What is an Unsubsidized Student Loan?

Contents

- What is an Unsubsidized Student Loan?

- How do Unsubsidized Loans Work?

- Who is Eligible for an Unsubsidized Loan?

- What are the Interest Rates for Unsubsidized Loans?

- How to Apply for an Unsubsidized Loan

- What are the Repayment Terms for Unsubsidized Loans?

- What are the Pros and Cons of Unsubsidized Loans?

- Alternatives to Unsubsidized Loans

An Unsubsidized Student Loan is a type of financial aid that you have to pay back with interest. It’s not based on your financial need.

Checkout this video:

What is an Unsubsidized Student Loan?

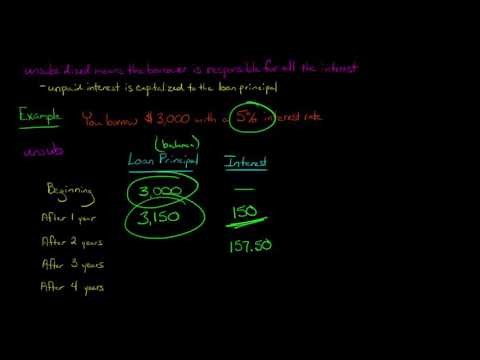

An unsubsidized student loan is a type of financial aid that you have to repay with interest. You are responsible for all the interest that accrues on your unsubsidized student loan from the time it is first disbursed until it is paid in full.

How do Unsubsidized Loans Work?

An unsubsidized loan is a student loan that is not awarded on the basis of financial need. Students are responsible for the interest on unsubsidized loans from the time the loans are disbursed until they are paid in full. The U.S. Department of Education offers two unsubsidized loan programs: the William D. Ford Federal Direct Loan Program and the Federal Perkins Loan Program.

The William D. Ford Federal Direct Loan Program offers four types of unsubsidized loans: Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

Direct Subsidized Loans are awarded to undergraduate students with financial need. The U.S. Department of Education pays the interest on these loans while the borrower is in school at least half-time, during a grace period, and during deferment periods.

Direct Unsubsidized Loans are not awarded on the basis of financial need. Interest accrues on these loans from the time they are disbursed until they are paid in full. Borrowers can choose to pay the interest while they are in school or allow it to accrue and be added to the principal amount of their loan (capitalization).

Direct PLUS Loans are unsubsidized loans for graduate students and parents of dependent undergraduate students. Parents can borrow up to the cost of attendance minus any other financial aid their child receives. Graduate students can borrow up to the cost of attendance minus any other financial aid they receive. Interest accrues on these loans from the time they are disbursed until they are paid in full. Borrowers can choose to pay the interest while they are in school or allow it to accrue and be added to the principal amount of their loan (capitalization).

Direct Consolidation Loans allow borrowers to combine all of their eligible federal student loans into a single loan with a single repayment period and repayment options. Private education loans cannot be consolidated into a Direct Consolidation Loan but may be reconsolidated into a Direct Consolidation Loan if certain conditions are met..

Who is Eligible for an Unsubsidized Loan?

To be eligible for an unsubsidized student loan, you must:

-Be enrolled in an eligible degree or certificate program

-Be a U.S. citizen or eligible non-citizen

-Have a valid Social Security number

-Not be in default on any federal student loans or owe money on a federal grant

-Maintain satisfactory academic progress in college or career school

-CompleteEntrance Counseling at studentaid.gov/entrance-counseling

-Sign a Master Promissory Note at studentaid.gov/mpn

What are the Interest Rates for Unsubsidized Loans?

The current interest rate for unsubsidized undergraduate Stafford Loans is 5.05%. graduate Stafford Loans have a slightly higher interest rate of 6.6%. These rates are effective as of July 1, 2017 and are fixed for the life of the loan.

How to Apply for an Unsubsidized Loan

To apply for an unsubsidized loan, fill out the Free Application for Federal Student Aid (FAFSA®) form. You will need to provide information about your financial situation, including your income, assets and family size. The form is available for free on the FAFSA website.

If you’re a dependent student, your parents will also need to fill out the form. If you’re an independent student, you won’t need to provide your parents’ information.

Once you’ve submitted the FAFSA form, you’ll receive a Student Aid Report (SAR). This document will tell you how much money you’re eligible to receive from the government. It will also list your Expected Family Contribution (EFC). This is the amount of money that your family is expected to contribute towards your education.

If you’re applying for an unsubsidized loan, you can borrow up to the full cost of attendance minus any other financial aid that you’re receiving. For example, if the cost of attendance at your school is $10,000 and you’re receiving a $5,000 scholarship, you can borrow up to $5,000 in unsubsidized loans.

What are the Repayment Terms for Unsubsidized Loans?

Assuming you don’t have a grace period, you’ll have to start repaying your unsubsidized student loan immediately after you graduate, withdraw from school, or drop below half-time enrollment.

The repayment term for an unsubsidized loan is usually 10 years, but it can be up to 25 years if you consolidate your loans or have a lot of debt. The repayment term for a Parent PLUS Loan is also 10 years.

You can choose from several repayment plans for both subsidized and unsubsidized loans, including the Standard Plan, Graduated Plan, Extended Plan, and Income-Based Repayment (IBR) Plan.

The Standard Plan offers fixed monthly payments for up to 10 years. The Graduated Plan starts with smaller payments that increase every two years for up to 10 years. The Extended Plan offers fixed or graduated payments for up to 25 years. The IBR Plan bases your monthly payment on your income and family size and is available for both subsidized and unsubsidized loans.

If you have trouble making your monthly loan payments, you can defer or forbear your loans. With deferment, you can temporarily postpone making your loan payments. With forbearance, you can temporarily reduce or stop making your loan payments.

What are the Pros and Cons of Unsubsidized Loans?

There are a few key differences between subsidized and unsubsidized loans that you should be aware of before taking out a loan.

An unsubsidized loan is a type of student loan that is not based on financial need. This means that you will be responsible for paying the interest on the loan from the time the funds are disbursed until the time the loan is paid in full. With a subsidized loan, the government pays the interest while you are in school and during any deferment periods.

The main advantage of an unsubsidized loan is that you are not required to prove financial need in order to qualify. This makes them a good option for students who may not qualify for other types of financial aid. Another advantage is that you can start accruing interest from the time the funds are disbursed, which can save you money in the long run.

The main disadvantage of an unsubsidized loan is that you will be responsible for paying the interest from the time the funds are disbursed. This can add up over time and increase the amount you have to repay. Additionally, unsubsidized loans typically have higher interest rates than subsidized loans.

Alternatives to Unsubsidized Loans

There are a few alternatives to unsubsidized loans that you may want to consider:

Federal Perkins Loans: These are low-interest loans for undergraduate and graduate students with exceptional financial need.

Direct PLUS Loans: These are loans for parents and graduate or professional students. They have a higher interest rate than other federal student loans, but they offer flexible repayment options.

Private loans: These are non-federal loans, which means they’re not guaranteed by the government. They typically have variable interest rates and may not offer the same repayment options as federal loans.