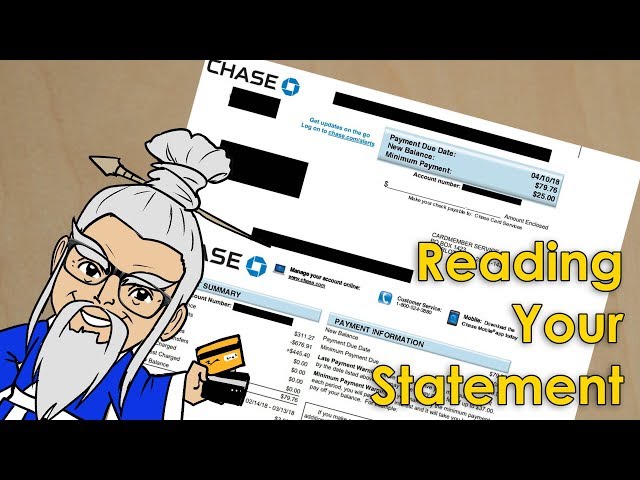

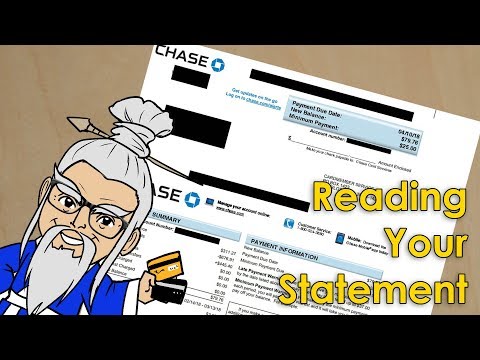

What is a Credit Card Statement?

Contents

- What is a Credit Card Statement?

- How to Read a Credit Card Statement?

- What is a Credit Card Statement Balance?

- What is a Credit Card Statement Minimum Payment?

- How to Pay Your Credit Card Statement?

- When is Your Credit Card Statement Due?

- What Happens if You Don’t Pay Your Credit Card Statement?

- How to Dispute a Charge on Your Credit Card Statement?

- How to Avoid Paying Interest on Your Credit Card Statement?

- How to Reduce the Amount You Owe on Your Credit Card Statement?

A credit card statement is a monthly report that shows all the activity on your credit card account for the previous month.

Credit Card Statement?’ style=”display:none”>Checkout this video:

What is a Credit Card Statement?

A credit card statement is a monthly report that shows all the activity on your credit card account for a billing period. This includes all the transactions you made, any fees you were charged, and your current balance. Credit card statements are important because they give you a detailed record of your spending and can help you spot any fraudulent activity. They also provide an opportunity to check for errors and correct them before they become a problem.

How to Read a Credit Card Statement?

Financial literacy is important. Learning how to read a credit card statement is a valuable skill that can help you keep track of your spending and avoid costly mistakes.

Most credit card statements will have the following information:

-Your name and address

-The date the statement was generated

-The name of the credit card issuer

-Your account number

-The opening and closing balance for the billing period

-A list of all transactions made during the billing period, including the date, type, amount, and balance after each transaction

-Minimum payment information

-Interest and fees charged for the billing period

Statement due dates are typically 21 days after the close of a billing period, so you will have time to review your statement and make any necessary payments. Most credit card issuers will also give you the option to receive electronic statements, which can be helpful if you want to track your spending more closely.

What is a Credit Card Statement Balance?

Your credit card statement is a record of your credit card activity during your billing period, typically two to three weeks. It includes all the transactions you made, including any interest and fees charged. Your statement balance is the total amount you owe on your credit card as of the statement date.

To avoid paying interest, you need to pay your statement balance in full by the payment due date. If you don’t, you’ll be charged interest on the outstanding balance, which will be added to your balance going forward. You can find your statement balance and other account information on your credit card statements.

What is a Credit Card Statement Minimum Payment?

Your minimum payment is the least amount of money that you can pay on your credit card bill each month without being penalized. Your minimum payment is usually a percentage of your balance, plus any interest and fees that have accrued.

If you only make your minimum payment each month, it will take you much longer to pay off your debt and you will end up paying more in interest. Therefore, it’s always best to pay more than the minimum if you can.

