How Does an Unsubsidized Loan Work?

Contents

If you’re considering taking out a student loan , you may be wondering how an unsubsidized loan works. Here’s a quick rundown of what you need to know.

Checkout this video:

What is an unsubsidized loan?

An unsubsidized loan is a type of financial aid that you have to pay back, with interest. Unlike a subsidized loan, the government does not pay the interest on your loan while you’re in school or during other periods of deferment.

With an unsubsidized loan, you’re responsible for all the interest that accrues on your loan from the time the loan is first disbursed (paid out) until it’s paid in full. If you choose not to pay the interest while you’re in school and during other periods of deferment, it will be added to your loan principal (the amount you borrowed), and you’ll have to pay interest on that larger amount when you enter repayment. This is called capitalization.

How do unsubsidized loans differ from subsidized loans?

The main difference between subsidized and unsubsidized loans is that the government pays the interest on subsidized loans while the borrower is in school, during the grace period, and during deferment periods. With unsubsidized loans, the borrower is responsible for all interest that accrues on the loan.

How do unsubsidized loans work?

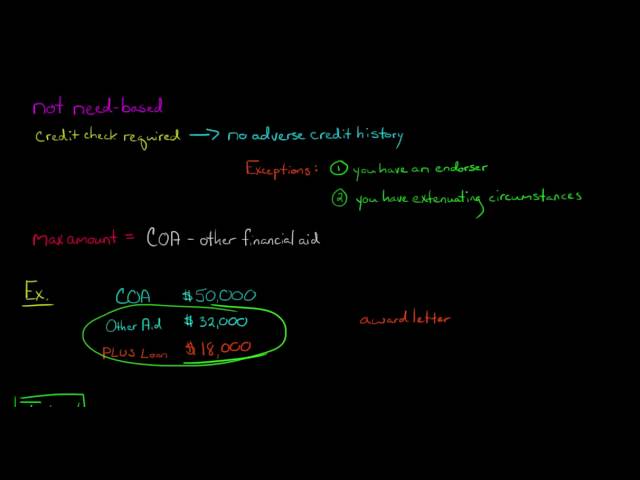

An unsubsidized loan is a type of financial aid that you have to pay back. With an unsubsidized loan, you’re responsible for paying the interest even while you’re in school. Unsubsidized loans are not need-based, which means that anyone can qualify for one, regardless of their financial circumstances.

There are two types of unsubsidized loans: direct unsubsidized loans and indirect unsubsidized loans. Direct unsubsidized loans are issued by the federal government, while indirect unsubsidized loans are issued by private lenders.

Both types of loans have the same terms and conditions, including a fixed interest rate and a grace period. The grace period is the time after you graduate, leave school, or drop below half-time enrollment before you have to start repaying your loan.

With a direct unsubsidized loan, the federal government pays the interest while you’re in school and during your grace period. With an indirect unsubsidized loan, you’re responsible for paying the interest from the time the loan is disbursed until it’s paid in full.

If you don’t pay the interest on an unsubsidized loan, it will be added to your principal balance (capitalization). This will increase the amount of interest you have to pay over the life of the loan.

What are the benefits of an unsubsidized loan?

An unsubsidized loan is a type of financial aid that you have to pay back with interest. Unlike a subsidized loan, the interest on an unsubsidized loan starts accruing as soon as the loan is disbursed.

The benefits of an unsubsidized loan include:

-You are not required to make interest payments while you are in school or during grace periods and deferment or forbearance periods.

-The interest that accrues on your unsubsidized loan may be tax-deductible.

-You can choose to make interest payments while you are in school, which will lower the amount of interest that accrues and save you money in the long run.

What are the drawbacks of an unsubsidized loan?

There are a few drawbacks to an unsubsidized loan. The first is that you will accrue interest on the loan while you are still in school. This can add up quickly and cause the amount you owe to increase significantly. The second drawback is that unsubsidized loans are not need-based, which means that you may end up with a higher interest rate than you would with a subsidized loan.