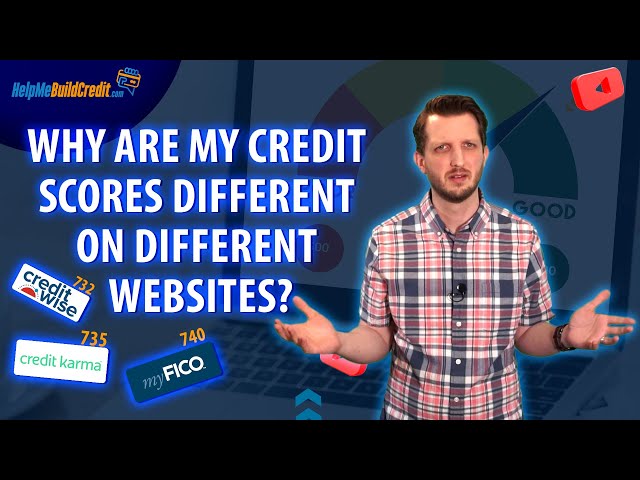

Why Is My Credit Score Different on Different Sites?

Contents

A credit score is a numerical expression based on a level analysis of a person’s credit files, to represent the creditworthiness of an individual.

Checkout this video:

The Different Types of Credit Scores

There are many different credit scoring models in the industry. Each model produces a slightly different score, which is why your score may be different on different sites. The most important thing is to focus on the factors that impact your score the most. This section will cover the different types of credit scores and why they differ.

FICO Score

FICO scores are the most common type of credit score and are used by 90% of lenders. FICO scores range from 300 to 850, with the average score being 723. Scores above 700 are considered good, while scores below 620 are considered bad.

There are three different types of FICO scores: base, industry-specific, and custom. Base FICO scores are the most common type of score and are used by 90% of lenders. Industry-specific FICO scores are used by specific lenders to assess risk in specific industries. Customized or secret FICO scores are developed by lenders for their own internal use and are not available to consumers.

Your credit score may be different on different sites because each site may use a different scoring model or may be using a custom or industry-specific score that is not available to consumers.

VantageScore

VantageScore is a credit scoring model developed jointly by the three major national credit bureaus: Experian, Equifax, and TransUnion. It’s now the most widely used scoring model, as all three of those bureaus use it to generate credit scores for their own customers.

The VantageScore model ranges from 300 to 850, just like the FICO score. But there are some key differences in how it’s calculated. For one thing, the VantageScore doesn’t give as much weight to paid-off debt; instead, it focuses on current debt and recent credit activity. It also doesn’t penalize you quite as much for having a few missed payments or other dings on your credit report.

That said, the two scoring models are similar enough that a high VantageScore will generally get you the same results as a high FICO score—and a low score will tend to have the same consequences. So if you’re trying to improve your credit score, it’s helpful to track both your VantageScore and your FICO score over time to see how your efforts are paying off.

The Different Credit Reporting Agencies

There are three main credit reporting agencies in the U.S.(Equifax, TransUnion, and Experian). They all use different algorithms to calculate your credit score. That’s why your credit score may be different on different sites. Each credit reporting agency has its own method for calculating your credit score.

Experian

Experian is a consumer credit reporting agency. Experian collects and aggregates data on more than 220 million individual consumers in the United States and over 800 million globally. The company then uses this information to produce credit reports, which are sold to businesses for the purposes of extending credit, monitoring creditworthiness, and detecting fraud. Experian also maintains a file on each consumer that includes information such as credit history, public record information, and Inquiries.

Equifax

Equifax is one of the three major credit reporting agencies in the United States, along with Experian and TransUnion. Headquartered in Atlanta, Georgia, Equifax maintains files on over 820 million consumers and more than 91 million business entities worldwide.

Equifax generates revenue through the sale of its data products, including credit reports, credit scores, and other analytics. The company also provides a suite of business services, such as marketing solutions, human resources management, and risk management.

While Equifax is best known for its consumer credit products, the company has been investing heavily in its business solutions division in recent years. In 2016, Equifax acquired human resources management software company Workforce Solutions for $700 million. In 2017, the company announced plans to acquire identity theft protection firm ID Watchdog for $63 million.

TransUnion

TransUnion is a consumer credit reporting agency. TransUnion collects and aggregates information on over one billion individuals worldwide, including more than 330 million people in the United States.

TransUnion’s US data is used by over 60,000 businesses and is lenders’ primary source for making credit decisions for more than 20 million consumers.

Why Your Score May Be Different on Each Site

Your credit score is a important number that lenders look at to decide whether or not to give you a loan and what interest rate to charge. The number is supposed to be a representation of how likely you are to repay a loan. So why then, when you check your score on different sites, are the numbers often different?

The Methodology Is Different

There are a few reasons why your credit score may differ from site to site. The first, and most important, is that each site uses a different method to calculate your score.

While the underlying data may be similar, the way that information is weighted will produce a different score. That’s why you may see a big difference between your score on one site and another.

In addition, some sites don’t use the same scoring model as the one used by lenders. So even if the methodology is similar, the actual score may not be comparable to what a lender would use when making a decision about your loan.

You May Have a Different Score With Each Agency

Your credit score is a number that represents your creditworthiness. It is based on your credit history, which is a record of how you have handled debt in the past.

