What is a Grace Period on a Credit Card?

If you’re new to credit cards, you may be wondering what a grace period is. A grace period is the time between the end of your billing cycle and when your payment is due. During this time, you can avoid paying interest on your purchases by paying your balance in full.

Checkout this video:

Understanding Grace Periods

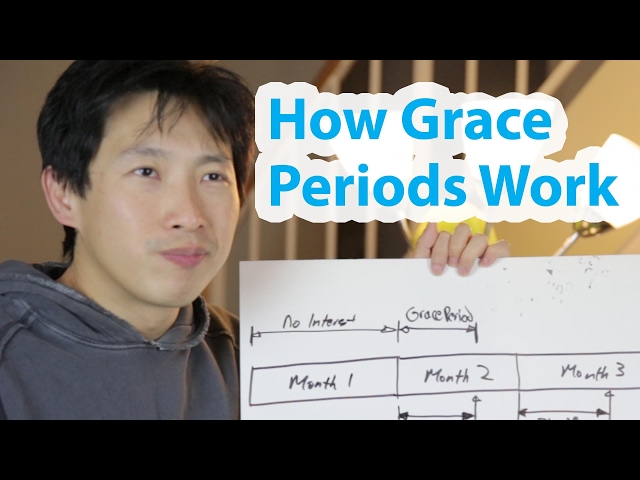

A grace period is the interest-free period that cardholders have on new purchases before interest is applied to the balance. In other words, if you pay your balance in full and on time each month, you won’t have to pay any interest on your new purchases. Grace periods typically last between 21 and 25 days.

What is a grace period?

A grace period is the time you have to pay your credit card bill in full before interest is applied to the outstanding balance. Most grace periods are at least 21 days long, but some extend up to 25 days. If you carry a balance from one month to the next, you’ll lose your grace period and be charged interest on your average daily balance—including new purchases—from the date each purchase is made.

The best way to avoid paying interest is to pay off your credit card bill in full and on time every month. Or, if you can’t pay the entire balance, try to pay as much as possible so you’ll owe less when the grace period ends.

How long is a grace period?

A grace period is the time between the end of a billing cycle and when your credit card issuer starts charging interest on your balance. Typically, this interval lasts about 20 to 25 days. If you pay your balance in full and on time during the grace period, you won’t be charged any interest on that balance.

There are a few things to keep in mind about grace periods:

1. not all credit card issuers offer them

2. some cards only offer a grace period on purchases, not cash advances or balance transfers

3. if you’re late with a payment, you may lose your grace period for the next billing cycle

4. your grace period may be shorter if you have a promotional APR

If you’re not sure whether your card has a grace period or how long it is, contact your issuer for more information.

What purchases are not covered under a grace period?

There are a few types of transactions that are not subject to a grace period, including balance transfers and cash advances. That means any interest will accrue from the date of the transaction. In addition, most issuers also exclude any fees associated with these transactions from the grace period.

Purchases made during the grace period are not subject to interest as long as you pay your balance in full by the due date. If you carry a balance on your card from month to month, interest will be charged on any new purchases starting on the date of the transaction, even if you’ve paid your previous balance in full.

Grace periods also do not apply if you have been late with a payment or if you have gone over your credit limit. In these cases, any new purchases will be subject to interest charges immediately.

Advantages of a Grace Period

A grace period is the length of time between the end of a billing cycle and when your payment is due. Grace periods give cardholders time to pay their bill without incurring interest. Most credit cards have a 21-day grace period, which means cardholders have 21 days to pay their bill before interest is applied. Having a grace period can be beneficial because it allows cardholders to avoid paying interest on their purchases.

Avoid paying interest

When you carry a balance on your credit card from month to month, you will be charged interest on that balance. However, most credit cards offer a grace period during which no interest will be charged on new purchases. The grace period typically lasts 21 to 25 days and begins on the first day of your billing cycle. If you pay your balance in full before the end of the grace period, you will avoid paying interest on your new purchases.

The grace period only applies to new purchases, not to balances carried over from previous months. If you have a balance on your credit card at the beginning of your billing cycle, you will be charged interest on that balance from the first day of the billing cycle, even if you pay it off in full before the end of the grace period.

