What is a Credit Card Statement?

Contents

A credit card statement is a monthly report from your credit card issuer that lists your activity for the billing period.

Credit Card Statement?’ style=”display:none”>Checkout this video:

What is a Credit Card Statement?

A credit card statement is a monthly or quarterly report that shows all the activity on your credit card account for a billing period. This includes all the transactions you made, any fees or interest charged, and your current balance. Your credit card statement can help you keep track of your spending, so you can stay on budget.

What is included in a Credit Card Statement?

A credit card statement is a record of your credit card activity for a set period of time, usually one billing cycle. It will show all the charges made on your account, as well as any payments you have made and any interest or fees charged.

Your credit card statement will also show your current balance, which is the total amount you owe on your credit card. This can be useful information if you are trying to stay within your credit limit or if you are trying to pay off your balance.

If you have made any late payments, these will also be listed on your statement. This information can help you keep track of your spending and make sure that you are paying off your balance on time.

How often is a Credit Card Statement issued?

Most credit card issuers will send you a statement every month. This monthly statement will include all of the transactions that you made during the billing cycle, including any interest or fees that have accrued. Your credit card company may print and mail your statement to you, or they may make it available online for you to view.

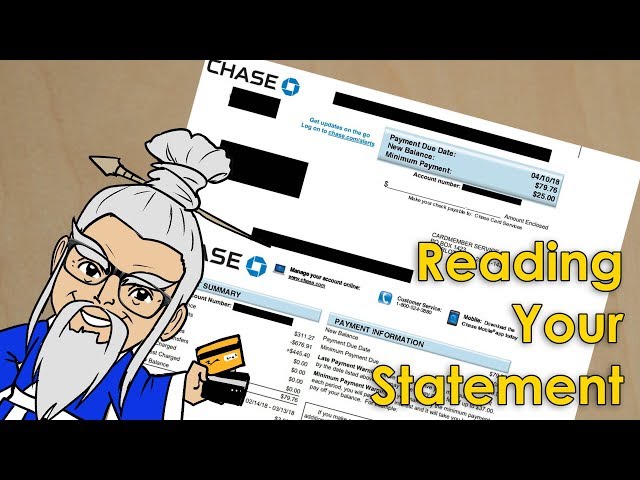

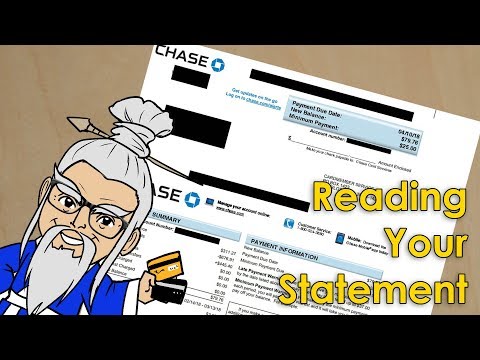

How to Read a Credit Card Statement

Your credit card statement is a summary of your credit card activity for the billing period. It includes your balance, payments, credits, and other activity during the period, as well as any finance charges. Most statements also include important information like your credit limit, current interest rate, and payment due date. Your credit card issuer must send you a statement at least 21 days before your payment is due.

How to understand the different charges on your Credit Card Statement

Your credit card statement is a record of your credit card activity over a billing period, typically one month. It lists each purchase, withdrawal, or payment you made with your credit card during that time frame, as well as any fees or interest charged.

Understanding your credit card statement can help you keep track of your spending and spot any unauthorized charges. It can also help you see how much interest you’re paying on your outstanding balance and make informed decisions about paying off your debt.

Here’s a quick guide to understanding the different charges on your credit card statement:

Credit Card Statement Date: This is the date that your statement was generated. Your payment is due on or before this date.

Previous Balance: This is the unpaid balance from your previous statement. Any payments you made since then will be subtracted from this amount.

New Charges: This is a list of all the new transactions made with your credit card since the last statement date. This includes purchases, cash advances, balance transfers, and any other type of transaction.

Payment Received: This is the total amount of payments you made since the last statement date, including any payments made toward new charges or toward your previous balance.

Credits Received: This is the total amount of credits applied to your account since the last statement date. Credits can include things like returned purchases and cash back rewards.

Interest Charged: This is the amount of interest that has accrued on your outstanding balance since the last statement date.

Late Fees Charged: If you paid your previous balance after the due date, you may be charged a late fee . This will be listed here if applicable.

Returned Payment Fee: If a payment you made was returned by your bank (for example, if there were insufficient funds in your account), you may be charged a returned payment fee by your credit card issuer . This will be listed here if applicable.

Understanding these charges can help you keep track of your spending and avoid costly fees . If you have any questions about charges on your credit card statement, contact your credit card issuer for more information.

How to understand your Credit Card Statement balance

The balance on your credit card statement is your account balance. This is the total amount you owe on your credit card at the time your statement was generated, including any new charges, payments, interest, and fees since your last statement.

Your account balance is different from your current balance, which is the amount you owe on your credit card at any given time. Your current balance can fluctuate throughout the month as you make new purchases or payments on your account.

You can find your account balance on your credit card statement, which is typically sent to you once a month. Make sure to review your statement carefully so you can understand all the charges and activity on your account. If you have any questions about a charge on your statement, you can contact your credit card issuer for more information.

Tips for Managing your Credit Card Statement

A credit card statement is a monthly report that lists all of the activity on your credit card account for the previous month. This includes all purchases, payments, and any other activity that has occurred on your account. Your credit card statement can help you keep track of your spending and spot any fraudulent activity. Here are some tips for managing your credit card statement.

How to avoid paying interest on your Credit Card Statement

If you have a credit card, you’re probably used to getting a statement in the mail every month. This statement shows all of the activity on your account for the past month, including any purchases, payments, fees, and interest charged.

The most important thing to look at on your credit card statement is the “amount due.” This is the total amount of money you owe for the month, and it’s important to pay this amount by the due date to avoid paying interest.

Paying interest on your credit card balance is one of the biggest wastes of money, so it’s important to understand how to avoid it. Here are a few tips:

– Pay your balance in full every month. This is the best way to avoid paying interest, and it’s also a good way to improve your credit score.

– If you can’t pay your balance in full, try to pay as much as possible. The more you pay, the less interest you’ll owe.

– Use a low-interest credit card. If you have a high-interest credit card, consider transferring your balance to a card with a lower interest rate. Many cards offer 0% APR for 12 months or more on balance transfers.

– Get a personal loan. If you have good credit, you may be able to get a personal loan with a lower interest rate than your credit card. You can use this loan to pay off your credit card balance, and then make monthly payments on the loan instead of paying interest on your credit card.

How to use your Credit Card Statement to improve your credit score

Your credit card statement is one of the most important tools you have to manage your credit score. Here are a few tips to help you make the most of it:

First, take a close look at your statement to make sure all of the charges are accurate. If you see any discrepancies, be sure to contact your creditor right away to resolve the issue.

Next, take a look at your spending patterns. Are there any areas where you can cut back? If so, make a plan to do so. This will not only help improve your credit score, but it will also save you money in the long run.

Finally, keep an eye on your account balance. If it gets too high, consider making a payment before your next billing cycle begins. This will show creditors that you are actively working to keep your debt under control and will help improve your credit score over time.