How Does Credit Utilization Affect Your Credit Score?

Contents

Credit utilization is one of the most important factors in your credit score. It’s a measure of how much of your available credit you’re using at any given time, and it can have a big impact on your score.

In this blog post, we’ll take a look at how credit utilization works and how it can affect your credit score. We’ll also provide some tips on how you can keep your credit utilization low and improve your credit score.

Checkout this video:

What is credit utilization?

Credit utilization is the amount of credit you’re using compared to the amount of credit you have available. Put more simply, it’s how much debt you’re carrying in relation to your credit limits. For example, if you have a $5,000 credit limit and a balance of $2,500, your credit utilization is 50%.

Credit utilization is one factor that makes up your credit score—the higher your balances are in relation to your credit limits, the lower your score will be. That’s because high credit utilization signals to lenders that you may be at a higher risk of defaulting on your debt obligations.

There are a few different ways to lower your credit utilization ratio:

– Pay down your balances: This will immediately lower your ratio and can help improve your score over time.

– Request a credit limit increase: If you have a good payment history and low balances relative to your current limits, you may be able to get approved for a higher credit limit. This will also lower your credit utilization ratio.

– Keep balances low on revolving accounts: If you can’t pay down your balances completely, try to keep them below 30% of your credit limits. This will help improve your score over time.

Credit utilization is just one factor that makes up your credit score—but it’s an important one. By keeping an eye on your ratio and taking steps to lower it if necessary, you can help improve your score and make yourself a more attractive borrower to lenders.

How does credit utilization affect your credit score?

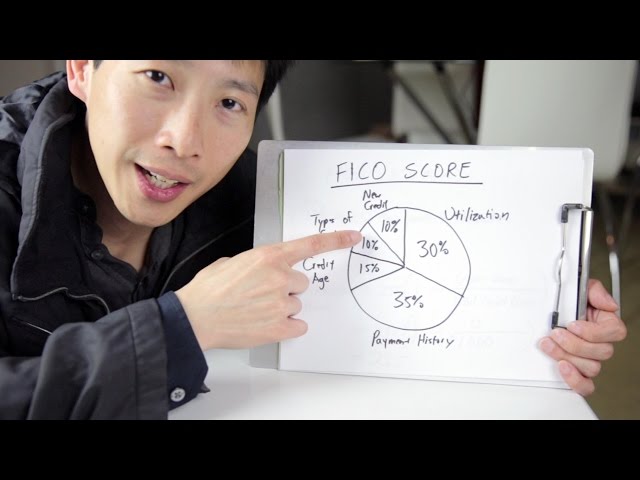

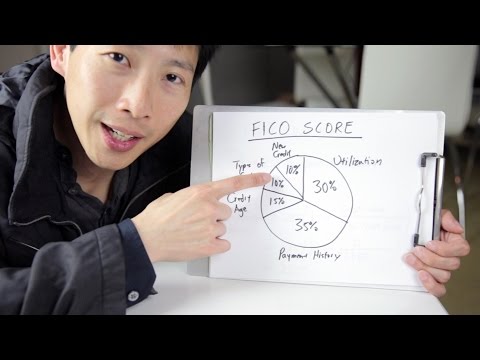

Credit utilization is one of the most important factors in your credit score. It’s a measure of how much of your available credit you’re using, and it makes up 30% of your FICO® Score.

Here’s how it works: A high credit utilization ratio (meaning you’re using a lot of your available credit) can hurt your credit score. That’s because it signals to potential lenders that you might be struggling to pay your bills. On the other hand, a low credit utilization ratio indicates that you’re using a small portion of your available credit and could handle more debt responsibly. Lenders like to see this, so it can help boost your score.

To keep your credit utilization low, aim to use no more than 30% of your total credit limit on any one card. If you have multiple cards, try to keep your overall utilization below 30%.

Paying off debt is one way to lower your credit utilization ratio. Another option is to ask for a higher credit limit from your issuer. This will instantly lower your utilization ratio without affecting how much debt you actually have. Just remember: Don’t close any old accounts or open new ones just to get a higher limit. These actions could hurt your score in the long run.

What is a good credit utilization ratio?

Credit utilization is the amount of revolving credit you have used divided by the total amount of revolving credit you have available, and is one factor that makes up your credit score.

A good credit utilization ratio is generally below 30%, with anything above that being considered potentially harmful to your credit score. A higher percentage of credit utilization may hurt your credit score because it could indicate to lenders that you’re relying too heavily on credit, which could make you a higher-risk borrower.

How can you lower your credit utilization ratio?

Credit utilization is one of the most important factors in your credit score. Your credit utilization ratio is the amount of revolving credit you are using divided by the total amount of revolving credit you have available to you. For example, if you have a $1,000 balance on a credit card with a $5,000 limit, your credit utilization ratio is 20%.

If your goal is to lower your credit utilization ratio, there are a few different ways you can do it. One way is to simply pay down your balances. If you have multiple credit cards with balances, focus on paying down the card with the highest balance first. Another way to lower your credit utilization ratio is to ask for a higher limit on your credit cards. If your card issuer agrees to raise your limit, that will immediately lower your credit utilization ratio. Finally, you can open new lines of credit to increase the amount of available credit you have and lower your credit utilization ratio.

Whatever method you choose to lower your credit utilization ratio, be sure to do it gradually. A sudden drop in your ratio could be viewed negatively by the credit scoring companies and could cause your score to go down.

How often is your credit utilization ratio updated?

Your credit utilization ratio is the second most important factor in your credit score, and it’s important to keep it as low as possible. But how often is your credit utilization ratio updated?

The answer is: it depends.

If you have a revolving line of credit, such as a credit card, your credit utilization ratio is updated every time you make a purchase. If you have a static line of credit, such as an installment loan, your credit utilization ratio is updated once per month.

For most people, the biggest factor in their credit utilization ratio is their credit card balance. If you have abalance of $2,000 and a credit limit of $5,000, your credit utilization ratio is 40%.

Your goal should be to keep your credit utilization ratio below 30%, and ideally below 10%. The lower your credit utilization ratio, the better it is for your credit score.

What other factors affect your credit score?

Your credit score is a number that represents your creditworthiness. It is used by lenders to determine whether you qualify for a loan and, if so, what interest rate you will pay. It is also used by landlords to decide whether to rent to you and by utility companies to decide whether to require a deposit.

There are many factors that contribute to your credit score. Payment history is the most important factor, accounting for 35% of your score. This means that paying your bills on time, every time is the best way to improve your credit score. The next most important factor is credit utilization, which accounts for 30% of your score. This means that using less of your available credit will improve your score. Other important factors include the types of credit you have (10%), the length of your credit history (15%), and any new credit lines or inquiries (10%).