What Is Principal on a Loan?

Contents

You’ve probably heard the term “principal” used in reference to a loan, but what is principal on a loan? This article will explain what loan principal is, how it’s used, and how it affects your loan.

Checkout this video:

Introduction

The principal on a loan is the original sum of money that you borrowed from a lender. This amount does not include any interest or fees that may have been charged on the loan. You are responsible for repaying the principal, plus any interest, when the loan comes due.

What Is Principal?

When you take out a loan, the total amount you borrowed is not the only cost you incur. There is also interest, which is charged as a percentage of the principal. The principal is the amount of money you borrowed, and it doesn’t include any interest that has been added on top of it.

For example, let’s say you take out a loan for $100 at an interest rate of 10%. The total amount you will have to repay is $110, which includes the $100 you borrowed (the principal) plus $10 in interest.

The interest on a loan can be simple or compound. With simple interest, you only pay interest on the principal amount of the loan. With compound interest, you pay interest on the principal as well as any accumulated interest from previous periods. This can cause your debt to grow quickly if you don’t make regular payments, which is why it’s important to understand how your loan works before taking one out.

How Does Principal Affect My Loan?

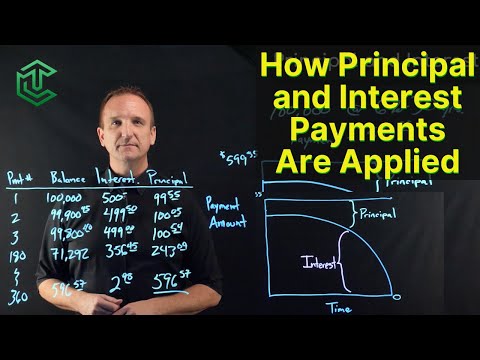

The amount of money you borrow from a lender is called the principal. The principal is the starting point for all loan repayments—you’ll pay interest on the money you borrow, and your loan payments will go toward both the principal and the interest.

As you make payments on your loan, a portion of each payment will go toward reducing the principal balance. The rest of each payment will go toward paying the interest that has accrued on the loan. In the early years of your loan, most of each payment will go toward paying interest, but as time goes on, an increasingly larger portion of each payment will go toward paying off the principal.

The amount of time it takes to pay off the principal balance of a loan depends on the term of the loan—the longer the term, the longer it will take to pay off the principal. For example, if you have a 30-year mortgage with a $200,000 principal balance, it will take 30 years to pay off the entire loan if you make regular payments at the same amount each month. On the other hand, if you have a 15-year mortgage with a $200,000 balance, it will take 15 years to pay off the entire loan.

The interest rate on your loan also affects how quickly you’ll be able to pay off the principal balance. A higher interest rate means that more of your monthly payment will go toward paying interest rather than reducing your principal balance. A lower interest rate means that more of your monthly payment will go toward reducing your principal balance.

Making extra payments on your loan can help you pay off the principal balance more quickly. When you make an extra payment, be sure to specify that you want that payment applied to your principle balance—otherwise, it may be applied to future payments or used to reduce your interest rate.

How Can I Pay Off My Principal Balance?

If you want to pay off your loan as quickly as possible, you need to focus on your principal balance. This is the amount of money you borrowed, minus any payments you’ve made toward the loan. Your interest payments go toward the interest charged on your loan, not the principal.

There are a few different ways to pay down your principal balance. One is to make extra payments on your loan. This can help you pay off your loan more quickly and save money on interest charges. You can also refinance your loan to get a lower interest rate and payment amount. This will help you reduce the amount of money you owe in interest charges and may help you pay off your loan more quickly.

If you’re having trouble making your monthly payments, there are some options that can help. You can talk to your lender about changing the terms of your loan, such as extending the repayment period or lowering the interest rate. You can also look into government programs that offer assistance for people who are struggling to make their loan payments.

Conclusion

Now that you know what principal is on a loan, you might be wondering how it’s different from interest. Principal is the amount of money you borrowed, while interest is the fee you’re charged for borrowing that money. Your mortgage payment is split between these two charges, with the majority usually going towards interest in the early years of your loan and more towards principal as time goes on.

Keep in mind that both of these charges are assessed by your lender based on the amount of your loan, the interest rate, and the term length. So, if you want to lower your monthly mortgage payment, you can try to get a lower interest rate or choose a shorter loan term. You can also try to make extra payments towards your principal balance to pay off your loan faster.