How to Calculate Credit Utilization

Contents

A credit utilization ratio is the amount of debt you have compared to your credit limit. A lower ratio is better. Here’s how to calculate it.

Checkout this video:

What is credit utilization?

Credit utilization is a key factor in your credit score—the lower your utilization, the better. Credit utilization is determined by dividing your total credit balances by your total credit limits. For example, if you have $3,000 in credit card debt across three cards with respective credit limits of $5,000, $10,000, and $15,000, your credit utilization would be 20%.

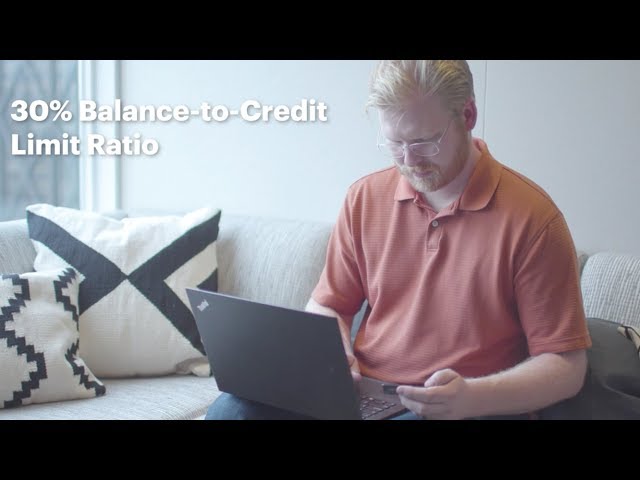

A good rule of thumb is to keep your credit utilization below 30%. Some experts recommend even lower ratios—below 10% or even 0% if possible. The idea is that by keeping your usage low, you’re showing creditors that you’re a responsible borrower who isn’t maxing out your cards and putting yourself at risk of default.

Of course, a low credit utilization won’t help your score if you’re carrying a lot of debt or if you have other negative information on your credit report. But if you’re trying to improve your credit score, reducing your utilization is a good place to start.

How is credit utilization calculated?

Your credit utilization is calculated by dividing your current credit balance by your credit limit.

For example, if you have a $1,000 balance on a credit card with a $5,000 limit, your credit utilization would be 20%.

A good rule of thumb is to keep your credit utilization below 30%, but the lower the better. A lower credit utilization indicates to lenders that you manage your credit well and are less likely to default on a loan.

What is a good credit utilization ratio?

The credit utilization ratio is the percentage of your credit limits that you are currently using. A good credit utilization ratio is between 10% and 30%. A higher percentage will lower your credit score, and a lower percentage will raise it.

How can I improve my credit utilization ratio?

There are a few things you can do to improve your credit utilization ratio:

1. Pay your bills on time. This is the number one factor in your credit score, so it’s important to keep up with your payments.

2. Keep your balances low. You don’t have to completely eliminate your debt, but try to keep your balances as low as possible.

3. Use credit wisely. Don’t open new accounts just to get a better credit utilization ratio – this can actually backfire and hurt your score. Use credit wisely and only open new accounts when you need them.

4. Check your report regularly. Make sure that the information on your report is accurate, so you can catch any mistakes that might be inflating your credit utilization ratio.

What are the other factors that affect my credit score?

There are many factors that can affect your credit score, including your payment history, credit mix, and length of credit history. However, one of the most important factors is your credit utilization ratio.

Your credit utilization ratio is the amount of debt you have compared to your credit limit. For example, if you have a credit card with a $1,000 limit and you owe $500 on the card, your credit utilization ratio is 50%.

Ideally, you should keep your credit utilization ratio below 30%. This means that you should owe no more than $300 on a card with a $1,000 limit. If you have multiple cards, you should try to keep the total amount of debt below 30% of your combined limits.

There are a few things you can do to improve your credit utilization ratio. First, try to pay down your existing debt. Second, if you have multiple cards, try to transfer some of the balances to cards with lower limits. Finally, ask your creditors for higher limits.