What is a Non Conforming Loan?

Contents

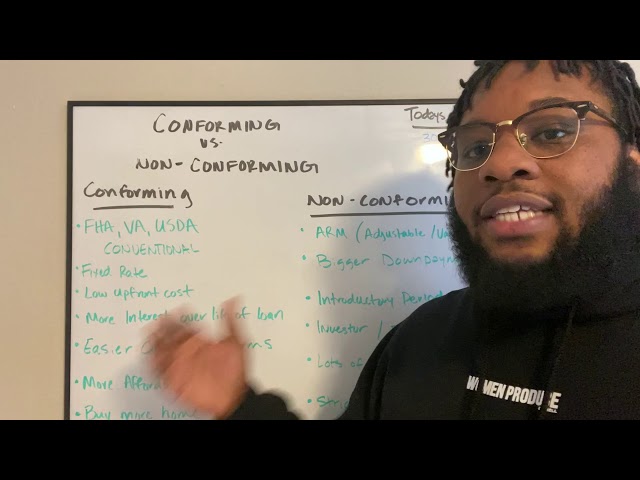

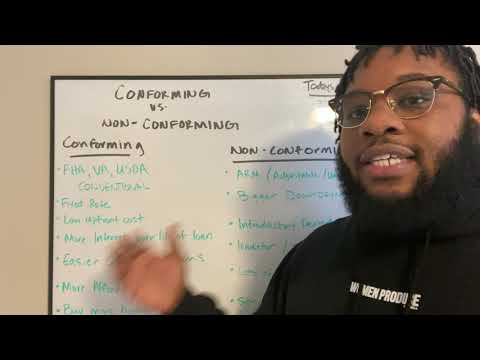

Non-conforming loans are loans that do not meet the guidelines of Fannie Mae or Freddie Mac. These loans typically have a higher interest rate and may require a larger down payment.

Checkout this video:

What is a Non Conforming Loan?

A non-conforming loan is a loan that doesn’t meet the guidelines that are set by Freddie Mac and Fannie Mae. These two companies purchase mortgages from lenders, so they have a good idea of what guidelines they will accept. For a variety of reasons, Freddie and Fannie may decide not to purchase certain loans; these are the non-conforming loans. The most common reason for a non-conforming loan is that the borrower poses a greater risk than lenders are willing to take. In order for Freddie and Fannie to purchase a mortgage, they need to be fairly certain that the borrower will be able to make the payments; with a greater risk comes a greater chance of default, so these loans are usually not purchased.

Who is a Non Conforming Borrower?

In general, any loan that does not meet guidelines is a non-conforming loan. A loan that does not meet guidelines specifically because it is too large is known as a jumbo loan.

Jumbo loans are non-conforming because they exceed the maximum loan amount allowed by Fannie Mae and Freddie Mac, the government-sponsored companies that buy most U.S. residential mortgages from lenders. When you borrow more than the limit set by FNMA/FHLMC, your loan is considered a jumbo mortgage and cannot be sold to these government-sponsored enterprises.

What are the benefits of a Non Conforming Loan?

A Non-Conforming Loan is a mortgage loan that exceeds the loan limits set by the Federal National Mortgage Association (FNMA) or the Federal Home Loan Mortgage Corporation (FHLMC). Non-Conforming Loans are also commonly referred to as Jumbo Loans.

The benefits of a Non-Conforming Loan are that it can be used to purchase a primary residence, second home, or investment property. Non-Conforming Loans can also be used to refinance an existing mortgage.

Non-Conforming Loans typically have slightly higher interest rates than Conforming Loans because they carry a higher level of risk for the lender.

If you are looking for a Non-Conforming Loan, contact your local mortgage lender or broker to discuss your options.

What are the drawbacks of a Non Conforming Loan?

Non Conforming Loans usually have a higher interest rate than Conforming Loans because they are seen as higher risk by lenders. They can be difficult to find because not all lenders offer them and they often come with strict eligibility requirements. Borrowers with less-than-perfect credit scores or who are self-employed may have difficulty qualifying for a Non Conforming Loan.

How do I qualify for a Non Conforming Loan?

A Non Conforming Loan is a mortgage loan that does not conform to the guidelines set by the Federal National Mortgage Association (Fannie Mae) or the Federal Home Loan Mortgage Corporation (Freddie Mac). These two government-sponsored enterprises purchase loans from lenders, then securitize them and sell them to investors through Wall Street. In order for a loan to be sold through these channels, it must meet certain standards, including size of the loan, credit score of the borrower, and documentation requirements.

Non Conforming Loans are also commonly referred to as Jumbo Loans. A jumbo loan is any mortage loan that exceeds the Conventional loan limit of $484,350 for a single-family home. In most U.S counties, the Conventional loan limit is $484,350, but in high-cost areas like San Francisco and New York City, the limit can be as high as $726,525.

To qualify for a Non Conforming Loan, you will need a higher credit score and a larger down payment than what is required for a Conventional Loan. You will also need to provide additional documentation to prove your income and assets.

How do I apply for a Non Conforming Loan?

The first step is to talk to a mortgage loan officer about your financial situation and what you are looking to do. They will help you determine if a non-conforming loan is the best fit for your needs. If it is, they will work with you to gather the necessary documentation and begin the application process.