What is the Grace Period on a Credit Card?

If you’re wondering what the grace period is on a credit card, you’re not alone. Many people are confused about this important detail. Read on to learn more about the grace period and how it can affect your credit card payments.

Checkout this video:

The Grace Period

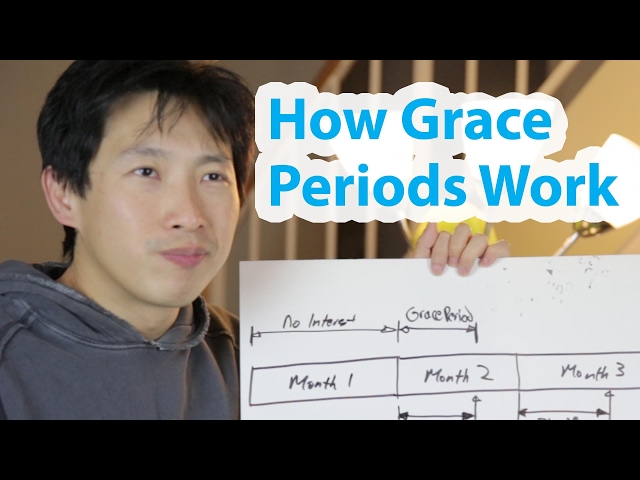

A grace period is the time between when your credit card bill is due and when the late payment penalty is applied. For example, if your credit card bill is due on the 1st of the month and you make a payment on the 5th, you would have a 5-day grace period. Most credit cards have a grace period of 21 days, which means you have 21 days to pay your bill without incurring a late fee. Many people don’t realize they have a grace period and end up paying late fees needlessly.

What is the Grace Period?

The grace period is the time between the end of your billing cycle and when your payment is due. During this time, you can avoid paying interest on your credit card balance by paying the full balance before the grace period ends. If you don’t pay off your balance, you’ll be charged interest on the outstanding balance from the date of purchase.

Most credit cards have a grace period of 21 days, but some cards have shorter or longer periods. For example, American Express cards typically don’t have a grace period, which means you’ll start accruing interest on purchases as soon as you make them. Discover and Chase generally offer 25-day grace periods on their credit cards.

To take advantage of the grace period, you’ll need to make sure that you pay off your balance in full by the due date. This can be tricky if you’re not diligent about tracking your spending, so it may be helpful to set up automatic payments from your checking account to ensure that your bill is paid on time.

How long is the Grace Period?

The grace period is the time from the end of your billing cycle to when your credit card company starts charging interest on your balances. Most credit cards have a grace period of 21 days, but some credit cards do not have a grace period. If you carry a balance on your credit card from one month to the next, you will be charged interest on that balance, even if your credit card has a grace period.

To avoid paying interest on your credit card balance, you will need to pay off your balance in full by the due date each month. If you are not able to pay off your balance in full, you should at least make a minimum payment by the due date to avoid being charged late fees.

What is the interest rate during the Grace Period?

The grace period is the time between when you are billed for your purchase and when the interest charge will be applied to your account. For example, if you are billed on the 1st of the month and have a grace period of 25 days, you will not be charged interest on any purchases made during that billing cycle until the 26th of the month. The grace period only applies if you pay your balance in full by the due date; if you carry a balance over from one month to the next, interest will be charged from the date of purchase.

The Benefits of the Grace Period

No interest accrues during the Grace Period

If you pay your balance in full each month, you can avoid paying interest on your credit card purchases by taking advantage of your card’s Grace Period. The Grace Period is the time between the end of a billing cycle and when interest begins to accrue on newly incurred balances.

So, if you have a credit card with a 20-day Grace Period and you make a purchase on the 10th day of your billing cycle, you will have 20 days to pay off that purchase before interest begins to accrue. If, however, you do not pay off your entire balance, any new purchases you make will begin to accrue interest immediately.

Grace Periods vary by credit card issuer, so be sure to check with your card issuer to find out how long you have to pay off your balance each month before interest begins to accrue.

More time to pay off your balance

The grace period is the time between when your credit card billing cycle ends and when your payment is due. Grace periods typically last 21 to 25 days, but they can vary depending on your card issuer. During this time, you won’t be charged interest on new purchases as long as you pay your balance in full by the due date. If you carry a balance from month to month, you’ll only be charged interest on that balance after the grace period ends.

Some issuers offer a grace period on cash advances and balance transfers, but others do not. It’s important to check with your card issuer to see what their policies are.

The grace period is a great way to avoid paying interest on your credit card purchases, as long as you can pay off your balance in full before the due date. If you need more time to pay off your balance, you can always make a minimum payment until you can pay it off in full. Just be aware that if you don’t pay off your balance within the grace period, you’ll start accruing interest on your new purchases from the date of purchase—so it’s important to plan accordingly.

Avoid late fees

The grace period is the time you have to pay your credit card bill in full before interest is applied to your balance. Most grace periods are 21 days long, but some can be as short as 20 days or as long as 25 days. The length of your grace period depends on your credit card issuer, and it’s important to know because it determines when you need to pay your bill to avoid paying interest.

If you carry a balance on your credit card from month to month, you won’t have a grace period. That’s because interest is charged on your average daily balance from the date your last statement was issued until the date your payment is received.

Paying your credit card bill in full every month is the best way to avoid paying interest, and it’s also a good way to improve your credit score. When you use a grace period, you’re showing creditors that you can borrow money and pay it back on time.

The Disadvantages of the Grace Period

Credit card companies market the grace period as a benefit to consumers, but there are some disadvantages to it that you should be aware of. First, if you carry a balance on your credit card from month to month, you will not be able to take advantage of the grace period. Second, the grace period only applies to new purchases, not cash advances or balance transfers. Finally, if you make a late payment, you may lose your grace period for that billing cycle.

You may still be charged a late fee

If you make a payment after the due date, you may still be charged a late fee. The grace period is the time between the end of your billing cycle and when your payment is due. If you pay your balance in full and on time during this grace period, you will not be charged interest on your purchases.

Depending on your credit card issuer, the grace period may be 21 days or more. If you do not pay your balance in full during the grace period, you will be charged interest on any new purchases and any previous balance that you carry over to the next month.

Some credit card issuers do not offer a grace period for cash advances and balance transfers. If this is the case, you will be charged interest on these transactions from the date of the transaction.

Your interest rate may increase

If you carry a balance on your credit card after the grace period expires, you will be charged interest. How much interest you’re charged depends on your credit card’s APR, or annual percentage rate. Your APR is the rate of interest you pay on your credit card balance annually.

Most credit cards have variable APRs, which means that your interest rate can change at any time. If the prime rate increases, your APR will likely increase as well. The prime rate is the interest rate that banks charge their most qualified customers.

If your APR increases, you’ll end up paying more in interest if you carry a balance on your credit card. In some cases, your minimum monthly payment may also increase if your APR increases.

You may lose your Grace Period if you make a late payment

If you make a late payment, your creditor may terminate your grace period. If this happens, you will be charged interest on your outstanding balance from the date of your last statement, not just from the date of your last purchase. In addition, many creditors will increase your interest rate if you make a late payment.