What Percentage of Your Credit Should You Use?

Contents

If you’re like most people, you probably have a lot of questions about credit. How do I get it? How do I improve it? What percentage of my credit should I use?

Fortunately, we can help you answer that last question. According to credit experts, you should aim to use no more than 30% of your credit limit. This will help you keep your credit score high and avoid getting into debt.

So next time you’re considering a purchase, make

Checkout this video:

How much credit is too much credit?

When you’re trying to decide how much credit to use, you need to consider a few things. How much can you afford to pay back each month? What’s your credit score? What’s your credit history? The answer to these questions will help you determine how much credit is too much credit for you.

The 30% rule

The rule is simple: keep your balances on all credit cards and other revolving credit accounts, such as retail store cards, at or below 30% of your credit limit at all times. This will help you keep your credit utilization in check and improve your credit scores over time.

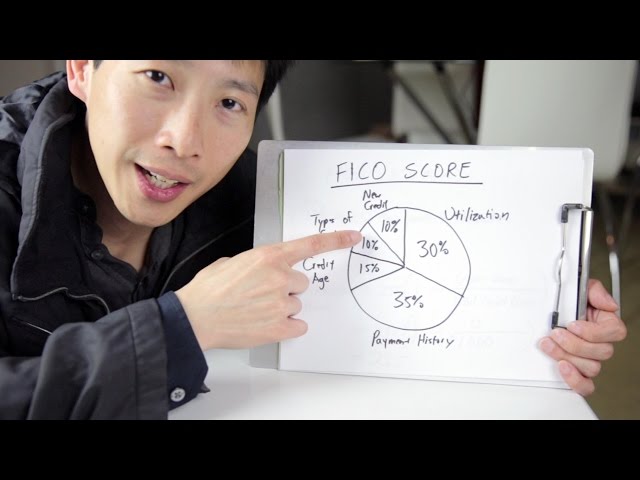

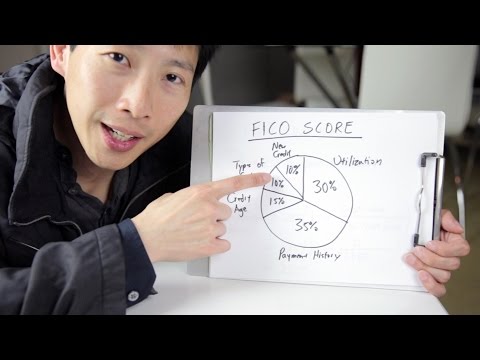

Here’s why this is important: Credit utilization is the second most important factor in credit scores, after payment history. It measures how much of your available credit you are using and is represented as a percentage. So if you have a $1,000 credit limit and a balance of $300, your utilization ratio would be 30%.

Utilization ratios above 30% can drag down your scores, even if you have otherwise impeccable credit habits. That’s because high balances relative to your limits can indicate to creditors that you’re stretched too thin or are mismanaging your finances –– even if that’s not the case.

Fortunately, it’s easy to keep tabs on your utilization ratio. Most major credit issuers now provide online access to account information, including current balances and credit limits. And some issuers even send monthly updates via email or text message. If you see that your ratio is edging toward 30%, simply pay down the balance to reduce it.

The 10% rule

It’s generally accepted that using more than 10% of your credit limit will hurt your credit score. Technically, using more than 30% of your limit can hurt your score, but most scoring models don’t start penalizing until you surpass 10%, so it makes sense to aim for that target.

If you have a good credit score, you may be able to get away with carrying a higher balance, but it’s still a good idea to keep your usage below 20%. That will help you avoid damaging your credit and giving lenders the impression that you’re struggling to manage your finances.

What if you can’t stick to the 30% or 10% rule?

Try the 20% rule

A lower credit utilization ratio is better for your credit score. But what if you can’t seem to keep your balances below 30% of your credit limits? You might try the 20% rule.

With the 20% rule, you would keep your balances at or below 20% of your credit limits. So, if you have a credit card with a limit of $1,000, you would try to keep your balance below $200.

The 20% rule is a good general guideline. But there are a couple of reasons why you might want to keep your balances even lower than 20%.

First, credit scoring models may give extra points to people who keep their balances well below their credit limits. So, if you can manage it, keeping your balances at 10% or even lower could give your scores an extra boost.

Second, it’s always a good idea to have some cushion in your credit limits in case of emergencies. If you have a balance at 20% and something comes up that requires you to use some of your credit limit, you could quickly find yourself in danger of going over the 30% mark—and that would be bad for your scores.

Try the 50% rule

The 50% rule is simple: Your credit utilization should never exceed 50%.

This means that if you have a credit limit of $3,000, you should never carry a balance of more than $1,500. And if you have a limit of $10,000, your maximum balance should be $5,000.

The 50% rule is a good guideline to follow, but it’s not set in stone. There may be times when your utilization is higher than 50%, such as when you’re making a large purchase and you know you’ll be able to pay it off quickly.

If your utilization is consistently above 50%, it’s a good idea to try to bring it down to avoid damaging your credit score. You can do this by paying down your balances, asking for a higher credit limit, or both.

How to use credit wisely

Use credit to your advantage

Credit can be a great tool to help you build your financial future — if used wisely. When used responsibly, credit can help you get a lower interest rate on a loan, rent an apartment, buy a car and much more. But when misused, credit can lead to expensive debt that can take years to pay off.

So how can you use credit wisely? One good rule of thumb is the 30% rule. This rule says that you should keep your balances at or below 30% of your credit limit. For example, if your credit limit is $1,000, you should keep your balance at or below $300.

Why is this important? Keeping your balances low will help you avoid costly interest charges and will also keep your credit score high. A high credit score will save you money in the long run by helping you get lower interest rates on loans and other forms of credit.

So if you’re looking to use credit wisely, remember the 30% rule — it can help you build a strong financial future.

Use credit to improve your credit score

Credit utilization is one of the most important factors in your credit score—it accounts for 30% of your FICO® Score. That’s why it’s important to keep your balances low and make payments on time.

What is credit utilization?

Credit utilization is the second largest factor in your credit score, and it refers to the amount of debt you have relative to your credit limits.

For example, suppose you have three credit cards:

-Credit Card A: $5,000 limit, $2,000 balance

-Credit Card B: $10,000 limit, $6,000 balance

-Credit Card C: $15,000 limit, $8,000 balance

Your total credit utilization would be 40% (($2,000 + $6,000 + $8,000) / ($5,000 + $10,000 + $15,000)).

Ideally, you should keep your credit utilization below 30%, but the lower the better.

How do I lower my credit utilization?

There are a few ways to lower your credit utilization ratio:

-Pay down your balances. If you have a high balance on one of your cards, try to pay it down as much as possible. Even a small decrease can have a big impact on your credit score.

-Request a higher credit limit. If you have a good payment history with a lender, you may be able to request a higher credit limit. This will immediately lower your credit utilization ratio. Just be sure not to use the extra room on your card—this can actually hurt your score in the long run.

-Keep unused accounts open. Closing an unused account will not improve your credit utilization ratio—and may actually hurt your score by lowering the average age of all your accounts.