What Can Good Credit Get You?

Contents

If you have good credit , you may be able to get a lower interest rate on a loan or credit card. You may also be able to rent an apartment or buy a car. Good credit can also help you get a job.

Credit Get You?’ style=”display:none”>Checkout this video:

The Basics of Good Credit

Having good credit is important. It can get you lower interest rates on loans, better credit card terms, and make it easier to rent or buy a home. In general, good credit means less financial stress and more opportunities. Here are the basics of good credit.

What is a credit score?

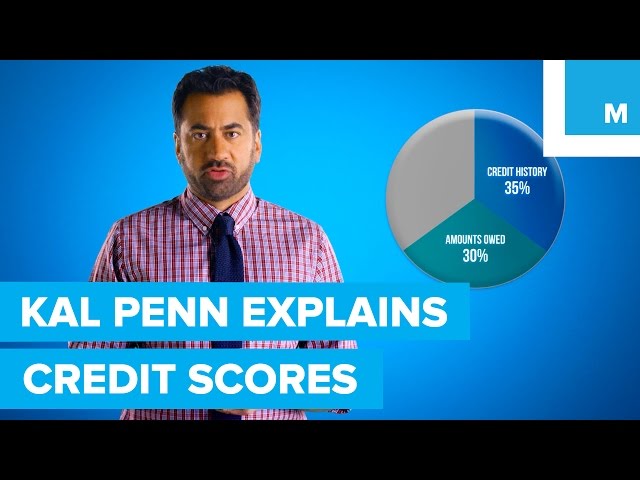

Your credit score is a number that reflects the risk you pose to creditors. It is based on your credit history, which is a record of your borrowing and repayment activity. The higher your score, the lower the risk you pose, and the more likely you are to get approved for a loan or line of credit.

A good credit score can open doors for you – from getting a better interest rate on a loan to qualifying for a lease on an apartment. A bad credit score can make it difficult to get approved for financing, and can result in higher interest rates and fees if you are approved.

There are many different ways to calculate a credit score, but the most common method uses a scale of 300 to 850. The higher your score, the better. Here is what each range on the scale generally means:

300-579: Poor

580-669: Fair

670-739: Good

740-799: Very Good

800-850: Excellent

What is a credit report?

Your credit report is a snapshot of your credit history. It includes information about your credit accounts, including the type of account, the date it was opened, the credit limit or loan amount, the balance owed, and your payment history. It also includes information about any late payments or collections actions on your accounts.

The Benefits of Good Credit

Good credit can get you a lot of things in life. A good credit score can help you get a lower interest rate on a loan, it can help you get a better rental agreement, and it can even help you get a job. In general, good credit is going to make your life easier. Let’s take a look at some of the specific benefits of having good credit.

Lower interest rates

When it comes to borrowing money, those with good credit will always have an easier time than those with bad credit. That’s because lenders see good credit as an indication that a borrower is more likely to repay their debt. As a result, borrowers with good credit tend to get lower interest rates on loans, which can save them a lot of money over time.

For example, let’s say you want to take out a $10,000 loan with a three-year repayment period. If you have good credit and qualify for a 4% interest rate, your monthly payments would be $297 and you would pay a total of $1,089 in interest over the life of the loan. But if you have bad credit and can only qualify for a 17% interest rate, your monthly payments would jump to $676 and you would pay $5,067 in interest — nearly five times as much!

Of course, not everyone can qualify for the lowest possible interest rate. But even borrowers who don’t get the best rates can still save money by having good credit. That’s because lenders typically offer their best rates to borrowers with scores at or above the “prime” level — currently 703 for FICO scores and 667 for VantageScores. So if your score is above 600 (the minimum for most lenders), you’re likely to get a better deal than someone with bad credit.

Better credit card rewards

One of the most immediate benefits of good credit is the ability to qualify for cards with better rewards. If you have good credit, you’ll likely be able to qualify for a rewards credit card that offers points, cash back, or other perks for every purchase you make.

