How to Get a Loan from a Credit Union

Contents

If you’re looking for a loan from a credit union, there are a few things you’ll need to do first. Here’s a quick guide on how to get started.

Checkout this video:

Overview

A credit union is a financial cooperative that is owned and controlled by its members. Unlike a bank, a credit union does not have shareholders. Its members are also its customers, and they elect a board of directors to run the credit union. Each credit union has its own rules about who can join, but membership is usually open to people who live, work, or worship in the same area.

Credit unions offer many of the same products and services as banks, including loans. In fact, you may be able to get a better deal on a loan from a credit union than you could from a bank. Here’s what you need to know about how to get a loan from a credit union.

1. Find a credit union that you’re eligible to join. If you’re not sure, ask family and friends if they belong to any credit unions that they would recommend. You can also check with the National Credit Union Administration (NCUA), which is the federal agency that regulates credit unions.

2. Once you’ve found a few potential credit unions, find out what type of loans they offer and whether you meet their eligibility requirements. For example, some credit unions only offer loans to members who have an account with the Credit Union for at least six months.

3. Once you’ve chosen a Credit Union, you’ll need to become a member before you can apply for a loan. To do this, you’ll likely need to open an account with the Credit Union and maintain it for at least six months before applying for a loan.

4. When you’re ready to apply for the loan, gather all of the required documentation beforehand so that you can fill out your application completely and accurately

How to Join a Credit Union

Joining a credit union is easy and can be done online in just a few minutes. To join, you’ll need to provide some basic information like your name, address, and date of birth. You may also be required to open a savings account with the credit union, which is used to keep your funds safe and secure. Once you’ve joined, you’ll be able to apply for loans, credit cards, and other financial products offered by the credit union.

Applying for a Loan

Applying for a loan from a credit union is a great way to get the money you need without having to pay high interest rates. Credit unions are nonprofit organizations that offer their members low-interest loans. To qualify for a loan from a credit union, you will need to become a member of the credit union. This usually involves opening a savings account and making a small deposit.

Personal Loans

personal loan from a credit union, you will probably have to become a member of the credit union first. There are many different types of credit unions, each with their own requirements for membership. Some credit unions require that you work for a certain employer, live in a certain area, or belong to a certain organization. Others are open to anyone who wants to join.

Once you have joined the credit union, you will need to apply for the loan. The application process will vary from credit union to credit union, but most will require you to fill out a loan application and provide some financial information. The credit union will use this information to determine whether or not you are eligible for the loan and how much they are willing to lend you.

Once you have been approved for the loan, you will need to sign a loan agreement. This document will specify the repayment terms and interest rate of the loan. Make sure that you understand these terms before signing the agreement.

Auto Loans

Auto loans are a type of loan that is specifically designated for the purchase of a vehicle. The vehicle serves as collateral for the loan, which means that if you default on your loan payments, the lender can repossess your vehicle. auto loans typically have lower interest rates than other types of loans, such as personal loans or credit cards.

To apply for an auto loan from a credit union, you will need to become a member of the credit union first. Once you are a member, you can apply for a loan by filling out an application and submitting it to the credit union. The credit union will then review your application and make a decision on whether or not to approve your loan.

Home Equity Loans

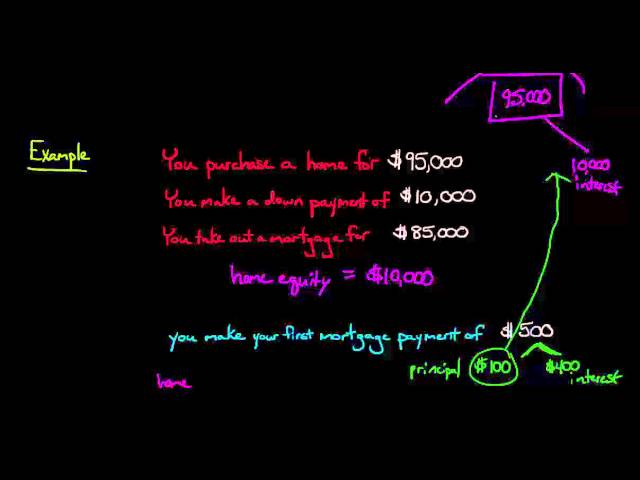

A home equity loan is a type of loan in which the borrower uses the equity of their house as collateral. Equity is the difference between the appraised value of the house and the amount still owed on the mortgage. For example, if your house is worth $250,000 and you owe $150,000 on your mortgage, you have $100,000 in equity.

