When Does Student Loan Interest Start Accruing?

Contents

If you’re wondering when student loan interest starts accruing, the answer is typically after you graduate or drop below half-time enrollment.

Checkout this video:

Federal Student Loans

There are two types of federal student loans: subsidized and unsubsidized. Subsidized loans are need-based, meaning the government pays the interest while you’re in school at least half-time, during your grace period, and during any deferment periods.

Direct Subsidized Loans

Direct Subsidized Loans are low-interest loans for eligible students with financial need. As of July 1, 2012, first-time borrowers will have the interest on their Subsidized Loans deferred while they are making payments on time and are enrolled at least half-time in an eligible program. For these first-time borrowers, the no interest accrual period will be limited to 150% of the length of their program. This means that if you enroll in a four-year program, your grace period would extend for six years (4 x 150% = 6).

Direct Unsubsidized Loans

Direct Unsubsidized Loans are student loans available to undergraduate and graduate students. The U.S. Department of Education is the lender for these loans.

With a Direct Unsubsidized Loan, you’re responsible for paying the interest that accrues on your loan while you’re in school and during grace periods and deferment or forbearance periods. If you choose not to pay the interest while you’re in school and during grace periods and deferment or forbearance periods, your interest will accrue (accumulate) and be capitalized (that is, added to the principal amount of your loan).

Direct PLUS Loans

Direct PLUS Loans are federal student loans that graduate and professional students and parents of dependent undergraduate students can use to help pay for college or career school. PLUS loans can help pay for education expenses not covered by other financial aid.

The U.S. Department of Education (ED) makes Direct PLUS Loans to eligible borrowers through schools participating in the Direct Loan Program. Only the borrower may receive Direct PLUS Loans; they cannot be made to pay for someone else’s education expenses.

To get a Direct PLUS Loan, you must complete a Free Application for Federal Student Aid (FAFSA®) form and then sign a Master Promissory Note (MPN).

Private Student Loans

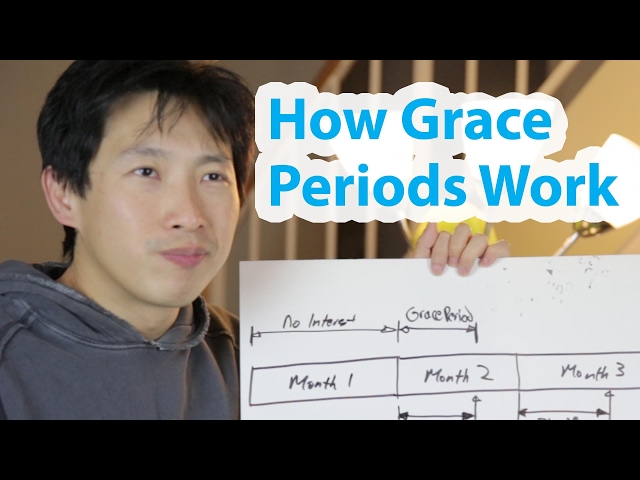

Most private student loans have a grace period of six months after you graduate, leave school, or drop below half-time enrollment before interest starts accruing. This means that if you take out a private student loan on June 1st, your first interest payment will likely be due on December 1st.

Fixed-rate private student loans

Fixed-rate private student loans offer borrowers the same interest rate for the life of their loan. So, if you have a fixed-rate loan with an interest rate of 6%, your rate will still be 6% when you make your last payment, even if rates have increased in the meantime. A fixed interest rate can offer peace of mind, since you’ll know exactly how much your loan will cost over time. And, since private student loan rates are often lower than variable rates, a fixed-rate loan could save you money in the long run.

Variable-rate private student loans

Variable-rate private student loans have interest rates that can change during the life of the loan. The monthly payments on these loans can also increase or decrease, depending on the interest rate.

Most variable-rate private student loans have a limit, or “cap,” on how high the interest rate can go. For example, a loan with a 5% interest rate cap would have a maximum interest rate of 10%.

The advantage of a variable-rate loan is that the interest rate may go down over time. The disadvantage is that the monthly payments could increase if the interest rate goes up.

Student Loan Interest Rates

The interest on your student loans can start accruing as soon as your grace period ends. This means that if you do not start making payments on your loans, the interest will continue to grow and be added to your loan balance. The interest rate on your student loans will depend on the type of loan you have and when you took it out.

Federal student loan interest rates

Interest rates for federal student loans are set by Congress and typically adjust every year on July 1. Your interest rate won’t change for the life of your loan, so it’s important to understand how it’s determined when you first take out your loan.

Federal student loan interest rates for undergraduates is set at 4.53% for the 2019-2020 school year.

The interest rate for Direct Unsubsidized Loans and Direct PLUS Loans first disbursed on or after July 1, 2018 and before July 1, 2019 is 7.08%.

Private student loan interest rates depend on many factors, including:

-Your credit score and history

-The type of loan you choose

-The length of your repayment term

-The current market conditions

Private student loan interest rates

Interest rates on private student loans tend to be higher than on federal student loans. The average interest rate for the 2018-2019 school year was 4.53% for private student loans, according to private lender Sallie Mae.

That’s higher than the average interest rate of 5.05% for federal student loans for undergraduates during the same time period.

Federal student loan rates are set by Congress and don’t change from year to year. Private student loan rates are set by individual lenders, so they can vary widely.

When you’re shopping around for a private student loan, it’s important to compare interest rates as well as other factors such as repayment terms and fees.

When Does Student Loan Interest Start Accruing?

Student loan interest typically starts accruing after you leave college or university and enter repayment. This means that if you have a six-month grace period after graduation, you may not have to start making payments until six months after you leave school. However, interest will begin to accrue during that grace period.

Federal student loans

Federal student loans don’t accrue interest while you’re in school at least half-time, during your grace period, or during certain types of deferment. Your grace period is a set amount of time after you graduate, leave school, or drop below half-time enrollment when you’re not required to make payments on your loan. After your grace period ends, your loan enters repayment.

Most federal student loans have a fixed interest rate, which means that the rate won’t change over the life of your loan. The only exception is federal Perkins Loans, which have a variable interest rate that’s set annually.

The following table shows the maximum fixed interest rates for Direct Subsidized Loans and Direct Unsubsidized Loans first disbursed on or after July 1, 2019, and before July 1, 2020. These rates will remain in effect through June 30, 2020:

Direct Subsidized Loans and Direct Unsubsidized Loans

Borrower type Fixed interest rate Maximum fixed interest rate

Undergraduate 4.53% 8.08%

Private student loans

Interest on private student loans starts accruing immediately after the loan is disbursed. Most private student loans have a grace period of six months, meaning that you won’t have to start making payments until six months after you graduate (or drop below half-time enrollment). Some private student loans, however, do not have a grace period. This means that you will have to start making payments as soon as the loan is disbursed.