What is Principal in a Loan?

Contents

A loan’s principal is the initial amount of money borrowed, plus any additional money borrowed along the way. The interest is the cost of borrowing money, and is usually a percentage of the principal.

Checkout this video:

Introduction

The principal of a loan is the original sum of money that is borrowed before any interest or other fees are added. The principal is also the amount of money that remains to be paid on the loan, excluding any interest or other charges. When you make a payment on a loan, a portion of the payment goes towards paying off the principal, and the rest goes towards paying the interest.

What is a Principal?

A loan’s principal is the initial amount of money that is borrowed and needs to be repaid. This amount does not include interest or any other fees. For example, if you take out a loan for $1000, the principal would be $1000. You would then need to pay back the $1000 plus interest and fees.

The definition of a principal

When you take out a loan, the principal is the amount of money that you borrow. You also agree to pay interest on the principal. The interest is calculated as a percentage of the principal and is paid to the lender in addition to the principal. The amount of interest that you pay depends on the interest rate, which is set by the lender.

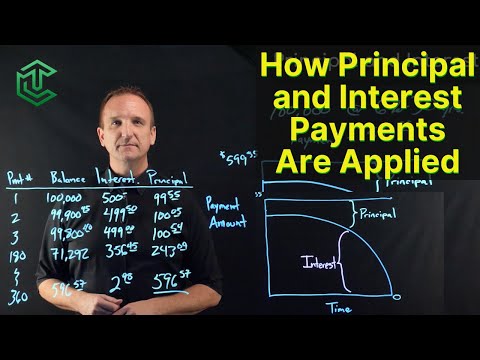

A loan’s term is the length of time that you have to repay the loan. The term can be as short as a few months or as long as 30 years. The interest rate and term determine your monthly payments. If you have a large principal and a long term, your monthly payments will be lower than if you have a small principal and a short term.

How a principal is used in a loan

In a loan, the principal is the amount of money that is borrowed and needs to be repaid. The interest is the fee charged for borrowing the money, and is typically a percentage of the principal. The term of the loan is the length of time over which the loan must be repaid. Each month, a portion of the payment goes towards repaying the principal, and a portion goes towards paying the interest. The proportion that goes towards each will depend on the terms of the loan.

How is a Principal Calculated?

A loan’s principal is the amount of money that is borrowed and needs to be repaid. It is important to know how your loan’s principal is calculated so that you can make informed decisions about your loan. In this article, we will explain how a loan’s principal is calculated.

The formula for calculating a principal

The formula used to calculate a loan’s principal is simple: P = L – M. Let’s break this down:

-P is the principal, or the amount of money you borrowed from the lender.

-L is the loan amount, or the total amount of money you borrowed including interest and fees.

-M is the amount of money you have already paid back to the lender.

So, if you have borrowed $100 from a lender, and you have already paid back $20, then your remaining principal balance is $80.

An example of how to calculate a principal

To calculate a monthly mortgage payment, start with the loan’s interest rate. For example, if you’re paying 5% interest, your annual interest rate would be 0.05. Then, multiply your principal loan amount by that decimal. So, if you’re borrowing $100,000, you’d multiply $100,000 by .05 to get $5,000. Then divide that number by 12 to get your monthly interest cost: $5,000/12 = $416.67. Finally, add that number to your monthly principal payments to calculate your full monthly mortgage payment: $416.67 + 1,000 = $1,416.67/month.

What are the Benefits of a Principal?

A principal in a loan is the initial sum of money that is borrowed and needs to be paid back. This sum does not include any interest that may have been accrued. A principal can also be referred to as the face value of a bond. There are many benefits to having a principal, which we will explore in this article.

The benefits of a principal for lenders

A principal is the face value of a bond, loan, or other security. For lenders, the principal is the amount of money that must be repaid, plus any interest. The benefits of a principal for lenders are clarity and security. A loan with a clear principal allows lenders to easily calculate their return on investment (ROI), and also makes it easier to track payments and monitor late payments. A lender is also able to rely on the fact that the borrower will not be able to get out of the loan by refinancing at a lower interest rate or taking out a new loan.

The benefits of a principal for borrowers

A principal is the amount of money borrowed or the starting balance of an investment. The borrower or investor pays interest on the principal. For example, if you take out a $100,000 mortgage with a 4% interest rate, your monthly payment will be $4,000, and $400 of that will go toward interest while $3,600 will go toward the principal.

Paying down the principal is important because it reduces the amount of interest you pay over time. With each mortgage payment, more money goes toward the principal, and less goes toward interest. In the early years of your loan, most of your payment goes toward paying off interest because there’s a larger balance. But as you pay down the principal, your payments will increasingly go toward paying off the loan itself.

Keep in mind that some loans, such as adjustable-rate mortgages (ARMs), may have low introductory interest rates that increase over time. That means you could end up paying more interest in the long run even if you make extra payments to reduce the principal.

What are the Drawbacks of a Principal?

When you take out a loan, the amount of money you borrowed is known as the principal. You are required to pay the lender back the principal, plus any interest that has accrued, over the course of the loan term. However, there are a few drawbacks to taking out a loan with a principal.

The drawbacks of a principal for lenders

There are a few potential drawbacks for lenders when it comes to a principal. First, if the borrower defaults on the loan, the lender will only be able to collect the principal amount from the sale of the property. This means that the lender could end up losing money on the loan if the property is sold for less than the outstanding balance. Additionally, if the borrower makes late payments or misses payments altogether, the lender may not receive all of the money that is owed.

The drawbacks of a principal for borrowers

The drawbacks of a principal for borrowers are that they may have to pay a higher interest rate and may not be able to borrow as much money as they would with a lower principal. Additionally, if the borrower defaults on the loan, the lender may foreclose on the property and the borrower could lose their home.

Conclusion

To sum it up, the principal in a loan is the initial amount of money that is borrowed, and it is typically repaid over the life of the loan with interest. The principal does not include any fees or charges associated with the loan.