How to Finance Your New Macbook

Contents

- How to finance your new Macbook

- How to save money when financing your new Macbook

- How to get the best financing deal on your new Macbook

- How to use credit cards to finance your new Macbook

- How to finance your new Macbook with bad credit

- How to get 0% financing on your new Macbook

- How to finance your new Macbook with AppleCare

- How to trade in your old Macbook to finance your new one

- How to get discounts on your new Macbook when financing

- How to find the best financing options for your new Macbook

Follow these guidelines to help you finance your new MacBook so you can enjoy all the features without breaking the bank.

Checkout this video:

How to finance your new Macbook

There are a few different ways that you can finance your new Macbook. You can either pay for it in full upfront, or you can finance it over a period of time with a loan or through a leasing agreement.

If you decide to finance your Macbook, one option is to take out a personal loan from a bank or other lending institution. The interest rate on personal loans can vary, so be sure to shop around for the best deal before you decide on a lender. Another option is to lease your Macbook from an authorized Apple dealer. Leasing typically requires a down payment and monthly payments over the term of the lease, which is usually two to three years.

No matter which financing option you choose, be sure to read the terms and conditions carefully before you agree to anything. By understanding the fine print, you can avoid any unwanted surprises down the road.

How to save money when financing your new Macbook

There are a few things to consider when financing your new Macbook. The biggest factor is the price of the computer itself. You’ll also want to consider the interest rate and terms of the loan, as well as any fees associated with the loan.

One way to save money when financing your new Macbook is to take advantage of special financing offers from major retailers. These offers usually come with 0% interest for a certain period of time, which can help you save on interest payments. Another way to save money is to get a loan from a credit union or bank, which may offer lower interest rates than retail financing offers.

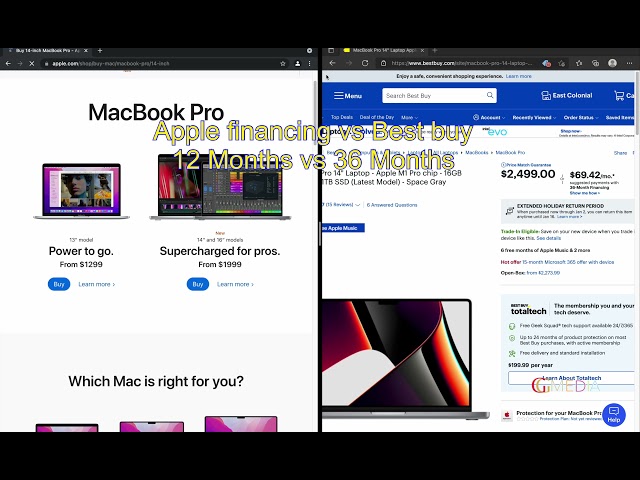

How to get the best financing deal on your new Macbook

When it comes to financing your new Macbook, you have a few different options. You can pay for it in full up front, finance it through Apple, or finance it through a third-party lender.

If you’re looking to get the best deal on financing, your best bet is to finance through a third-party lender. This way, you can shop around for the best interest rate and terms.

When you’re ready to finance your new Macbook, be sure to compare interest rates and terms from a few different lenders before you choose one. This way, you can make sure you’re getting the best deal possible.

How to use credit cards to finance your new Macbook

If you’re looking to finance your new Macbook, there are a few things you should know. First of all, using a credit card is one of the most common ways to finance a big purchase. This is because it’s a quick and easy way to get the money you need, and it can also help you build your credit score.

There are a few things to keep in mind when using a credit card to finance your new Macbook. First of all, you’ll need to make sure that you have a good credit score. This is because the better your credit score, the more likely you are to be approved for a credit card with a low interest rate. If you don’t have a good credit score, you may still be able to get approved for a credit card, but you’ll likely have to pay a higher interest rate.

Another thing to keep in mind is that you’ll need to make sure that you can afford the monthly payments on your credit card. This is because if you can’t afford the monthly payments, you’ll end up with late fees and interest charges that can quickly add up.

Once you’ve taken these things into consideration, it’s time to start shopping around for the best credit card for financing your new Macbook. There are a few things you should look for when searching for the best credit card. First of all, you’ll want to find a card with 0% APR financing for 12 months or more. This will allow you to finance your purchase without having to pay any interest charges.

You’ll also want to find a card with no annual fee. This will help save you money in the long run by not having to pay an additional fee every year just for using the card. Finally, be sure to read through all of the fine print before applying for any credit cards so that you know exactly what fees and charges will apply.

How to finance your new Macbook with bad credit

If you have bad credit, you may think that you won’t be able to finance a new Macbook. However, there are a few options available to you.

One option is to take out a personal loan from a lending institution. This can be a good option if you have good credit and can get a low interest rate.

Another option is to use a credit card with a 0% APR promotional period. This means that you won’t have to pay any interest on your purchase for a certain amount of time. Just be sure to make your payments on time and in full so that you don’t accrue any interest charges.

