What is the Highest Equifax Credit Score?

Contents

If you’re looking to understand what the highest Equifax credit score is, you’ve come to the right place. In this blog post, we’ll break down everything you need to know about credit scores, including what the highest Equifax score is and what it means for your creditworthiness.

Checkout this video:

Understanding Equifax Credit Scores

What is the Equifax Credit Score?

Your Equifax credit score is a number between 300 and 850 that represents your creditworthiness. The higher your score, the better your credit standing and the more likely you are to be approved for loans and credit card applications.

Equifax is one of the three major credit bureaus in the United States, along with TransUnion and Experian. Your Equifax credit score is based on information in your Equifax credit report, which includes information about your credit accounts, payment history, and any derogatory items such as late payments or collections.

lenders will use your Equifax credit score (as well as your scores from TransUnion and Experian) to help them decide whether to approve you for a loan or extend you a line of credit.

The highest possible Equifax credit score is 850, which is considered excellent. A score of 800 or above is considered very good, while a score of 750-799 is considered good. A score of 700-749 is considered fair, while a score of 650-699 is considered poor.

If you have a poor Equifax credit score, you may have difficulty qualifying for loans or lines of credit. You may also be offered less favorable terms, such as a higher interest rate, if you are approved for financing.

What is the highest Equifax Credit Score?

Most lenders use the FICO credit score system to determine creditworthiness, but there are other scoring systems out there. One of these is the Equifax Credit Score, which ranges from 280-850. This system is not as widely used as the FICO score, but it’s still worth understanding. So, what is the highest Equifax Credit Score?

The answer is 850. This is the top of the range and indicates an excellent level of creditworthiness. If you have a score in this range, you should have no problem getting approved for loans and credit cards with the best terms and rates.

Scores in the 780-850 range are considered excellent, while scores below 620 are considered poor. If your score falls in the middle of this range (620-780), you may still be able to get approved for loans and credit cards, but you may not qualify for the best terms and rates.

If you’re not sure where your Equifax Credit Score falls, you can check your credit report for free once a year at AnnualCreditReport.com. This will give you a good idea of where you stand and whether you need to take steps to improve your score.

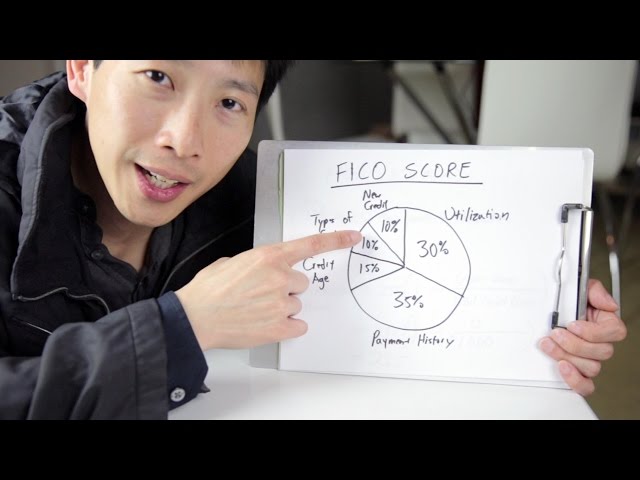

The Components of an Equifax Credit Score

Your Equifax credit score is made up of six components: payment history, credit utilization, credit mix, credit age, inquiries, and new credit. Payment history and credit utilization make up 65% of your score, so these are the most important factors.

Payment History

One of the most important aspects of your credit score is your payment history. This is a record of whether you have made your payments on time, and if not, how late they were. Payment history makes up 35% of your FICO® Score, so it’s vital to keep track of your payments and make sure you’re paying your bills on time.

One late payment can impact your credit score for up to seven years, so it’s important to be diligent about making all of your payments on time. You can set up automatic payments for some of your bills to help make sure you never miss a payment, and you can use a credit monitoring service to track your progress and see where you need to improve.

If you have a history of late payments, you may want to consider working with a credit counseling or debt management service to help you get back on track. These services can help you create a budget and develop a plan to get caught up on your payments. They can also negotiate with your creditors on your behalf to try to get late fees waived or reduced.

Credit Utilization

Credit Utilization is one of the components that make up your Equifax Credit Score. It accounts for 30% of your score and is defined as the amount of revolving credit you are using compared to the amount of credit you have available. It’s important to keep your credit utilization low in order to maintain a good Equifax Credit Score.

