How to Calculate a Loan

Contents

How to Calculate a Loan – Banks and other lenders use a complex set of criteria to determine the size and terms of the loan they’ll offer you.

Checkout this video:

Introduction

When you borrow money, you agree to pay it back over time, usually with interest. To calculate the total cost of your loan, you need to know the interest rate, the term of the loan, and the amount you’re borrowing. With that information, you can use a simple equation to calculate your monthly payment or the total amount you’ll pay over the life of the loan.

The steps to calculate a loan

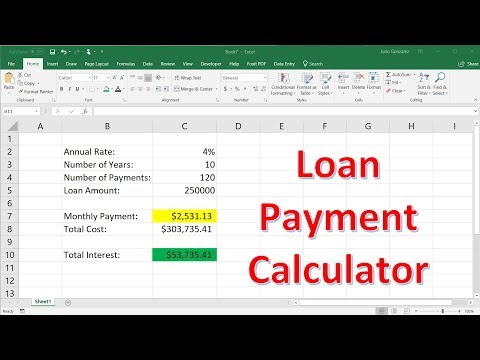

There are a few things you need to know before you can calculate a loan. The first is the interest rate. This is the amount of money you will be charged for borrowing the money. The second is the term of the loan, which is the length of time you have to pay back the loan. The last is the amount of the loan, which is the total amount of money you are borrowing.

Enter the loan amount

The first step is to enter the loan amount that you want to calculate.

Enter the interest rate

Interest is the cost of borrowing money, and the interest rate is the percentage of the loan amount that you will pay in interest over the life of the loan. To calculate the interest rate on your loan, divide your annual interest by the number of payments you will make in a year. The resulting number is your periodic interest rate. Periodic interest rates are used to calculate monthly or semimonthly loan payments.

Enter the loan term

You can calculate a loan’s monthly payment or the total amount you will pay over the life of the loan using Microsoft Excel or a financial calculator. To calculate a loan payment, use the PV, or present value, function. To calculate the total cost of a loan, use the FV, or future value, function. You will need to know the interest rate, loan amount and length of the loan in order to use either function.

Open Microsoft Excel and create a new spreadsheet by clicking on “File” and then “New.” Click on the “Formulas” tab at the top of the screen and then scroll down to find either the PV or FV function.

Click on cell A1 and type “Interest Rate.” Click on cell A2 and type “Loan Term.” Click on cell A3 and type “Loan Amount.” These column headers will make it easier for you to enter your data into the spreadsheet.

Enter your loan’s interest rate into cell B1. This is the annual percentage rate you will be paying on your loan. For example, if your interest rate is 6 percent, you would enter “6” into cell B1.

Enter your loan term into cell B2. This is how long you have to pay back your loan in months. For example, if you have a 30-year mortgage, you would enter “360” into cell B2 for 360 months. If you have a car loan for five years, you would enter “60” into cell B2 for 60 months.

Enter your loan amount into cell B3. This is how much money you are borrowing from the lender. Do not enter commas when entering large numbers; just enter the digits without any punctuation marks

Calculate the monthly payment

The first step is to calculate the monthly payment. To do this, you need to know the loan amount, the interest rate, and the term of the loan. The loan amount is the total amount you borrowed from the lender. The interest rate is the cost of borrowing money from the lender, expressed as a percentage. The term is the length of time you have to repay the loan, expressed in months.

To calculate the monthly payment, you will need to use an equation that takes into account all three of these factors. The most common equation used is called the “PITI” equation, which stands for “principal, interest, taxes, and insurance.”

The PITI equation looks like this:

PITI = Principal + Interest + Taxes + Insurance

In this equation, “principal” refers to the loan amount, “interest” refers to the interest rate, “taxes” refers to any property taxes that may be included in your monthly payment, and “insurance” refers to any private mortgage insurance (PMI) that may be required by your lender.

To calculate your monthly payment using this equation, you will need to know your loan amount, interest rate, term (in months), and any taxes or insurance that may be included in your payment. Once you have all of this information, plug it into the equation and solve for your monthly payment.

Conclusion

Now that you know how to calculate a loan, you can use this information to make smart decisions about borrowing money. Remember to shop around for the best interest rates and terms before you sign any loan documents.