What is the Highest Possible Credit Score?

Contents

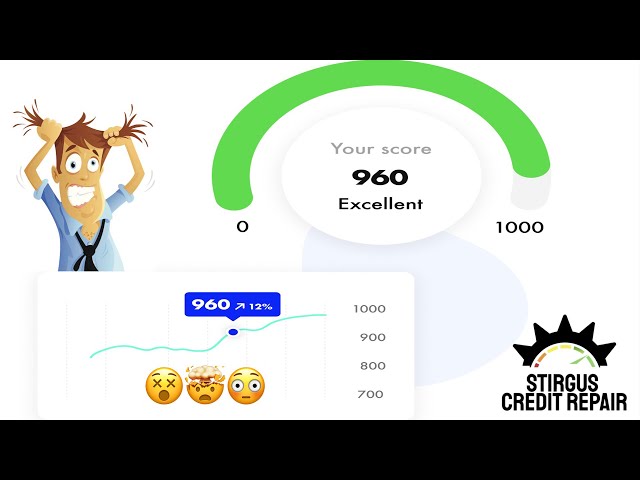

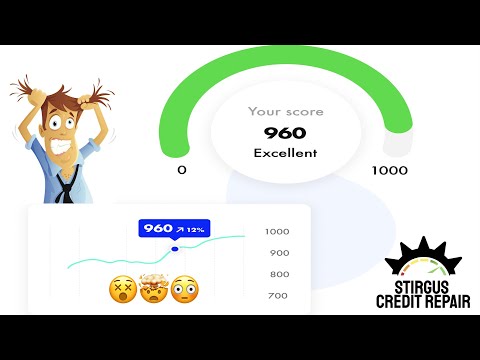

The highest possible credit score is 850. This is the highest score that you can achieve on the FICO scale. A score of 850 means that you have an excellent credit history and are a low-risk borrower.

Checkout this video:

Understanding Credit Scores

What is a credit score?

A credit score is a number that represents your creditworthiness – or how likely you are to repay debt. It’s used by lenders, landlords, and others to make decisions about whether or not to give you credit.

Your credit score is based on information from your credit report. This includes things like your payment history, the types of credit you have, and how much debt you have.

The highest possible credit score is 850. But if you have a score in the 800s, you’re doing well – most people have scores between 600 and 750.

You can get your credit score from a few different sources, including credit reporting agencies and some banks and credit card companies.

What is the highest possible credit score?

There are a few different credit scoring systems in use today, but the most common one is the FICO score. This score ranges from 300 to 850, with 850 being the highest possible score. A good credit score is generally considered to be anything above 700.

The Components of a Credit Score

A credit score is a three-digit number that lenders use to decide whether to give you a loan and what interest rate to charge. The highest possible credit score is 850. But if you have a score above 780, you’re doing very well. let’s break down the components of a credit score so you can understand what goes into your rating.

Payment history

One of the most important factors in your credit score is your payment history. Your payment history is a record of whether you have made your payments on time. It makes up 35% of your FICO score.

Your payment history includes:

-Your record of on-time payments

-Late payments

-Collection accounts

-Bankruptcies

-Foreclosures

If you have a history of late payments, it will hurt your credit score. To improve your payment history, make sure you pay all of your bills on time, every time. You should also try to avoid opening new lines of credit too frequently.

Credit utilization

Credit utilization is one of the most important factors in your credit score—it makes up 30% of your FICO® Score 9 calculation—so it’s important to keep it under control.

Your credit utilization rate is the percentage of your credit card’s credit limit that you use each month. For example, if you have a credit card with a $1,000 credit limit and you spend $500 in one month, your credit utilization rate would be 50%. The lower your rate, the better for your score.

Ideally, you should keep your credit utilization rate below 30%. That means if you have a $1,000 credit limit, you should only charge $300 to it each month. However, even if you go over that 30% mark, there’s no need to panic. Your score won’t be immediately impacted—and as long as you keep making payments on time and as agreed, your score will continue to improve over time.

To get a handle on your credit utilization rate, check out your credit report from Experian or another provider. You can see all of your open lines of credit and how much of their limits you’re using each month. If you find that you’re consistently above 30%, consider paying down your balances or asking for higher limits from your creditors.