Equifax calculates your credit utilization by taking the total amount of revolving credit you have available and dividing it by the total amount of revolving credit you are using. For example, if you have a $1,000 credit limit on a credit card and you have a balance of $500, your credit utilization would be 50%. The general rule of thumb is to keep your credit utilization below 30%.

There are a few things you can do to lower your credit utilization and improve your Equifax Credit Score. One is to simply pay down your balances. Another is to ask for a higher credit limit from your creditors. And finally, you can try to spread out your balances across multiple cards instead of concentrating them on one card.

Length of Credit History

One of the most important factors in your Equifax credit score is the length of your credit history — specifically, how long you have been using credit. This factor makes up 15% of your score.

If you have a long history of responsible credit use, it will reflect positively on your score. On the other hand, if you have only recently started using credit, it will have a negative impact on your score. The length of your credit history is one factor that you cannot change, but it is important to be aware of its importance.

The good news is that the length of your credit history has a relatively small impact on your score compared to other factors. So even if you don’t have a long credit history, there are still things you can do to improve your score.

Types of Credit

There are four types of credit: installment, revolving, open and closed.

Installment credit is a loan that must be repaid in equal monthly payments over a set period of time, such as a mortgage or auto loan. The monthly payment includes both principal (the amount borrowed) and interest (the cost of borrowing the money).

Revolving credit is also called revolving debt. It’s a type of credit that doesn’t have a set repayment schedule, such as credit cards and lines of credit. You can choose to pay the minimum amount due each month or more, as long as you make your minimum payment on time. The interest rate on revolving debt is usually higher than on installment debt because it’s seen as a riskier type of borrowing.

Open credit is an account that does not have a set repayment schedule or term, such as some lines of credit. With open credit, you can borrow money up to your credit limit and repay it anytime without penalty.

Closed credit is an account with a set repayment schedule and term, such as installment loans and mortgages. Once you’ve repaid the loan in full, the account is closed.

How to Improve Your Equifax Credit Score

Your Equifax credit score is one of the most important factors that lenders look at when considering you for a loan. A high credit score means you’re a low-risk borrower, which could lead to a lower interest rate on your loan. Here are a few tips on how to improve your Equifax credit score.

Pay Your Bills on Time

One of the biggest factors in your Equifax credit score is your payment history—specifically, whether you pay your bills on time. So, if you want to improve your Equifax credit score, one of the best things you can do is make sure you’re never late with a payment.

There are a few different ways to make sure you always pay your bills on time. One is to set up automatic payments with your creditors—that way, you’ll never have to worry about forgetting to make a payment. Another is to set up reminders for yourself—you can do this by setting up a calendar reminder or using a phone app.

Remember, late payments can stay on your Equifax credit report for up to seven years, so it’s important to make sure you’re always paying on time. If you have any late payments in the past, try to get them removed by disputing them with Equifax.

Keep Your Credit Utilization Low

Your credit utilization makes up 30% of your credit score, so it’s important to keep it low. Utilization is the percentage of your credit limit that you’re using. For example, if you have a $1,000 credit limit and you’re carrying a balance of $500, your utilization would be 50%.

Ideally, you should keep your utilization below 30%, but the lower the better. If you have a high utilization, you can try to pay down your balances or ask for a higher credit limit to lower your ratio.

Paying down your balances isn’t always easy, but it’s worth it in the long run. Not only will it help improve your credit score, but it will also save you money in interest charges.

Use a Variety of Credit Types

You’ve probably heard that using a mix of credit types is one of the keys to a high credit score. That’s because it shows lenders that you can handle different types of debt responsibly.

The most common types of credit are:

-Mortgages

-Auto loans

-Credit cards

-Personal loans

But there are other types of credit, too, like:

-Home equity lines of credit (HELOCs)

-Student loans

-Secured loans (where you put down collateral, like a car or savings account)

Monitor Your Credit Report for Errors

You are entitled to a free credit report from each of the three credit bureaus every 12 months. Check your report for errors and dispute any that you find. An error on your credit report could lower your credit score, so it’s important to check and correct any mistakes. You can get your free annual credit reports from AnnualCreditReport.com.

Reviewing your credit report regularly is the best way to catch errors early. If you see an error on your Equifax credit report, you can dispute it online or by mail. Include as much supporting documentation as possible, such as a copy of your driver’s license or a bill with your current address. Equifax will investigate the error and remove it from your report if it finds that the information is incorrect.