There are three major credit reporting agencies in the United States: Experian, Equifax, and TransUnion. Each agency has its own method for calculating your score, so it’s not unusual for your score to be different on each site.

In addition, each site uses a different scoring model. For example, Experian uses the FICO® Score 8, while Equifax uses the BEACON® 9.0 score. And because each scoring model weights different factors differently, your score may be different on each site even if you have the same information in your credit report.

Finally, keep in mind that credit scores are meant to be used as a guide, not as a definitive measure of your creditworthiness. Lenders will also consider other factors when making lending decisions, such as your income and employment history.

The Score May Be Inaccurate

It’s not uncommon for your credit score to be different on different sites. In fact, it’s quite common. There are a few different reasons for this:

1. The scoring model used. Each site uses a different scoring model, which means that the way they calculate your score may be slightly different. This can lead to small differences in your score.

2. The credit report used. Each site uses a different credit report, which may contain slightly different information. This can also lead to small differences in your score.

3. The time the score is calculated. Your credit score can change over time, so if one site calculates your score at a different time than another site, that can lead to a difference in your score.

4. The range of scores used. Some sites use a smaller range of scores than others, which can make it appear as though your score is higher or lower than it actually is.

5. Human error. Sometimes, a site may simply make a mistake when calculating your score. This is usually not the case, but it is possible.

If you notice a big difference in your score on one site compared to another, it’s usually not cause for concern. However, if you notice that your score is consistently lower on one site than on others, it’s worth looking into to see if there is an inaccuracy that needs to be corrected

How to Check Your Credit Score

Your credit score is a numerical representation of your creditworthiness. Lenders use your credit score to determine whether you’re a good candidate for a loan and how much interest to charge you. A higher score indicates less risk to the lender, which could lead to a lower interest rate on a loan. A lower score means you’re a higher-risk borrower, which could lead to a higher interest rate.

Get a Free Credit Report

One of the best ways to check your credit score is to get a free credit report.

Each of the three main credit bureaus in the United States—Experian,TransUnion, and Equifax—is required to provide you with a free copy of your credit report once every 12 months if you request it.

You can request your free credit report from AnnualCreditReport.com, the only site authorized by federal law to provide them.

When you check your credit score on a site like CreditKarma or CreditSesame, you’re actually seeing a version of your Experian credit report. These sites use what’s called a soft inquiry to generate your score, which doesn’t impact your credit at all.

Check Your Credit Score for Free With a Credit Card

If you’re like most people, you probably don’t know your credit score off the top of your head. And you probably don’t want to spend the money to find out.

Luckily, there’s an easy way to check your credit score for free: with a credit card.

Many credit card issuers now offer their customers free access to their FICO score, which is the most widely used credit score. So if you have a credit card from Discover, Barclaycard, Citi, Chase, or American Express, you can probably check your score for free.

If your issuer doesn’t offer free FICO scores, don’t worry — there are still other ways to check your score for free. For example, some personal finance websites, like Credit Karma and NerdWallet, offer free credit scores from TransUnion and Equifax, two of the other major credit bureaus.

So why is my credit score different on different sites?

The short answer is that there are multiple types of credit scores, and each lender uses a different one when considering loan applications. That’s why you might see a slightly different number on each site — but don’t worry, they’re all in the same ballpark.

How to Improve Your Credit Score

Credit scores are important because they show how likely you are to repay a loan. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on a loan. A low credit score could lead to a higher interest rate and could mean you won’t be approved for a loan at all.

Check for and Dispute Any Inaccuracies

It’s important to check your credit reports regularly for any errors or inaccuracies. You can get a free copy of your credit report from each of the three major credit bureaus — Equifax, Experian, and TransUnion — once every 12 months at AnnualCreditReport.com. You can also get your credit score for free from several websites and lenders.

If you find any errors on your credit report, dispute them with the appropriate credit bureau. Be sure to include any supporting documentation and an explanation of why you believe the information is inaccurate. The credit bureau will then investigate and remove any inaccurate information from your report if they agree with you.

Make All Your Payments on Time

One important factor that is considered when calculating your credit score is your payment history—specifically, whether you have made all of your payments on time. Therefore, one of the best ways to improve your credit score is to make sure that you make all of your payments on time, including your mortgage, car loan, student loan, and credit card payments.

If you have missed any payments in the past, you can still improve your credit score by catching up on those payments as soon as possible. Additionally, if you have been consistently making all of your payments on time for a while, that positive payment history will be reflected in your credit score.

Use Credit Wisely

What is a credit score and why is it important? A credit score is a number that lenders use to evaluate your creditworthiness. It’s important because it can influence the interest rate you pay on a loan or credit card, and can even affect your ability to get a job.

There are different types of credit scores, but the most common are FICO® scores, which are used by 90% of lenders. Your FICO® score may be different on different sites because there are multiple versions of the score, and each lender may use a different version.

The best way to improve your credit score is to use credit wisely. Here are some tips:

-Pay your bills on time. This is the most important factor in your credit score.

-Keep your balances low. Your credit utilization ratio, which is the amount of debt you have relative to your credit limit, should be below 30%.

-Apply for new credit only when you need it. Every time you apply for new credit, it results in a hard inquiry on your credit report, which can temporarily lower your score.

-Monitor your report for errors and dispute any inaccuracies. You can get a free copy of your report from each of the three major credit bureaus every year at AnnualCreditReport.com