How Long Does a Hard Inquiry Stay on Your Credit Report?

Contents

A hard inquiry stays on your credit report for 24 months, but its effect on your score decreases over time.

Checkout this video:

How Long Does a Hard Inquiry Stay on Your Credit Report?

A hard inquiry is an inquiry into your credit report by a potential lender or creditor. Hard inquiries can stay on your credit report for up to two years, but they only affect your credit score for the first year.

What is a hard inquiry?

A hard inquiry is a type of credit check that occurs when you apply for a loan or credit card. Hard inquiries can lower your credit score and stay on your credit report for up to two years.

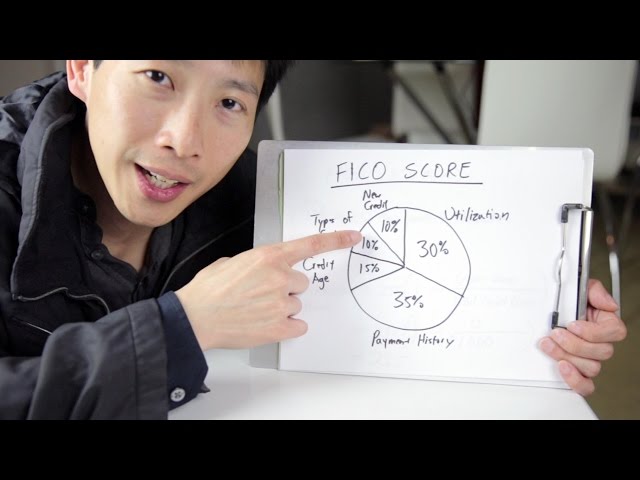

When lenders check your credit before approving a loan, they’re looking at many factors, including your payment history, credit utilization, and length of credit history. They also look at the types of credit you have, such as revolving (credit cards) or installment (loans).

Hard inquiries are just one factor that can impact your credit score. If you’re concerned about hard inquiries on your report, you may want to check your free annual credit reports for accuracy, dispute any errors you find, and consider ways to build positive credit history.

How long does a hard inquiry stay on your credit report?

Hard inquiries stay on your credit report for two years but only impact your credit for the first year. This is because your score is determined, in part, by how many recent inquiries you have. After 12 months, hard inquiries fall off your credit report and no longer impact your score.

If you’re trying to get a mortgage, auto loan or new credit card, you may be wondering how long hard inquiries stay on your credit report—and how much they’ll affect your score.

What is a hard inquiry?

A hard inquiry is placed on your report when you apply for new credit and a lender checks your credit as a part of their approval process. These are also known as “hard pulls” and can be done by creditors, landlords, employers and insurers.

How long do hard inquiries stay on my credit report?

Hard inquiries stay on your credit report for 24 months but only impact your score for 12 months. Anytime you check your own credit or rate shop for a loan within that 14-month period, those checks won’t count as a hard inquiry—so checking your own rate cards for new loans shouldn’t hurt your scores.

How can you remove a hard inquiry from your credit report?

Unfortunately, you can’t really do anything to remove a hard inquiry from your credit report. It will stay on your report for up to two years, but it will only affect your credit score for the first year. Hard inquiries are only a small factor in your credit score, so don’t worry too much about them.

The Impact of a Hard Inquiry on Your Credit Score

When you apply for a new credit card, loan, or line of credit, the lender will likely do a hard pull of your credit report. This can temporarily lower your credit score by a few points. But how long does a hard inquiry stay on your credit report? And what can you do to remove it?

How does a hard inquiry affect your credit score?

There are two types of inquiries that can happen on your credit report — hard and soft. A hard inquiry is when a lender checks your credit to decide whether to approve you for a loan or credit card. These are also called hard pulls. A soft inquiry is when you or someone else checks your credit, and it doesn’t have any effect on your score. Hard inquiries can stay on your report for up to two years, but they usually only affect your score for the first year. They also only count as a single inquiry when your score is calculated.

What is a good credit score?

A credit score is a number that reflects the creditworthiness of an individual, or how likely they are to repay a loan. A good credit score is typically above 700. Scores can range from 300 to 850, and the higher the score, the better.

A hard inquiry is when a lender checks your credit report to determine whether or not you are a good candidate for a loan. Hard inquiries can negatively impact your credit score, but only for a short period of time – usually around 12 months.

If you have a good credit score, you will likely be approved for loans with lower interest rates and better terms. This can save you money in the long run.

It is important to shop around for loans before applying, so that you can compare offers and choose the best one for your needs.

How can you improve your credit score?

There are a number of things you can do to improve your credit score, including paying your bills on time, keeping a good credit history, and using a credit monitoring service. One thing you may not know is that a hard inquiry can actually impact your score.

A hard inquiry is when a lender requests your credit report in order to make a lending decision. This could be for a new credit card, a car loan, or a mortgage. Each time a lender makes this request, it will show up on your report as an inquiry.

Inquiries can stay on your report for up to two years, but they will have the biggest impact on your score in the first year. After that, their impact will lessen over time. If you are trying to improve your credit score, it’s important to avoid hard inquiries whenever possible.

How to Avoid a Hard Inquiry on Your Credit Report

A hard inquiry is when a lender checks your credit report when you apply for a loan or credit card. Hard inquiries can stay on your credit report for up to two years, but they usually only affect your credit score for the first year. You can avoid a hard inquiry by not applying for new credit cards or loans.

What are some common causes of hard inquiries?

There are a few common scenarios that can lead to a hard inquiry:

1. You apply for a new credit card.

2. You apply for a new loan, such as a mortgage or auto loan.

3. You open a new account with a utility company or cell phone provider.

4. You rent a car, sign up for a gym membership, or start service with a new cable or satellite TV provider.

5. A lender does a periodic review of your account and conducts a hard inquiry as part of that review.

How can you avoid a hard inquiry on your credit report?

If you are planning to apply for a loan or a new credit card, you may be able to avoid a hard inquiry on your credit report by applying for a “pre-approved” offer instead. With a pre-approved offer, the lender has already decided that you are a good candidate for credit and is willing to extend an offer to you without doing a hard pull on your report.

If you are not able to get a pre-approved offer, you can still avoid a hard inquiry by asking the lender to do a “soft pull” instead. A soft pull will not show up on your credit report and will not impact your score. The lender may still do a hard pull if you decide to move forward with the loan or credit card, but at least you will have avoided the inquiry if you are not approved.

It is also worth noting that some lenders may do a hard pull on your credit report even if you have been pre-approved for an offer. This is more common with loans than with credit cards, but it is always best to check with the lender before applying to make sure that they will not do a hard pull on your report.

How can you dispute a hard inquiry on your credit report?

If you find a hard inquiry on your credit report that you don’t recognize, you can dispute it with the credit bureau. Once you file a dispute, the credit bureau will investigate and determine whether the hard inquiry is valid. If they find that it’s not valid, they’ll remove it from your credit report.