Lenders will approve a loan for a certain percentage of the appraisal, usually up to 80%. In our example above, you could potentially borrow up to $80,000. The interest rate on a home equity loan is usually lower than that of a personal loan or credit card because the loan is secured by your house.

You may be able to deduct the interest you pay on a home equity loan from your taxes, but consult a tax advisor to be sure. A home equity loan is different from a home equity line of credit (HELOC), which allows you to borrow against your equity over time up to a certain limit.

Other Types of Loans Offered by Credit Unions

While credit unions offer several types of loans, the most common type of loan that people apply for is a personal loan. Credit unions offer personal loans for a variety of reasons, including debt consolidation, home repairs, medical expenses, and more. If you’re considering a personal loan from a credit union, it’s important to know the different types of loans that they offer.

Business Loans

Business loans from credit unions tend to be smaller than those offered by banks. The maximum loan amount is $50,000, and the average loan amount is $13,000. Interest rates on business loans from credit unions are also lower than those offered by banks, with rates ranging from 7% to 9%. Credit unions typically require collateral for business loans in the form of a business savings account, personal savings account, or CD.

Student Loans

Student loans are a great way to finance your education. Credit unions offer competitive rates and terms on student loans, making them a great option for borrowers.

Credit unions offer both private and federal student loans. Private student loans are made by banks, credit unions, and other private lenders. Federal student loans are made by the government and have fixed interest rates.

Most credit unions offer variable-rate private student loans, which means the interest rate can fluctuate over time. Variable-rate loans typically have lower interest rates than fixed-rate loans, but they can increase over time.

When you apply for a student loan from a credit union, you will need to fill out a loan application and provide proof of your income, asset, and debts. The credit union will then review your information and make a decision on whether or not to approve your loan.

Payday Alternative Loans

Payday Alternative Loans (PALs) are small, short-term unsecured loans offered by many credit unions. With a PAL, you can borrow up to $1,000 (depending on the credit union) for terms ranging from one to six months. Credit unions typically charge lower fees and interest rates for PALs than payday lenders. And, if you have trouble repaying your PAL, the credit union will work with you to develop a repayment plan.

Advantages of Getting a Loan from a Credit Union

There are a number of advantages to getting a loan from a credit union over other lending institutions. Credit unions are nonprofit organizations, so they tend to have lower interest rates and fees than banks. They also offer more flexible terms on loans, which can be helpful if you have less-than-perfect credit. Another advantage of credit unions is that they often work with members to create customized loan programs that meet their unique needs.

Disadvantages of Getting a Loan from a Credit Union

Though credit unions have many benefits, there are a few disadvantages to keep in mind when you’re considering getting a loan from one.

Credit unions typically have shorter operating hours than banks. This can make it difficult to get help when you need it.

Credit unions also tend to have fewer branches than banks. This can make it inconvenient to access your money.

Finally, credit unions may not offer all of the same services as banks. For example, you may not be able to get a mortgage from a credit union.

Alternatives to Getting a Loan from a Credit Union

There are a few alternatives to getting a loan from a credit union. You could get a loan from a bank, an online lender, or a peer-to-peer lending platform. Each option has its own set of pros and cons, so be sure to do your research before choosing one.

Banks:Loans from banks tend to have lower interest rates than those from other lenders. However, they may also require collateral, such as your home or car, to approve the loan.

Online Lenders: Online lenders usually have a more streamlined application process than banks. However, they may charge higher interest rates and fees.

Peer-to-Peer Lending Platforms: Peer-to-peer lending platforms connect borrowers with investors who are willing to fund their loans. Loans from these platforms tend to have competitive interest rates. However, they may require a good credit score for approval.