What Percent of Your Credit Should You Use?

When it comes to credit utilization, there’s no one-size-fits-all answer. But there are some general guidelines you can follow to help you figure out what’s right for you.

Checkout this video:

The 30% Rule

What is the 30% rule?

The 30% rule is a general guideline that financial experts recommend for optimal credit health. It says that you should keep your balance at or below 30% of your credit limit on all of your accounts.

The 30% rule isn’t a hard-and-fast rule, and there’s some debate about whether it’s the best way to manage your credit. But it’s a good starting point, and it can help you stay within your credit limits and keep your balances manageable.

There are a few things to keep in mind if you’re trying to follow the 30% rule. First, it’s important to pay attention to all of your credit accounts, not just your major accounts like your mortgage or auto loan. Second, remember that your credit utilization is calculated based on the balances reported to the credit bureaus, so it’s important to keep an eye on those balances and make sure they’re reported accurately. Finally, keep in mind that your credit utilization can fluctuate month-to-month, so don’t panic if you see a higher balance one month – as long as you keep it under control overall, you should be fine.

How does the 30% rule impact your credit score?

The 30% rule is a guideline recommendation for how much of your credit limit you should use at any given time. The general rule of thumb is to keep your credit utilization at or below 30%. This means if you have a credit limit of $1,000, you should keep your balance at or below $300 (30% x $1,000 = $300).

There are a few different ways that the 30% rule can impact your credit score. First, it can help you keep your balances low. This is important because one of the factors that goes into your credit score is credit utilization. Credit utilization is the amount of debt you have compared to your credit limits. So, if you have a high balance and low credit limits, your credit utilization will be high. Conversely, if you have low balances and high credit limits, your credit utilization will be low. Keeping your balances low relative to your credit limits will help keep your credit utilization low, which in turn will help support a good credit score.

Second, the 30% rule can help you avoid getting penalized for making multiple inquiries on your credit report within a short period of time. When lenders make inquiries on your report, it can temporarily ding your score. But if those inquiries are spread out over time and make up less than 30% of new activity on your report, they shouldn’t have a significant impact on your score. So following the 30% rule can help protect against any short-termScore decreases from multiple inquiries.

In general, following the 30% rule is a good way to keep both balances and inquiries low on your report, which can in turn help support a good credit score.

The 10% Rule

What is the 10% rule?

The 10% rule is a guideline that suggests you should only use 10% of your credit limit at any given time. This rule is designed to help you keep your credit utilization low, which can have a positive impact on your credit scores.

While there is no hard and fast rule about what percentage of your credit you should use, the 10% rule is a good general guideline. By keeping your usage below 10%, you’re likely to keep your credit utilization low, which can have a positive impact on your credit scores.

There are a few things to keep in mind if you’re trying to follow the 10% rule:

1. Your credit limit may fluctuate over time. If your limit goes up, you’ll need to adjust your spending accordingly.

2. You may not be able to avoid using more than 10% of your credit if you have a large purchase to make or an emergency expense. In these cases, it’s best to pay off your balance as soon as possible to get back below the 10% threshold.

3. Some experts recommend using even less than 10% of your credit limit, so feel free to adjust the rule based on what makes sense for you and your financial goals.

How does the 10% rule impact your credit score?

Most people know that using more than 30% of your credit limit can have a negative impact on your credit score. However, you may not be aware of the 10% rule.

This rule states that if you use more than 10% of your available credit, it will have a negative impact on your score. This is because it shows lenders that you are maxing out your cards and may not be able to make payments in the future.

If you keep your balances below 10%, it will show lenders that you are a responsible borrower and are less likely to default on your loans. This can help to improve your credit score and make it easier to get approved for loans in the future.

The 2% Rule

You’ve probably heard the advice to keep your credit utilization low. This means that you shouldn’t be using a large portion of your credit line. So, how much of your credit should you actually use? The answer is the “2% rule.”

What is the 2% rule?

The 2% rule is a general guideline for how much of your credit you should use at any given time. Essentially, you should try to keep your balances at or below 2% of your credit limit. So, if you have a credit limit of $1,000, you would want to keep your balance below $20.

There are a few reasons why this is a good rule of thumb. First, it help you avoid going over your credit limit, which can result in fees and damage your credit score. Second, keeping your balances low can help improve your credit utilization ratio, which is another important factor in your credit score.

