What Is a Finance Charge on a Credit Card?

Contents

A finance charge is the cost of borrowing money on your credit card account. If you carry a balance on your card from month to month, you’ll likely be charged a finance charge.

Credit Card?’ style=”display:none”>Checkout this video:

What Is a Finance Charge?

A finance charge is the cost of borrowing money.

When you use a credit card, you are borrowing money from the card issuer. The card issuer charges interest on the money you borrowed, and this is called a finance charge.

The finance charge is calculated based on your annual percentage rate (APR) and the amount of time you keep the balance on your credit card.

For example, let’s say you have a credit card with an APR of 18%. If you borrowed $100 from the credit card and kept the balance for one month, your finance charge would be $1.50.

You can avoid paying a finance charge by paying your credit card balance in full each month. Most credit card issuers will give you a grace period of 21 days to pay your balance without charging interest.

How Is the Finance Charge Calculated?

The finance charge on a credit card is the fee charged by the card issuer for borrowing money. This charge is typically expressed as an annual percentage rate (APR). For example, if you have a credit card with a 20% APR, you will be charged 20% of the outstanding balance on your card each year.

The finance charge is generally calculated by applying the APR to the outstanding balance on the credit card. This can be done on a daily, weekly, or monthly basis. For example, if you have a credit card with a $1,000 balance and a 20% APR, you will be charged $2 per day in interest ($1,000 x 20% / 365).

Some credit cards also have additional fees, such as annual fees and late payment fees, that are added to the finance charge. These fees are generally disclosed in the credit card agreement.

It’s important to note that the finance charge is not the same as the interest charged on a loan. The finance charge is only levied on balances that are carried over from month to month, while interest is charged on new purchases and cash advances immediately.

If you pay your entire balance in full each month, you will not be charged a finance fee. However, if you only make the minimum payment, you will be charged interest on your remaining balance and may also be subject to late payment fees.

What Are the Types of Finance Charges?

There are four main types of finance charges: interest, fees, penalties, and credit insurance premiums.

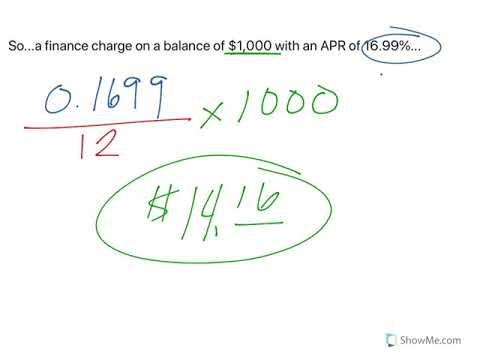

Interest is the most common type of finance charge. It’s based on the amount of money you owe, the interest rate your card charges, and the length of time you carry a balance. For example, if you have a balance of $1,000 and an annual percentage rate (APR) of 18%, your monthly interest charge would be $15 ($1,000 x 0.018/12).

Fees are one-time charges that can be assessed when you open a new account, use your card for certain transactions, or fail to make a payment on time. For example, many cards charge an annual fee just for having the account. Others may assess a fee each time you make a purchase with the card. Cash advance and balance transfer fees are also common.

Penalties are charged when you violate the terms of your credit card agreement. The most common penalty is a late payment fee, which is assessed if you don’t make at least your minimum payment by the due date. Other penalties can include over-the-limit fees and returned payment fees.

Credit insurance premiums are optional fees that some cardholders choose to pay in exchange for coverage in case of death or unemployment. This type of insurance is not required by law and is generally not considered worth the cost.

How Can You Avoid Finance Charges?

Here are some tips to help you avoid finance charges:

-Pay your balance in full and on time every month.

-Know your credit card’s grace period.

-Avoid using your credit card for cash advances and balance transfers.

-Limit your credit card purchases to items you know you can afford.

-Read your credit card statement carefully and dispute any errors promptly.

If you are ever unsure about whether or not a particular purchase will result in a finance charge, be sure to ask the merchant or give your credit card issuer a call before making the purchase.

How to Dispute a Finance Charge

If you think a finance charge on your credit card is incorrect, you can dispute the charge with your credit card issuer. You should do this as soon as possible after receiving your statement with the charge. Write a letter to the issuer and include your name, account number, and the amount of the charge you are disputing. You can also include why you believe the finance charge is incorrect.

Keep in mind that if you have already paid the finance charge, you may not be able to get a refund. But if you have not paid it yet, the credit card issuer may remove the finance charge from your account if they find that it was indeed incorrect.