What is a Finance Charge on a Credit Card?

Contents

If you’ve ever been confused by a finance charge on your credit card statement, you’re not alone. In this post, we’ll break down what a finance charge is and how it’s calculated.

Credit Card?’ style=”display:none”>Checkout this video:

What is a Finance Charge?

A finance charge is a charge assessed by a credit card issuer when a consumer fails to pay their credit card bill in full by the due date. This charge is typically a percentage of the outstanding balance, and is meant to compensate the credit card issuer for the time value of money. In most cases, finance charges are avoidable if the consumer pays their credit card bill in full and on time each month. However, some credit card issuers may assess a finance charge even if the consumer pays their bill on time, if the outstanding balance is above a certain threshold.

How is the Finance Charge Calculated?

The finance charge is the cost of borrowing money, and it’s calculated using your APR and your average daily balance. To get your average daily balance, your issuer takes the beginning balance of each day in your billing cycle and adds any new charges or payments. Then, they subtract any credits, like returns or adjustments. This number is then divided by the number of days in your billing cycle to get the average daily balance.

Here’s the formula:

Average Daily Balance x APR x Number of Days in Billing Cycle ÷ 365 = Finance Charge

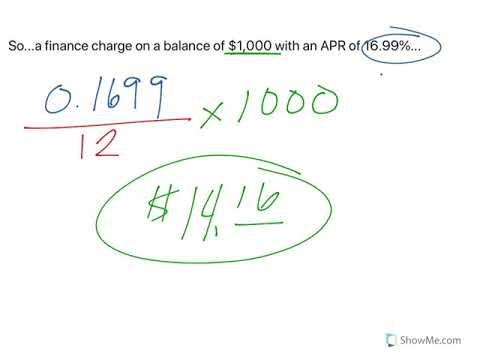

For example, let’s say you have a card with a 17% APR and you have a $100 balance at the beginning of a 30-day billing cycle. You don’t use the card during the month, but you do have a $5 monthly service fee. At the end of the billing cycle, your balance would be $105 ($100 + $5 service fee). Your Average Daily Balance would be $105 divided by 30 days, or $3.50. And your finance charge for that month would be:

$3.50 x .17 x 30 ÷ 365 = $0.16

What are the Types of Finance Charges?

A finance charge is a fee charged by a lender for the use of credit. The finance charge may be a flat fee, such as an annual fee, or it may be a variable fee that is based on the amount of credit used, the interest rate, or the length of time the credit is used. There are three main types of finance charges: interest charges, annual fees, and late fees.

Interest Charges

Finance charges on credit cards can take many forms, but the most common is interest. When you carry a balance from one month to the next, you accrue interest charges based on the amount of your balance and the annual percentage rate (APR) charged by your card issuer. Your monthly statement will list the interest charges incurred during the billing period.

Other types of finance charges may include annual fees, late payment fees, returned payment fees, cash advance fees and balance transfer fees. Some cards also charge foreign transaction fees for purchases made outside of the United States.

Minimum Finance Charges

Minimum finance charges are the smallest amount that your credit card issuer can charge you for carrying a balance on your card. This type of finance charge is usually around $1.50. If you have a balance of $10 on your credit card, and your credit card’s APR is 15%, your minimum finance charge for that month would be $1.50.

Transaction Fees

Transaction fees are finance charges that are assessed each time you use your credit card for a purchase. The fee is typically a percentage of the total transaction amount, and it is added to your balance at the end of the billing cycle. For example, if you have a 1% transaction fee and you make a $100 purchase with your credit card, the finance charge would be $1.

Transaction fees are just one type of finance charge that can be assessed on your credit card account. Other types of finance charges include interest charges, annual fees, and late payment fees.

How to Avoid Finance Charges

A finance charge is a fee that is charged by a lender for the use of credit. This charge is calculated based on the interest rate and the amount of time that the credit is used. The finance charge is usually a percentage of the total balance of the credit account. There are a few ways to avoid paying a finance charge on your credit card.

Pay Your Balance in Full Each Month

One way to avoid finance charges is to always pay your balance in full each month. That way, you don’t carry a balance from one month to the next, and you won’t be charged interest.

Of course, that’s not always possible. But even if you can’t pay your balance in full, try to pay as much as you can. The more you can pay, the less interest you’ll be charged.

Another way to avoid finance charges is to use a credit card with a 0% introductory APR on purchases. With this type of card, you won’t be charged interest on purchases for a certain period of time (usually 12 to 18 months).

