Which Document(s) Specify the Interest Rate Being Charged for a Loan

Contents

Learn which document(s) specify the interest rate being charged for a loan.

Checkout this video:

The Note

The Note discloses the interest rate being charged for the loan. The Note will also list any fees being charged in connection with the loan, such as origination fees, discount points, and so on. The Note will also specify the repayment schedule for the loan.

The note rate is the interest rate specified in the promissory note

When you take out a loan, the interest rate you pay is determined by many factors. One of those factors is the note rate, which is the interest rate specified in the promissory note. The note rate is generally lower than the Annual Percentage Rate (APR), which is the true cost of borrowing money and includes fees and other costs associated with the loan.

The note rate may be fixed or variable. A fixed interest rate means that your payments will not change during the life of the loan. A variable interest rate means that your payments may change over time, depending on changes in an index such as the prime rate.

The term of a loan also affects your payments. A shorter term results in higher monthly payments, but you will pay less interest overall because you are borrowing money for a shorter period of time. A longer term results in lower monthly payments, but you will pay more interest overall because you are borrowing money for a longer period of time.

Your creditworthiness also affects your interest rate. If you have good credit, you will generally qualify for a lower interest rate than someone with poor credit. This is because lenders view borrowers with good credit as being less likely to default on their loans.

The Truth in Lending Statement (TIL)

The TIL is a disclosure statement that lists the cost of borrowing money. It must be provided to borrowers by lenders before consummation of the loan. The TIL must be in writing and must be signed by the borrower. The TIL is required by the Truth in Lending Act (TILA) and Regulation Z. The TIL discloses the annual percentage rate (APR) as well as other important loan terms.

The TIL must be provided to the borrower at or before consummation

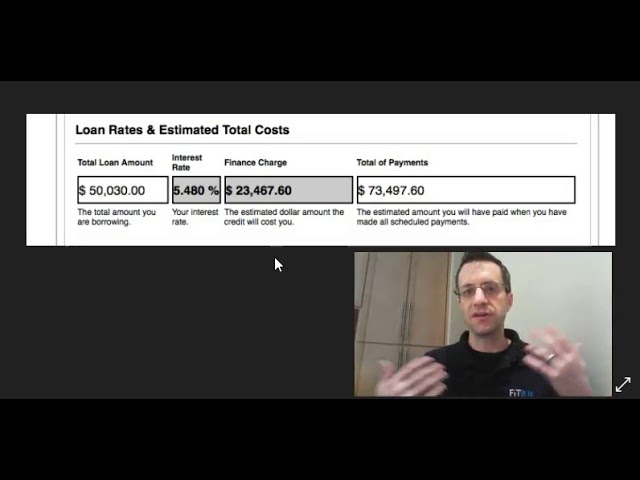

The Truth in Lending Act (TILA) requires lenders to provide borrowers with a Truth in Lending statement at or before consummation.1 The TIL discloses the annual percentage rate (APR), finance charges, and other important terms of the loan so that borrowers can comparison shop for the best deal.2

Lenders must use uniform terminology and format when disclosing the APR, which is the cost of credit expressed as a yearly rate.3 The APR includes not only the interest rate but also certain fees charged by the lender, such as points, private mortgage insurance premiums, and loan origination fees.4 Borrowers should compare APRs when shopping for a loan because this rate provides the most accurate picture of the true cost of credit.5

The finance charge is the total dollar amount of interest and other charges paid by the borrower over the life of the loan.6 Lenders must disclose the finance charge on the TIL so that borrowers can compare total costs when shopping for a loan.7

The TILA also requires lenders to provide certain other important information on the TIL, such as:

– The amount financed: This is the total amount of credit extended to the borrower minus any prepaid finance charges. 8

– The total number of payments: This is the number of periodic payments required to repay the loan in full, including any balloon payments. 9

– The payment schedule: This is a table showing how much each periodic payment will be and when it is due. 10

The TIL must disclose the APR

The TIL must disclose the APR in order to give borrowers a clear picture of the true cost of the loan. The APR includes not only the interest rate but also any points, origination fees, and other charges that may be required to get the loan. By law, lenders must give you the TIL at least 3 business days before you close on the loan.

The Mortgage or Security Instrument

The mortgage or security instrument is the document that specifies the interest rate being charged for a loan. The rate may be fixed for the life of the loan or may change periodically.

The mortgage or security instrument may specify the interest rate

The mortgage or security instrument may specify the interest rate being charged for a loan. The rate may be fixed for the life of the loan or may change periodically. If the interest rate changes, it will usually do so in accordance with an index and margin. An index is a published interest rate. The margin is a number of percentage points added to or subtracted from the index to determine the interest rate that will be charged for the loan.

The Servicing Agreement

The Servicing Agreement is a document that specifies the interest rate being charged for a loan. This document is also used to establish the payment schedule and other terms of the loan. The Servicing Agreement is between the lender and the borrower.

The servicing agreement may specify the interest rate

The servicing agreement may specify the interest rate being charged for a loan, or it may state that the interest rate is variable and will be adjusted periodically. The interest rate may also be specified in the promissory note or other loan documents.