICO Score and Credit Score

Your FICO score and credit score are two different things. Your FICO score is a number that is used by lenders to decide whether or not to give you a loan. Your credit score is a number that is used by lenders to decide how much interest to charge you on a loan.

FICO score is based on credit report data

Your FICO score is a specific number that’s calculated based on the information in your credit report. Because the data in your report can change over time, so can your score. Credit scores are ranges (for example, 750-850) and not specific numbers like FICO scores.

Here are a few key things to know about your FICO score:

-It’s based on the information in your credit report at the time it’s requested.

-It’s a snapshot in time, so it may change as your credit report changes.

-Your score may be different from one credit scoring company to another.

-You have multiple FICO scores, which may be different depending on which type of credit scoring company requests it and what type of lending you’re doing (for example, auto lending or credit card lending).

Credit score is based on credit utilization

A FICO score is a type of credit score that is used by lenders to help them determine whether or not you are a good candidate for a loan.

A credit score is a number that represents your creditworthiness. It is based on your credit history, which is a record of your ability to repay debts.

Your credit utilization ratio is the amount of debt that you have compared to the amount of credit that is available to you. This ratio is one factor that is used to calculate your credit score.

If you have a lot of debt and a low credit score, your lender may consider you to be a high-risk borrower and may be less likely to give you a loan.

The Importance of FICO Score

FICO score is a measure of credit risk, and it’s important to know your FICO score if you’re planning to apply for a loan or credit card. A FICO score is calculated using information from your credit report, and it’s the most widely used credit score. A FICO score of 750 or above is considered excellent, and a score of 700 to 749 is considered good.

FICO score is used by lenders to determine creditworthiness

Your FICO score is the most important factor when it comes to getting approved for a loan or credit card. This three-digit number is used by lenders to determine your creditworthiness — in other words, how likely you are to repay a loan on time. A higher score means you’re a lower risk, which could lead to a lower interest rate on a loan.

What’s in a FICO Score?

Your FICO score is based on the information in your credit report, including:

-Payment history (35%)

-Amounts owed (30%)

-Length of credit history (15%)

-Credit mix (10%)

-New credit (10%)

Credit score is used by lenders to determine interest rates

Your FICO score is important because it is used by lenders to determine the interest rate you will pay on a loan. A higher score means you will pay a lower interest rate, and a lower score means you will pay a higher interest rate.

For example, let’s say you have a credit score of 780 and you are applying for a 30-year fixed-rate mortgage. Based on the national average mortgage rate, you would qualify for a 4.176% interest rate. But if your credit score was just 720, your interest rate would jump to 4.648%. That may not seem like much, but over the life of the loan, it could cost you more than $21,000 in additional interest!

Your FICO score is also important because it is used by lenders to determine whether or not you will be approved for a loan. In general, the higher your score, the better your chances of being approved for a loan with favorable terms (such as a low interest rate).

So why is your FICO score sometimes lower than your credit score? The answer has to do with the way that FICO scores are calculated. While we don’t know all of the details (FICO scores are developed by Fair Isaac Corporation and they keep their formula secret), we do know that FICO scores focus on five main factors:

-Payment history (35%)- Do you pay your bills on time?

-Amounts owed (30%) – How much debt do you owe?

-Length of credit history (15%) – How long have you been using credit?

-Credit mix (10%) – Do you have a mix of different types of credit accounts?

-New credit (10%) – Have you opened any new credit accounts recently?

As you can see, payment history is the most important factor in calculating your FICO score. So if you have missed any payments or made late payments, that will lower your score. Additionally, if you have any collection accounts or charge-offs, that can also drag down your score.

How to Improve Your FICO Score

Your FICO score is a important number that potential lenders look at when considering you for a loan. A low FICO score could lead to you being denied for a loan or could lead to you paying a higher interest rate. There are a few things you can do to help improve your FICO score.

Check your credit report for errors

One of the most common reasons for a lower-than-expected FICO® Score is an error on your credit report. According to a study by the Federal Trade Commission, about one in four consumers had an error on one of their credit reports.

You can check your credit report for free once a year from each of the three major credit reporting agencies—Equifax, Experian and TransUnion—at www.annualcreditreport.com. If you find an error, you can file a dispute with the credit reporting agency and the creditor. (You can also file a dispute directly with the creditor, but it may be easier to go through the credit reporting agency.)

Pay your bills on time

One of the most important things you can do to improve your credit score is to pay all your bills on time, every time.

Your payment history is the record of how often you’ve made your payments on time, and is one of the most important factors in determining your credit score. Payment history makes up 35% of your FICO® Score, so even if you have a low credit limit and carry a high balance, if you always make your payments on time, you could still have a good credit score.

Keep your credit utilization low

One factor that influences your FICO® Score is your credit utilization ratio—the amount of revolving credit you’re using divided by the total amount of revolving credit available to you. To calculate your credit utilization ratio, divide your outstanding balances by your credit limits. The lower your credit utilization ratio, the better for your score.

If you have multiple revolving accounts, like credit cards, the balances and credit limits on all those accounts are used to calculate your total credit utilization. So if you’re trying to improve your score, one strategy is to bring down the balances on all your revolving accounts—not just one account.

And don’t close unused cards thinking it will help your score. It could actually hurt it because that would increase your overall credit utilization ratio.