Rewards credit cards often come with valuable sign-up bonuses that can put hundreds of dollars back in your pocket if you meet the card’s minimum spending requirements. And if you use your card wisely, the rewards you earn can offset the cost of interest and help you save money on everyday purchases.

A higher credit limit

A higher credit limit can help you in several ways. It can give you more flexibility when making purchases, help you during an emergency, and improve your credit score.

A higher credit limit can help you make larger purchases without maxing out your credit card. This can be useful if you need to make an emergency purchase or if you want to take advantage of a sale. Having a higher credit limit can also help improve your credit score. This is because your credit utilization – the amount of your available credit that you are using – is one of the factors that goes into calculating your score. A higher credit limit means that you can use more of your available credit without affecting your score as much.

If you have good credit, you may be able to qualify for a higher credit limit on your existing cards or when you apply for new ones. You can also ask for a higher limit in person or over the phone. When requesting a higher limit, it’s helpful to have proof of income and payment history handy to show the issuer that you’re capable of handling a larger amount of debt.

How to Maintain Good Credit

Your credit score is a number that represents your creditworthiness. A good credit score means you’re a low-risk borrower, which could lead to lenders approving your loan or credit card application and/or offering you a lower interest rate. In short, good credit can save you money. Here’s how you can maintain good credit.

Pay your bills on time

Your payment history is one of the most important factors in your credit score—making up 35% of your FICO® Score—so you want to make sure you pay all your bills on time. That includes credit cards, utilities, telephone service, and any other regular payments.

If you have trouble remembering when all your bills are due, set up automatic payments through your bank or sign up for a service that will do it for you.

Paying all your bills on time is the single best thing you can do to improve your credit score.

Keep your credit utilization low

Credit utilization is a key factor in credit scores. It’s important to keep your balances well below your credit limit. A good rule of thumb is to keep your balances at or below 30% of your credit limit. This will help show creditors that you’re capable of managing your debt and not overextending yourself.

If you have a high balance on one or more of your cards, try to pay it down as quickly as possible. You can also contact your creditor and ask for a higher credit limit. This can be helpful if you have a high balance and you want to lower your credit utilization ratio. Just be sure to only request an increase if you’re confident you can handle the extra credit.

Monitor your credit report for errors

Good credit is important for many reasons. It can help you get approved for loans, lower interest rates, and even get certain jobs. That’s why it’s so important to monitor your credit report for errors.

You can order a free copy of your credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) once every 12 months. You can also use a service like Credit Karma to track your credit score for free.

If you see any errors on your credit report, you should dispute them right away. You can do this online or by mail. Be sure to include any supporting documentation that you have. The credit bureau will then have 30 days to investigate the error and update your report.

What to Do if You Have Bad Credit

Having good credit can get you a lot of things: a higher credit limit, a lower interest rate, and even a job. On the other hand, bad credit can do the opposite. If you have bad credit, you may be denied for a loan, have to pay a higher interest rate, or even be denied for a job. So, what can you do if you have bad credit?

Get a copy of your credit report

If you find inaccurate or incorrect information on your credit report, you should take steps to have it corrected. You can do this by contacting the credit reporting agency (CRA) directly. The CRA will then investigate your claim and make any necessary corrections.

You should also contact the company that provided the information to the CRA. This is so you can let them know there may be an error on their end. The company will also investigate your claim and make any necessary corrections.

Identify the negative items on your report

Start by ordering your credit report from one (or all) of the three main credit reporting bureaus: Equifax, Experian and TransUnion. Review your report carefully to identify any negative items that may be dragging down your score. These could be items such as late payments, collections accounts, charge-offs or even bankruptcies.

dispute the negative items on your report

If you think any of the information in your credit report is inaccurate, you can file a dispute with the credit reporting agency. The credit reporting agency will then investigate the dispute and removed the inaccurate items if they are found to be incorrect. This process can take a few weeks, but it is important to make sure that your credit report is accurate before you apply for any loans or new lines of credit.