Which Is Better: Refinance or Home Equity Loan?

Contents

If you’re a homeowner, you may be wondering if a home equity loan or a refinance is the better option for you. Here’s a rundown of the pros and cons of each to help you make the best decision for your situation.

Checkout this video:

What is a home equity loan?

A home equity loan is a loan in which the borrower uses the equity of their home as collateral. Home equity loans are often used to finance major expenses such as home repairs, medical bills, or college education. A refinance is a new loan that pays off an existing loan. The main reason to refinance is to get a lower interest rate.

How does a home equity loan work?

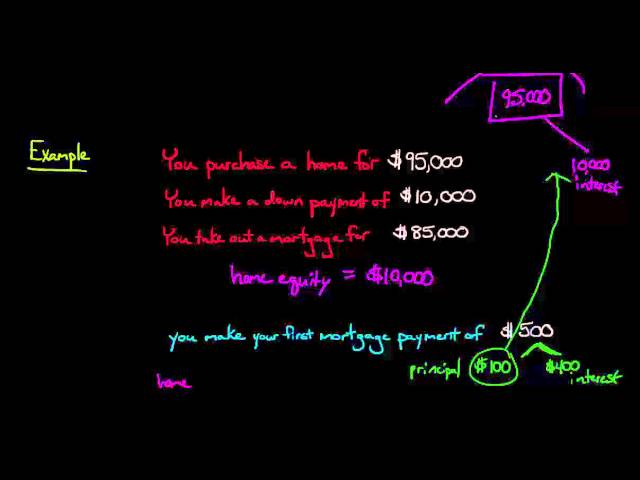

A home equity loan is a loan that uses your home as collateral. You can use the equity in your home to get a loan, using your home as collateral. Home equity loans are usually second mortgages, meaning they’re second in line to be repaid if you default on the loan. Home equity loans are usually available only if you have a considerable amount of equity in your home, often 25% or more.

If you obtain a home equity loan, you’ll receive a lump sum of cash that you can use however you like. Many people use home equity loans for large purchases such as home improvements, but you can also use the funds for other purposes such as consolidating debt or taking a much-needed vacation.

Before taking out a home equity loan, it’s important to consider the risks associated with any type of borrowing against your home. If you default on your payments, you could lose your home. Additionally, if your home value decreases, you may end up owing more than your home is worth.

What is a refinance?

A refinance is the process of taking out a new loan to pay off your old loan. This can be done for a variety of reasons, such as to get a lower interest rate, to change the term of your loan, or to access the equity in your home. A home equity loan is a loan that is secured by your home and can be used for a variety of purposes, such as home improvement, debt consolidation, or investments.

How does a refinance work?

If you have equity in your home and you need cash, you might be able to do a cash-out refinance. With a cash-out refinance, you borrow more than what you currently owe and take the difference in cash. But, there are some things to consider before you decide if this is the right move for you.

Which is better: refinance or home equity loan?

You may be able to save money by refinancing your home loan or taking out a home equity loan. Let’s compare the two options so you can decide which is best for you.

The pros and cons of a home equity loan

The Pros:

-A home equity loan is often one of the most affordable ways to finance a large project or debt consolidation.

-The interest rate is usually fixed, which means you know exactly how much your monthly payment will be.

-The repayment period is usually shorter than a traditional mortgage, which means you’ll pay less in interest over the life of the loan.

-You can typically borrow up to 80% of your home’s equity, which is the difference between your home’s appraised value and your current mortgage balance.

The Cons:

-If you don’t make your payments on time, you could lose your home to foreclosure.

-You may have to pay origination fees or closing costs, which can add to the cost of the loan.

-Your monthly payments could go up if the interest rate on your adjustable-rate home equity loan goes up.

The pros and cons of a refinance

If you’re thinking about refinancing your home, there are a few things you should consider first. There are both pros and cons to refinancing, and depending on your particular financial situation, one option may be better than the other.

The Pros of Refinancing

-You may be able to lower your interest rate: One of the main reasons people refinance is to get a lower interest rate. If you’re able to lower your interest rate even by a small amount, you could save money over the life of your loan.

-You may be able to shorten the term of your loan: Another advantage of refinancing is that you may be able to shorten the term of your loan. This could help you save money in the long run by paying off your debt faster.

-You may be able to get cash out: If you have equity in your home, you may be able to get cash out when you refinance. This could be helpful if you need money for home repairs or improvements, or if you want to consolidate other debts.

The Cons of Refinancing

-You may have to pay fees: One downside of refinancing is that there may be fees involved, such as appraisal fees, application fees, and closing costs. These fees can add up, so make sure you take them into account when considering whether or not to refinance.

-Your monthly payment could go up: Even if you lower your interest rate when you refinance, your monthly payment could still go up if you extend the term of your loan. This is something to keep in mind if you’re trying to save money each month.

-You could end up owing more money in the long run: If you don’t carefully consider all the factors involved in refinancing, you could end up owing more money than you did before. Make sure you do your research and understand all the potential risks before making a decision.

How to decide if a home equity loan or refinance is right for you

Making the decision of whether to refinance or get a home equity loan or line of credit depends on many factors. You’ll need to consider your current financial situation, as well as your goals and plans for the future.

For example, if you’re hoping to lower your monthly mortgage payments, you might want to refinance into a loan with a lower interest rate. Or, if you have a significant amount of equity in your home, you might be able to get a home equity loan or line of credit with a lower interest rate than other types of loans.

It’s also important to consider the fees associated with each type of loan. For example, refinancing typically includes closing costs such as appraisal fees, title insurance and origination fees. Home equity loans may also include closing costs, although these can sometimes be rolled into the loan.

Before making a decision, it’s important to compare offers from multiple lenders to make sure you’re getting the best deal possible.