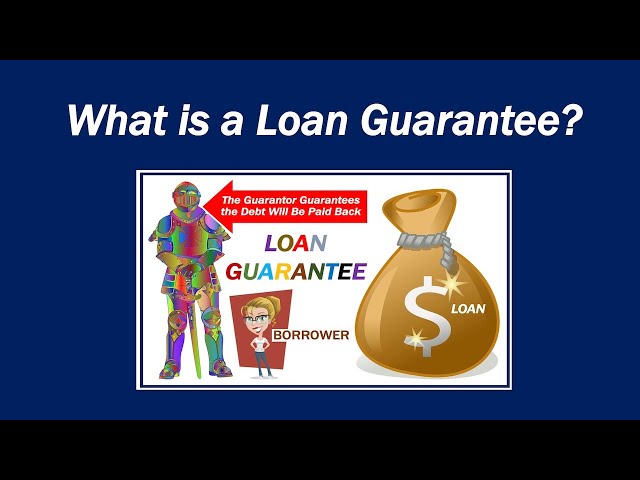

What is a Loan Guarantee?

Contents

A loan guarantee is a type of insurance that protects the lender if the borrower defaults on the loan. Loan guarantees can be issued by the government, private companies, or other financial institutions.

Checkout this video:

Introduction

A loan guarantee is a promise by a lending institution, such as a bank, to pay back a borrower’s loan if the borrower defaults. This type of guarantee gives the borrower peace of mind knowing that even if they are unable to repay the loan, the lender will still receive their money.

What is a loan guarantee?

A loan guarantee is a type of financial guarantee that is typically provided by a third party in order to secure a loan. The guarantee ensures that the lender will receive a certain amount of money if the borrower defaults on the loan.

What are the benefits of a loan guarantee?

A loan guarantee is when a lender agrees to back a borrower in case of default. This means that the lender will still get paid even if the borrower can’t make their payments. Loan guarantees can make it easier for borrowers to get loans because it reduces the risk for the lender.

There are several benefits of loan guarantees:

-Lenders are more likely to approve loans with a guarantee because it reduces their risk.

-Guarantees can help borrowers with bad credit get loans that they otherwise wouldn’t be able to get.

-Guarantees can help borrowers get lower interest rates because it reduces the risk for the lender.

Loan guarantees are not without risks, however. If a borrower defaults on a loan that is guaranteed, the lender will still have to pay back the entire loan. This can put the lender in a difficult financial position.

What are the risks of a loan guarantee?

There are a few risks associated with loan guarantees:

-The risk that the borrower will not be able to repay the loan

-The risk that the value of the collateral will not be enough to cover the loan

-The risk that the lender will not be able to collect on the guarantee if the borrower defaults

-The risk that the guarantor will not be able to pay if the borrower defaults

These risks are typically managed by requiring the borrower to provide additional collateral, or by limiting the amount of the loan that is guaranteed.

How does a loan guarantee work?

A loan guarantee is when a lender agrees to reimburse a borrower for any losses that they may incur if the borrower defaults on their loan. The lender will typically require some form of collateral, such as property, before agreeing to the loan guarantee. If the borrower does default, the lender will use the collateral to cover the losses.

How to get a loan guarantee?

There are several ways to get a loan guarantee. The most common is to have a third party such as a bank, insurance company, or government agency agree to back up the loan. This means that if you default on the loan, the lender can collect from the guarantor instead.

Guarantees can also be personal. In this case, someone with good credit agrees to cosign the loan with you. This person is then responsible for repayments if you can’t make them.

Another way to get a guarantee is to put up collateral. This is property or another asset that the lender can take if you don’t repay the loan. For example, you might use your car as collateral for a personal loan.

What are the conditions of a loan guarantee?

A loan guarantee is an agreement by a lender to provide financing for a borrower, contingent upon the borrower’s obtaining another loan from a third party. If the borrower defaults on the new loan, the lender that provided the guarantee will be responsible for repaying the third-party lender.

Loan guarantees are often used by small businesses and startups that may not have established enough credit history to qualify for a loan on their own. The guarantee gives the lender assurance that if the borrower defaults, they will still be repaid.

Conditions of a loan guarantee may vary, but usually include a minimum credit score for the borrower and often also require collateral, such as a personal guarantee or real estate. The terms of a loan guarantee are negotiable between the lender and borrower.

Case study: The UK loan guarantee scheme

The UK government launched a loan guarantee scheme in October 2008, in response to the global financial crisis. The scheme was designed to support banks and other lenders who were struggling to raise funds.

Under the scheme, the government agreed to provide a guarantee of up to 75% of the value of loans made by participating banks. This meant that if a borrower defaulted on their loan, the government would cover the cost of any losses incurred by the bank.

The scheme was initially due to run for one year, but was extended several times and eventually closed in 2012. In total, around £140 billion (about US$180 billion) of guarantees were issued under the scheme.

The UK loan guarantee scheme was widely praised for its effectiveness in supporting lending during the financial crisis. However, it was also criticized for including too many risky loans, and for not doing enough to support small businesses.

Conclusion

A loan guarantee is an agreement between two parties in which one party agrees to be responsible for the debt of the other party in the event that the original borrower defaults on the loan. Loan guarantees are often used by financial institutions to reduce the risk of lending money, and as a result, they can make it easier for borrowers to obtain loans.