What is the Difference Between a Subsidized and an Unsubsidized Loan

Contents

The major difference between subsidized and unsubsidized loans is that the government pays the interest on a subsidized loan while the student is in school.

Checkout this video:

Introduction

When you hear the terms “subsidized” and “unsubsidized” in relation to student loans, it is referring to the interest that accrues on the loan while you are in school. A subsidized loan means that the government will pay the interest that accrues on your loan while you are in school. An unsubsidized loan means that you are responsible for paying the interest that accrues on your loan while you are in school.

Subsidized Loan

A subsidized loan is a loan on which the interest is paid by the government. This type of loan is available to students who demonstrate financial need, as determined by the Free Application for Federal Student Aid (FAFSA®).

The amount of money you can borrow with a subsidized loan depends on your financial need, your cost of attendance, your enrollment status and whether you are a dependent or independent student. For most students, the maximum amount is $5,500 for each academic year ($3,500 for first-year undergraduate students with no other aid).

Interest does not accrue (accumulate) on subsidized loans while you are in school and during your grace period. If you choose to defer repayment, interest will accrue during your deferment period.

Unsubsidized Loan

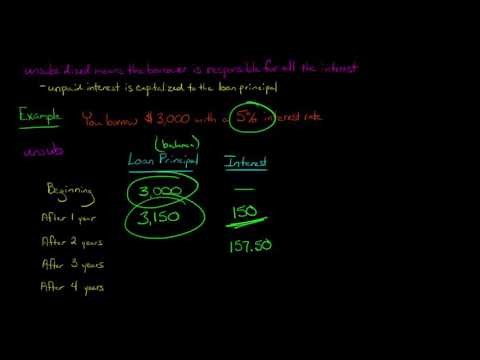

An unsubsidized loan is a type of financial aid that you have to pay back. The government does not subsidize or pay any of the interest for an unsubsidized loan. Interest will accrue (add up) from the day the loan is disbursed (paid out to you or your school) until it is paid in full. You can choose to pay the interest while you are in school or let it accrue and be added to your principal balance.

Differences between subsidized and unsubsidized loans

There are two main types of federal student loans: subsidized and unsubsidized. Here’s a quick rundown of the key differences between the two:

Subsidized loans are need-based, meaning that you must demonstrate financial need in order to qualify. If you do qualify, the government will cover the interest that accrues on your loan while you’re in school and during your grace period.

Unsubsidized loans are not need-based, meaning that you can qualify even if you don’t demonstrate financial need. However, if you take out an unsubsidized loan, you will be responsible for paying the interest that accrues on your loan while you’re in school and during your grace period.

Conclusion

There are two main types of student loans: subsidized and unsubsidized. Both types of loans have their own benefits and drawbacks, so it’s important to understand the difference before you decide which one is right for you.

A subsidized loan is a need-based loan that is offered by the government. The government pays the interest on your loan while you are in school, so you don’t have to worry about accruing interest during that time. This can save you a lot of money in the long run, because the interest on an unsubsidized loan will continue to accrue until you begin making payments after graduation.

The downside of a subsidized loan is that they are not available to everyone. You must demonstrate financial need in order to qualify for this type of loan. Additionally, there are limited funds available for subsidized loans, so they are not always an option for students who need them.

An unsubsidized loan is not need-based, so anyone can qualify for this type of loan regardless of their financial situation. However, because the government does not pay the interest on this type of loan, it will accrue while you are in school. This means that your loan balance will be higher when you begin making payments after graduation.

The upside of an unsubsidized loan is that they are available to everyone, regardless of financial need. Additionally, there are no limits on the amount you can borrow with an unsubsidized loan.

Ultimately, the choice between a subsidized and unsubsidized loan depends on your individual financial situation and needs. If you think you may qualify for a subsidized loan, it’s always worth checking into since the interest savings can be significant. However, if you don’t think you’ll qualify or if you need more money than what’s available through a subsidized loan, an unsubsidized loan may be a better option for you.