Credit mix

One of the factors that makes up your credit score is your credit mix, which is the variety of credit products you have in your name. A well-rounded mix might include a mortgage, auto loan, student loan and a few revolving lines of credit, such as a credit card.

While the specific impact of your credit mix on your score can vary depending on the scoring model being used, generally having a good mix of different types of credit is viewed favorably by lenders. This is because it demonstrates that you can manage different types of debt responsibly.

Length of credit history

One of the five key components that make up your credit score is your length of credit history, which is also sometimes referred to as your “average age of accounts.” This factor reflects the length of time you’ve been using credit, and it’s one of the more important factors in your credit score because it helps creditors assess your level of experience.

Your length of credit history accounts for 15% of your FICO® Score 8, the most widely used type of credit score. So, if you have a long credit history, it will generally be a positive contributing factor to your credit score.

That said, a long credit history isn’t always necessary for having a good credit score. There are other factors that are also important, such as your payment history and credit utilization rate. And if you don’t have a long credit history because you’re new to using credit, there are still things you can do to build positive credit and improve your score over time.

How to Improve Your Credit Score

Your credit score is important. It affects your ability to get loans, rent an apartment, and even get a job. So what is the highest possible credit score? The answer may surprise you.

Make your payments on time

One of the most important things you can do to improve your credit score is to make all your payments on time, every time. Payment history is the biggest factor in most credit scoring models, accounting for 35% of your score. If you have a history of late or missed payments, it will be harder to get a loan or credit card with good terms, and you may end up paying more in interest and fees.

You can get help making sure your bills are paid on time by signing up for autopay or setting up reminders in your calendar. And if you do miss a payment, be sure to catch up as soon as possible — the sooner you pay, the less damaging it will be to your score.

Keep your credit utilization low

Your credit utilization is the percentage of your credit limit that you use, and it’s an important factor in your credit score.

Ideally, you should keep your credit utilization below 30%. That means if you have a $1,000 credit limit, you shouldn’t charge more than $300 to your card.

If you’re trying to improve your credit score, one of the best things you can do is lower your credit utilization. You can do this by paying down your debt or asking for a higher credit limit from your issuer.

Remember, your goal is to keep your credit utilization below 30%. If you can do that, you’ll be on your way to an excellent credit score.

Use a variety of credit products

One common misconception about credit scores is that you can improve your score by simply using a variety of credit products. While a mix of credit products (secured and unsecured, revolving and installment) can help show lenders that you’re a responsible borrower, having too many active accounts may actually hurt your score by making it appear that you’re overextended.

Establish a long credit history

One factor that has a significant impact on your credit score is the length of your credit history. Lenders like to see a long history because it gives them a better idea of how you manage credit.

If you have a short credit history, there are a few things you can do to try to improve your score. One is to get a credit-builder loan from a bank or credit union. This is a small loan that you repay over time, and it can help to improve your credit score by adding positive information to your credit report.

Another option is to become an authorized user on someone else’s credit card account. This means that you’ll have access to the account and can use it to make purchases, but the primary cardholder will be responsible for making the payments. If the account is managed responsibly, this can help you to build up a positive credit history.

Finally, try to avoid opening too many new accounts in a short period of time. Every time you open a new account, it has the potential to lower your credit score, at least temporarily. So if you’re trying to build up your history, it’s best to open new accounts only as needed.

The Bottom Line

A credit score is a number that reflects the risk a lender takes when you borrow money. The higher your score, the lower the risk to the lender, and the lower the interest rate you’ll likely pay. The credit scoring system in the United States is tiered, with scores ranging from 300 to 850.

The importance of a good credit score

Your credit score is one of the most important factors in your financial life. A good credit score can mean the difference between getting a loan and being denied, or getting a lower interest rate on a loan. A bad credit score can lead to higher interest rates and fees, and can even prevent you from getting a loan at all.

The bottom line is that a good credit score is important for your financial health. If you have a bad credit score, take steps to improve it. And if you have a good credit score, keep it in good shape by paying your bills on time and maintaining a good credit history.