Some credit card companies may also raise your interest rate if you only make the minimum payment. This is because they see you as a higher-risk customer who is more likely to default on their debt.

If you’re having trouble making your minimum payments, contact your credit card company as soon as possible. They may be able to work with you to set up a repayment plan or lower your interest rate.

How to Pay Your Credit Card Statement?

Each month, you will receive a credit card statement in the mail (or via email, depending on your preference). This statement will list all of the activity on your account for the previous billing cycle, including purchases, payments, credits, interest and fees. It’s important to review your statement carefully each month to ensure that all of the charges are accurate and to catch any fraudulent activity.

To pay your credit card statement, you will need to log in to your online account or call customer service to make a payment. You will need to provide your account number and routing number (from your checkbook), as well as the amount you wish to pay. Most companies offer the option to set up automatic payments from your checking account, which can help you stay current on your balance and avoid late fees.

When is Your Credit Card Statement Due?

Your credit card statement is released at the end of your billing cycle. The exact date will vary depending on your credit card issuer, but it’s typically 21 to 25 days after the end of the month.

For example, if your billing cycle ends on March 31, your statement should be released around April 21. Keep in mind that weekends and holidays can push back the release date, so don’t be alarmed if it arrives a few days later than expected.

Your due date is also included in your credit card statement. This is the date by which you must pay your bill in full to avoid incurring interest charges. The grace period is usually 21 to 25 days, but it can be as short as 20 days or as long as 30 days.

To avoid paying interest, you’ll need to pay your bill in full by the due date each month. If you can’t do that, make sure to at least pay the minimum amount due to keep your account in good standing and avoid late fees.

What Happens if You Don’t Pay Your Credit Card Statement?

Your credit card statement is a monthly record of your credit card activity, including any new purchases, payments, changes in your balance, and any fees charged. It’s important to review your statement carefully each month to make sure there are no errors, and to keep track of your spending.

If you don’t pay your credit card statement in full each month, you will be charged interest on the outstanding balance. The interest rate will be listed on your statement, and can vary depending on the type of card and the issuer. You may also be charged late fees if you miss a payment deadline.

Paying only the minimum amount due on your credit card statement will result in high interest charges and can take years to pay off your debt. It’s important to make more than the minimum payment if you can, and to try to pay off your balance in full each month.

How to Dispute a Charge on Your Credit Card Statement?

When you see a charge on your credit card statement that you don’t recognize, it can be confusing and frustrating. You may not know what the charge is for, or you may think it’s a mistake. Either way, you can dispute the charge with your credit card issuer.

Most credit card issuers have a process for disputes, and they will usually investigate the charge for you. If they find that the charge was made by a merchant that you did business with, they will not remove the charge from your statement. But if they determine that the charge was made in error, they will remove it and may refund the amount of the charge to your account.

You can usually dispute a charge by calling your credit card issuer or filing a dispute form online. You will need to provide some information about the charge, such as the date and amount of the charge, and the name of the merchant. Once you file a dispute, the credit card issuer will investigate and get back to you with their findings.

How to Avoid Paying Interest on Your Credit Card Statement?

Your credit card statement is a summary of your credit card activity for a billing period. It includes your balance, payments, credits, interest charges, and any fees you may have incurred during the period.

To avoid paying interest on your credit card statement, you must pay your balance in full by the due date. If you do not pay your balance in full, you will be charged interest on the outstanding balance.

You can avoid paying interest on your credit card statement by making habitual use of a few key repayment strategies:

– Paying more than the minimum amount due each month

– Paying off your balance in full each month

– Avoiding cash advances and other transactions that incur additional fees

– Making payments on time and in full

If you follow these repayment strategies, you will not only avoid paying interest on your credit card statement, but you will also improve your credit score.

How to Reduce the Amount You Owe on Your Credit Card Statement?

There are a few things you can do to help reduce the amount you owe on your credit card statement.

-First, try to make more than the minimum payment each month. This will help to reduce your overall balance and the amount of interest you accrue.

-Secondly, try to pay down any high-interest balances first. By doing this, you’ll save money in the long run by paying less in interest charges.

-Lastly, if you have multiple cards with balances, try to focus on paying down one card at a time. Once you’ve paid off one card, you can then focus on paying down the next one. This method can help to keep you motivated as you see your debt balances shrinking.