To take advantage of the grace period and avoid paying interest charges, you need to make sure that you pay your balance in full each month. This can be difficult if you only make the minimum payment each month, as it may not be enough to completely pay off your balance before the end of the grace period. One way to avoid this problem is to make a payment that is large enough to cover both your current month’s purchases and any remaining balance from previous months, so that your account has a zero balance at the beginning of each new billing cycle.

More time to pay off your balance

When you’re approved for a credit card, you’re typically given a grace period of at least 21 days to pay your balance in full without accruing interest. The grace period is the time between the end of your billing cycle and when your payment is due. If you pay your balance in full and on time each month, you’ll avoid paying interest on your purchases.

Some credit cards offer a grace period on balance transfers and cash advances as well, but this isn’t always the case. Be sure to check with your issuer to see if there’s a grace period on these types of transactions. There also may be special rules or conditions that must be met in order for the grace period to apply.

Here are a few things to keep in mind about credit card grace periods:

-Not all credit cards offer one. If yours doesn’t, you’ll start accruing interest on your purchases as soon as they post to your account.

-Grace periods only apply if you carry a balance from month to month. If you pay your balance in full and on time each month, you won’t have to worry about accruing interest.

-The length of your grace period may vary depending on the type of purchase you make. For example, some issuers may give you more time to pay off cash advances than they do for regular purchases.

-If you’re late with a payment, you may lose your grace period for future purchases.

-Your due date may not be the same as the end of your billing cycle. Be sure to check with your issuer to find out when your payment is due each month.

Build credit history

One of the primary advantages to having a grace period is that it allows cardholders to build a good credit history. A grace period is the set amount of time between the end of a billing cycle and when the card issuer starts charging interest on the account. For example, if your card issuer offers a 25-day grace period and your billing cycle ends on June 10, you will have until July 5 to pay your balance in full before interest is applied.

Assuming you make all of your payments on time and in full, having a grace period can help you build a strong credit history. That’s because paying your balance in full and on time each month is one of the key factors that make up a good credit score. When you don’t have a grace period, it’s easier to carry a balance from month-to-month, which can hurt your credit scores.

Disadvantages of a Grace Period

A grace period is the period of time between the end of a billing cycle and when the credit card issuer charges interest on the balance. If you carry a balance on your credit card from one month to the next, you will be charged interest on that balance, even if you pay your bill on time. The grace period is the time when you can avoid paying interest on your credit card balance.

You may still be charged interest

If you don’t pay your balance in full during the grace period, you will be charged interest on your average daily balance—including any new purchases you made during the billing cycle—from the date each purchase was made.

You may be charged a late fee

If you don’t pay your credit card bill in full by the due date, you will likely be charged a late fee. The fee may be a flat rate, such as $25, or it may be a percentage of your outstanding balance, such as 5%.

Your credit card issuer may also increase your interest rate if you pay your bill late. This is called a penalty APR, and it can apply to both new purchases and existing balances. The penalty APR can be as high as 29.99%, so it’s important to pay your bill on time to avoid this costly mistake.

If you have a history of making late payments, your credit card issuer may close your account and report the account closure to the credit bureaus. This will damage your credit score and make it harder to get approved for new credit products in the future.

Your credit score could be impacted

If you’re thinking about using a grace period on your credit card, it’s important to understand how it could affect your credit score. A grace period is the time between when your credit card bill is due and when late fees begin to accrue. Grace periods typically last between 21 and 25 days, but they can vary depending on your particular card issuer.

There are a few ways that using a grace period could impact your credit score. First, if you consistently carry a balance from one month to the next, you may be charged interest on that balance even during the grace period. Second, paying only the minimum amount due each month can hurt your credit score because it will increase your credit utilization ratio, which is the percentage of your available credit that you’re using. Finally, if you’re late on a payment or miss a payment entirely, that late payment will be reported to the credit bureaus and will damage your credit score.

If you’re considering using a grace period on your credit card, be sure to weigh the potential risks and benefits carefully. Although a grace period can give you some extra time to pay your bill, it’s important to remember that it could also have a negative impact on your credit score.