How Do You Pay Off a Credit Card?

Contents

If you’re trying to pay off a credit card , you’re not alone. In fact, credit card debt is one of the most common types of debt that people carry. But don’t despair – there are ways to pay off your credit card and get out of debt. Check out our tips on how to pay off a credit card and start getting your finances back on track.

Credit Card?’ style=”display:none”>Checkout this video:

Introduction

If you have credit card debt, you’re not alone: The average American household owes $5,700 on their credit cards, according to CNN Money. But there’s good news: It’s possible to get out of debt. In fact, with the right strategy, you can be debt-free in no time.

There are two basic methods for paying off credit card debt: the “debt snowball” method and the “debt avalanche” method. With the debt snowball method, you focus on paying off your smallest balance first while making minimum payments on your other debts. Once your smallest debt is paid off, you move on to your next smallest debt, and so on until all of your debts are paid off. The benefit of this method is that it can help motivate you to keep going: As you see your debts shrinking, it’ll give you the boost you need to keep going until all of your debts are gone.

With the debt avalanche method, you focus on paying off your debt with the highest interest rate first while making minimum payments on your other debts. Once your high-interest debt is paid off, you move on to your next highest-interest debt, and so on until all of your debts are paid off. The benefit of this method is that it saves you money in the long run: By targeting your high-interest debts first, you’ll pay less in interest over time and be able to get out of debt faster.

Both methods can work well — it really just depends on what works best for you. If you need some motivation to keep going, the debt snowball method might be a good choice; if saving money is your priority, the debt avalanche method might be a better fit. Whichever method you choose, make sure you have a plan in place and make a commitment to stick with it — that’s how you’ll be able to pay off your credit card Debt once and for all.

Minimum Payments

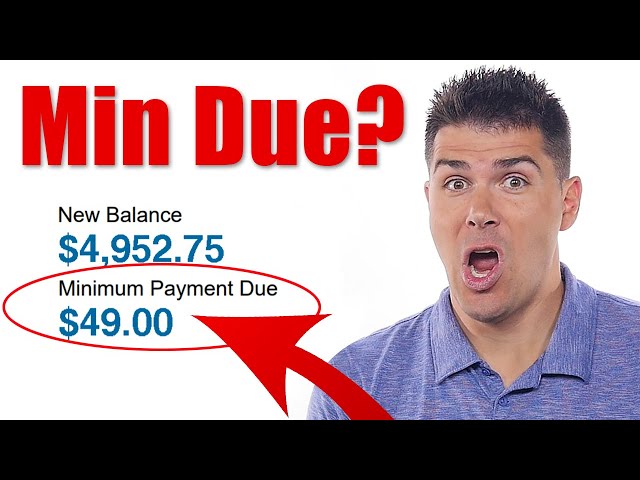

The minimum payment is the lowest amount you can pay on your credit card bill each month without getting penalized. Your minimum payment will be different each month, and will be based on your outstanding balance and interest rate.

Paying only the minimum payment each month will result in costly interest charges and will take a long time to pay off your balance. In fact, if you make only the minimum payments on a $3,000 balance with a 18% APR, it would take you 30 years to pay off the debt and you would end up paying more than $14,000 in interest!

The Snowball Method

The Snowball Method is a debt payoff strategy where you pay off your debts from smallest to largest, regardless of interest rate. When you’re making payments on multiple debts, it can be difficult to stay motivated. The Snowball Method can help by giving you small wins early on that will keep you motivated to stick with your plan.

To use the Snowball Method, list all of your debts from smallest to largest. Make the minimum payment on all of your debts except for the one with the smallest balance. put as much money as you can toward paying off the debt with the smallest balance. Once that debt is paid off, you’ll have more money available to put toward your next debt on the list. You’ll repeat this process until all of your debts are paid off.

The Snowball Method can work well if you’re struggling with multiple debts and need a simple plan to stay on track. But keep in mind that this strategy could end up costing you more in interest charges if some of your debts have higher interest rates than others.

The Avalanche Method

The avalanche method is a debt payoff strategy in which you pay off your debts from the highest interest rate to the lowest. The logic behind this strategy is that you’ll save more money in interest over the long run by tackling the debt with the highest interest rate first.

To use the avalanche method, you’ll need to list out all of your debts from highest interest rate to lowest. Then, you’ll make the minimum payments on all of your debts except for the one with the highest interest rate. For that debt, you’ll put as much money as possible towards paying it off. Once it’s paid off, you can move on to tackling the next debt on your list.

The main benefit of the avalanche method is that it can save you money in interest over time. By targeting the debt with the highest interest rate first, you’ll minimize the amount of interest you accrue on your outstanding debt. This can lead to a faster overall pay-off, as well as lower total interest payments.

There are a few potential drawbacks to using the avalanche method, however. First, it can take longer to see results when using this strategy since you’re not targeting any specific debts for accelerated payoff. This can be frustrating if you’re struggling with high interest rates and are eager to get rid of your debt as soon as possible. Additionally, focusing solely on debt with high interest rates can ignore other important factors, like emotional stress or quality of life. In some cases, it may make more sense to target smaller debts first so that you can get a “quick win” and boost your motivation levels.

Balance Transfers

There are a few different ways to pay off a credit card. One option is to do a balance transfer. This means you transfer the balance of your credit card to another account, usually one with a lower interest rate. This can help you save money on interest and pay off your debt faster.

Another option is to make extra payments on your credit card. You can do this by either setting up automatic payments from your checking account or making manual payments each month. If you make more than the minimum payment, you will pay off your debt faster and save money on interest.

You can also use a personal loan to pay off your credit card debt. This can be a good option if you have good credit and can qualify for a low-interest loan. Personal loans can help you save money on interest and pay off your debt faster than making extra payments on your credit card.

Whatever method you choose, it is important to make sure that you are making at least the minimum payment on your credit card each month. If you only make the minimum payment, it will take longer to pay off your debt and you will end up paying more in interest.

Personal Loans

Personal loans can be used for a variety of purposes, including paying off credit cards. If you have good credit, you may be able to qualify for a personal loan with a lower interest rate than what you’re currently paying on your credit card, which can help you save money on interest and pay off your debt faster.

There are a few things to keep in mind when using a personal loan to pay off credit card debt:

-Make sure you compare interest rates and fees before taking out a personal loan. Some personal loans come with origination fees or prepayment penalties, which could offset any interest rate savings.

-It’s important to note that your credit score may be impacted if you close an older credit card account when you pay it off with a personal loan. This is because closing an account can shorten your average credit history, which is one factor that determines your credit score. If possible, try to keep the account open and just make the minimum payment until the balance is paid in full.

-If you have good credit, you may be able to get a 0% APR introductory offer on a new credit card and transfer your balance from your old card. This could help you save on interest in the long run and give you some breathing room with your monthly payments. Just be sure to read the fine print and understand any potential fees before taking advantage of this offer.

Debt Settlement

One of the most effective—although often extreme—means of reducing your credit card debt is to enter into a debt settlement agreement with your creditor.

In a debt settlement, you and your creditor agree on a lump-sum payment that is less than the full amount you owe. For example, if you owe $10,000, you might agree to pay $7,000. Your creditor agrees to accept the reduced amount as payment in full on your debt.

Debt settlement is an extreme measure because it will have a negative impact on your credit score and may result in a lawsuit. Therefore, it’s important to consider debt settlement only as a last resort after you have explored all other options for reducing your credit card debt.