Of course, there may be times when you need to use more than 2% of your credit, and that’s OK. Just be sure to pay off the balance as soon as possible to avoid paying interest and damaging your credit score.

How does the 2% rule impact your credit score?

The two percent rule is a guideline often cited by financial experts when it comes to managing credit card debt. The rule states that you should never charge more than 2% of your credit limit on any given credit card in a single billing cycle. So, if you have a credit card with a $1,000 limit, you should never charge more than $20 in a single billing cycle.

There are a few different schools of thought on why the 2% rule exists, but the most common reason given is that it helps keep your credit utilization low. Credit utilization is one of the most important factors in your credit score, so by following the 2% rule, you can help keep your score high.

Of course, there are always exceptions to the rule – if you know you can pay off your balance in full and on time, then charging more than 2% of your limit shouldn’t impact your score too negatively. And if you’re really in a pinch and need to use more than 2% of your limit, just be sure to pay off that debt as quickly as possible to avoid any long-term damage to your credit score.

So, what percent of your credit should you use?

Honestly, it depends on who you ask. You’ll find opinions all over the place on this one. And, to be honest, there’s no 100% right or wrong answer. It really varies depending on your unique situation. However, there are some general guidelines you can follow. In this article, we’ll explore what some of those guidelines are.

What is the ideal percentage to use?

Most money experts will agree that if kept below 30%, your credit utilization rate has a minimal impact on your credit scores. In fact, it’s possible to have a great credit score with a utilization rate over 30%.

For example, let’s say you have a $10,000 credit limit and carry a $2,000 balance. Your utilization rate would be 20% ($2,000 divided by $10,000). And that 20% utilization rate is actually pretty good.

Carrying a balance of less than 10% of your credit limit is even better. So, if your credit limit goes up and you keep your balance at $2,000 or less, your utilization rate will drop — and that’s good for your credit scores.

What factors impact the ideal percentage?

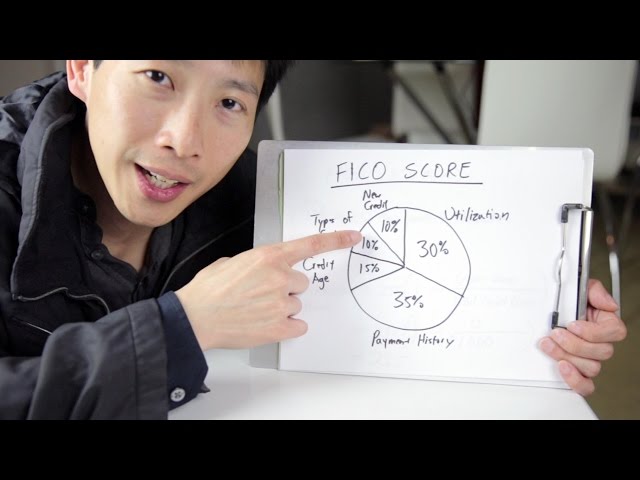

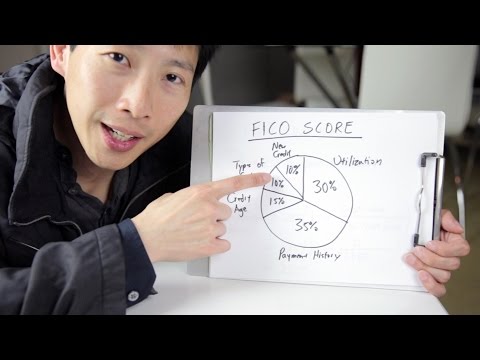

Usage rate is one factor that makes up your credit score—specifically, it’s the second most important factor, accounting for 30% of your FICO® Score☉ . But to really understand how it works, you have to understand credit utilization and what impacts your individual credit score.

Credit utilization is the second most important factor in your credit score— accounting for 30% of your FICO® Score☉ . Your credit utilization is calculated by dividing your total revolving balances by your total revolving credit limits. For example:

You have two credit cards, each with a credit limit of $1,000.

Card #1 has a balance of $200.

Card #2 has a balance of $800.

Your total balance is $1,000, and your total credit limits are $2,000, so your overall credit utilization ratio would be 50%.

Ideally, you want to keep your overall ratio below 30%, but the lower the better.