You could also try peer-to-peer lending. With this option, you can borrow money from individuals rather than institutions. This can be a good option if you have bad credit but can get a lower interest rate than with a personal loan from a bank.

Whatever option you choose, be sure to do your research and compare interest rates before taking out any loans.

How to get 0% financing on your new Macbook

If you’re looking to buy a new Macbook, you may be able to get 0% financing on your purchase. Here’s what you need to know.

When you buy a new Macbook, you can choose to finance your purchase with Apple. If you do this, you’ll be able to make monthly payments on your Macbook and pay no interest on your purchase. This can be a great way to spread out the cost of your new Macbook over time.

To take advantage of this offer, you’ll need to have good credit. Apple will check your credit history before approving you for financing. If you have poor credit, you may not be able to get 0% financing on your Macbook.

If you’re interested in getting 0% financing on your new Macbook, be sure to check out Apple’s financing options when you’re ready to make your purchase.

How to finance your new Macbook with AppleCare

If you’re looking to purchase a new MacBook, you may be considering financing options to help make the payments more manageable. One option is to finance your purchase through AppleCare, which offers monthly financing for Apple products. Here’s what you need to know about how this option works.

AppleCare offers 24-month financing for all new MacBooks, allowing you to spread the cost of your purchase over two years. To finance your MacBook through AppleCare, you’ll need to provide some basic information and decide on a monthly payment amount that fits within your budget. Once approved, you’ll be able to complete your purchase and start making monthly payments.

One important thing to note about financing through AppleCare is that if you decide to cancel your service or return your MacBook within the first 14 days, you’ll be required to pay the full amount financed plus any applicable interest charges. So be sure that you’re certain about your decision before moving forward with this option.

If you’re looking for a way to finance your new MacBook, AppleCare’s financing option is worth considering. Be sure to weigh all of your options and understand the terms of the agreement before making a final decision.

How to trade in your old Macbook to finance your new one

Although Macbooks are not cheap, there are a few ways that you can finance your new computer. One option is to trade in your old Macbook. Trading in your old Macbook can give you a discount on your new one, and if you have a newer model, you may be able to get a significant amount of money back.

Another option for financing your new Macbook is to take out a loan. There are many lenders who offer loans specifically for the purchase of a new Macbook. These loans usually have low interest rates and flexible repayment terms, so you can find one that fits your budget and needs.

If you have good credit, you may also be able to qualify for 0% financing from Apple itself. This means that you can finance your new Macbook with no interest for a certain period of time, which can save you a lot of money in the long run.

No matter how you choose to finance your new Macbook, be sure to do your research and compare offers before making a decision. By taking the time to shop around, you can ensure that you get the best deal possible on your new computer.

How to get discounts on your new Macbook when financing

If you’re looking to finance your new MacBook, there are a few options available to you. You can choose to finance through Apple, through your credit card provider, or through a third-party lender. Each option has its own benefits and drawbacks, so it’s important to compare them before making a decision.

Apple offers financing for MacBooks through its Apple Card program. You’ll get 0% interest for 24 months if you qualify, and there’s no annual fee. However, you will need to have good credit to qualify, and you’ll be charged late fees if you miss a payment.

Credit card providers usually offer 0% interest financing for 12-18 months on new purchases. This can be a great option if you have good credit and can pay off the balance within the promotional period. However, if you carry a balance after the promotional period ends, you’ll be charged interest at the card’s standard rate, which is often quite high.

Third-party lenders like Affirm and Klarna offer financing for online purchases at a fixed APR of typically around 10-30%. This can be a good option if you don’t have good credit or if you want to spread out the cost of your purchase over time. However, you’ll need to make sure that you can afford the monthly payments, as missed payments can damage your credit score.

How to find the best financing options for your new Macbook

When you’re ready to buy a new Macbook, the first thing you need to do is figure out how you’re going to finance it. There are a few different options available, and the best one for you will depend on your budget and your financial goals.

One option is to pay for your Macbook outright with cash. This is the simplest and most straightforward way to finance your purchase, but it may not be feasible for everyone. If you can’t afford to pay for your Macbook in full, you may want to consider financing it with a personal loan.

Personal loans can be obtained from banks, credit unions, and online lenders. The interest rate on a personal loan will vary depending on the lender, but it will typically be lower than the interest rate on a credit card. Personal loans also have fixed interest rates, so you’ll know exactly how much your monthly payments will be.

Another option for financing your new Macbook is to use a credit card. Credit cards usually have higher interest rates than personal loans, but they also offer reward points or cash back that you can use to offset the cost of your purchase. Just be sure to pay off your balance in full each month so that you don’t rack up any unnecessary debt.

No matter which financing option you choose, be sure to shop around and compare rates before making a decision. The last thing you want is to end up with an expensive monthly payment that you can’t afford.