Know Your Grace Period

To avoid finance charges, you must know your credit card’s grace period. The grace period is the time you have to pay your credit card balance in full without incurring any finance charges. Grace periods typically last 20 to 25 days, but some issuers don’t offer them at all. If your issuer doesn’t offer a grace period, you’ll start accruing interest on your balance as soon as each purchase posts to your account.

If you carry a balance from one month to the next, you’ll incur a finance charge. How much you’re charged depends on the interest rate and balance of your credit card account, as well as the method your issuer uses to calculate finance charges. Read on to learn more about how issuers calculate finance charges and ways you can avoid them.

There are two common methods issuers use to calculate finance charges: average daily balance (including new purchases) and daily periodic rate times average daily balance. To avoid finance charges under either method, simply pay your entire balance prior to the due date each month.

Avoid Cash Advances and Balance Transfers

Cash advances and balance transfers often have different terms than your normal credit card purchases. For example, they may have a higher interest rate or may not have a grace period (which means you’ll start accruing interest immediately).

To avoid finance charges on cash advances and balance transfers, either don’t use your credit card for these transactions or be sure to pay off the balance in full each month.

How to Dispute a Finance Charge

A finance charge is a fee that is charged by a credit card company for the use of their credit card. This fee can be charged for a variety of reasons, such as for the purchase of a product or service, for a cash advance, or for a balance transfer. If you believe that you have been charged a finance charge in error, you can dispute the charge with your credit card company.

Write a Letter to the Credit Card Company

If you believe a finance charge on your credit card is incorrect, you can dispute the charge by writing a letter to the credit card company. Be sure to include your account number, the date of the charge and an explanation of why you believe the charge is incorrect. You may also want to include copies of any supporting documentation.

It’s important to keep in mind that you will still be responsible for paying any undisputed charges on your account. If you have already paid the disputed amount, you can request a refund in your letter.

Once the credit card company receives your letter, they will investigate the charge and get back to you with their findings. If they determine that the finance charge is incorrect, they will adjust your account accordingly.

Include Documentation

If you’re disputing a finance charge, you need to include documentation that supports your position. For example, if you’re disputing a late fee, you need to include a copy of your payment history or a statement that shows the date your payment was received.

To dispute a finance charge, you need to:

-Include documentation that supports your position

-Send your dispute letter to the credit card company

-Include your name, address, and account number

-Explain why you’re disputing the charge

-Request a refund

You should send your dispute letter by certified mail so that you have proof of when it was sent and received. The credit card company has 30 days to respond to your dispute.

Send the Letter via Certified Mail

Sending the letter via certified mail provides you with proof that the credit card company received your dispute. Include the following information in your letter:

-Your name, address, and account number

-The date of the charge in question

-A description of the charge and why you believe it’s incorrect

-The amount of the charge

-The date you noticed the charge

If you have documentation to support your dispute, enclose copies (not originals) with your letter and keep a copy for your files. Send your letter to the address provided for “billing inquiries” on your statement. If you don’t have this information, call customer service to get the correct address.

When You Can’t Avoid a Finance Charge

A finance charge is a fee that’s charged on a credit card account when you carry a balance from one month to the next. A finance charge is based on your APR (annual percentage rate) and the number of days you carry a balance. The APR is the interest rate you pay on your credit card balance.

Create a Payment Plan

If you have a balance on your credit card and can’t pay it off in full, you may be able to set up a payment plan with your credit card issuer. This can help you avoid finance charges and keep your account in good standing.

Here’s how it works: You and your credit card issuer agree on a set monthly payment that will paid automatically from your bank account. In most cases, you’ll also be required to pay a one-time setup fee. Once the payments are set up, you’ll continue to accrue interest on your balance at the card’s regular APR, but you won’t be charged any additional fees as long as you make your payments on time.

If you’re not sure whether your card issuer offers this option, give them a call and ask. It’s important to note that not all issuers allow payment plans, and those that do usually have strict requirements that must be met. For example, some issuers may only allow payment plans for balances below a certain amount, or they may require you to make a minimum number of payments before they’ll allow you to set up a plan.

If you decide to create a payment plan, be sure to ask about all the details before agreeing to anything. That way, there won’t be any surprises down the road.

Negotiate with the Credit Card Company

If you find yourself in a situation where you can’t avoid a finance charge, your best bet is to try to negotiate with the credit card company. You may be able to get them to waive the fee or lower the interest rate. It’s always worth a try!

Refinance Your Debt

If you have high-interest debt, one way to reduce the amount of interest you pay is to refinance your debt. This means taking out a new loan with a lower interest rate and using it to pay off your existing debt. Although this will require you to take on more debt, it can save you money in the long run by reducing the amount of interest you pay. You can refinance your debt through a personal loan, a balance transfer credit card, or a home equity loan.