What Is a High Priced Mortgage Loan?

Contents

A high priced mortgage loan is a mortgage loan that has an annual percentage rate (APR) higher than the Average Prime Offer Rate (APOR).

Checkout this video:

Introduction

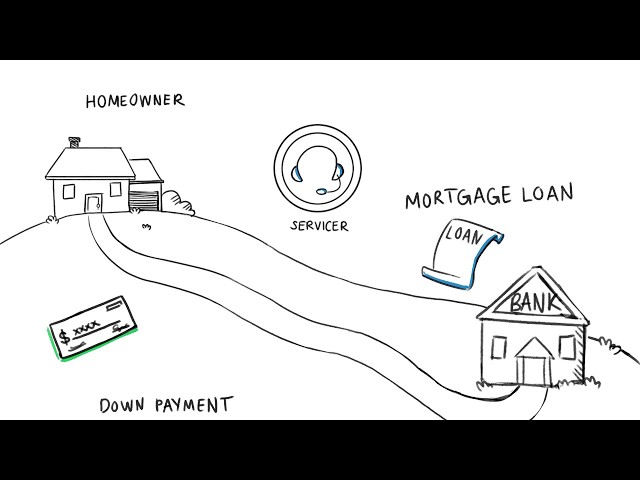

A high priced mortgage loan is defined as a loan with an Annual Percentage Rate (APR) higher than the Average Prime Offer Rate for a similar type of loan. A high priced mortgage loan is generally one that has interest rates that are at least 3% above the rates on comparable loans. This type of loan can also have other terms and conditions that make it more expensive than a similar loan with a lower APR.

High priced mortgage loans can be difficult to qualify for, and they can be very expensive. If you’re thinking about taking out a high priced mortgage loan, it’s important to understand all of the costs and risks involved.

What is a High Priced Mortgage Loan?

A high priced mortgage loan is defined as a loan with an annual percentage rate (APR) that exceeds the average prime offer rate by more than 1.5 percentage points for first mortgages, and by more than 2.5 percentage points for subordinate mortgages. The Average Prime Offer Rate (APOR) is an annual survey of conventional first mortgage interest rates in October published by The Federal Reserve Board.

Who is Eligible for a High Priced Mortgage Loan?

A high priced mortgage loan is one where the APR is 1.5 percentage points or more above the yield on a Treasury security of comparable maturity according to the Consumer Financial Protection Bureau. The higher cost must be attributable to fees and points paid by the consumer at or before closing. To be eligible for a high priced mortgage loan, consumers must also meet certain debt-to-income (DTI) thresholds.

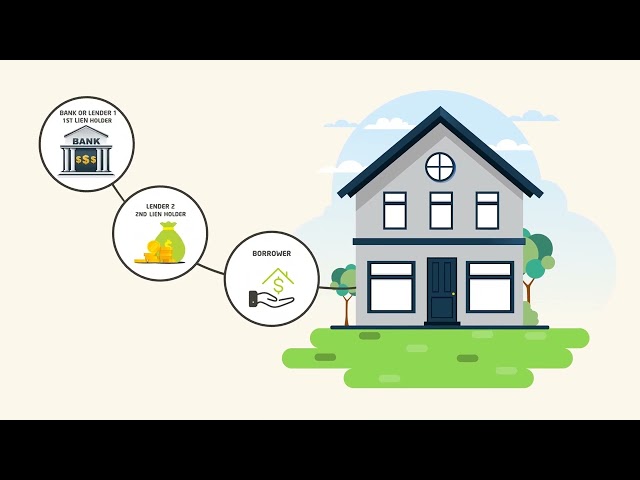

There are two types of loans that are considered high priced: first-lien and subordinate-lien. First-lien loans are those that take precedence over all other claims in the event of foreclosure. Subordinate-lien loans are those that take second place to first-lien loans in the event of foreclosure.

In order for a consumer to be eligible for a high priced mortgage loan, they must have a DTI ratio that does not exceed 43%. The DTI ratio is calculated by taking the borrower’s total monthly debts and dividing it by their gross monthly income.

What are the Benefits of a High Priced Mortgage Loan?

There are numerous benefits of a high priced mortgage loan, such as the ability to:

– Purchase a more expensive home

– Get a lower interest rate

– Receive a larger loan amount

– Access more favorable loan terms

– Build equity faster

If you are considering a high priced mortgage loan, it is important to speak with a knowledgeable mortgage professional to learn more about your options and ensure that you are getting the best possible deal.

What are the Risks of a High Priced Mortgage Loan?

Any mortgage loan where the annual percentage rate (APR) is greater than the Average Prime Offer Rate (APOR) as published monthly by the Federal Housing Finance Agency is considered a high priced mortgage loan.

High priced mortgage loans generally have higher interest rates and fees than other types of mortgages, which can make them more expensive for borrowers. In some cases, high priced mortgage loans can also have terms that are less favorable to borrowers, such as shorter repayment periods or less flexible repayment options.

High priced mortgage loans are sometimes also referred to as subprime mortgages. However, not all high priced mortgage loans are subprime mortgages, and not all subprime mortgages are high priced mortgage loans.

There are a number of risks associated with high priced mortgage loans. For one, borrowers who take out these types of loans may be more likely to experience financial difficulties, which could lead to foreclosure. In addition, high priced mortgage loans may be more difficult to refinance, which could leave borrowers stuck in a loan with unfavorable terms.

For these reasons, it is important for borrowers to understand the risks associated with high priced mortgage loans before taking one out. Borrowers who are considering a high priced mortgage loan should contact several different lenders to compare terms and rates before choosing a loan.

How to Apply for a High Priced Mortgage Loan

If you’re looking for a high priced mortgage loan, there are a few things you’ll need to do in order to get approved. Here’s what you need to know.

In order to apply for a high priced mortgage loan, you’ll need to have a credit score of at least 680. You’ll also need to have a down payment of at least 10% of the home’s value, and you’ll need to be able to show that you can afford the monthly payments.

If you meet all of these requirements, then you should be able to get approved for a high priced mortgage loan.

Conclusion

A high priced mortgage loan is one where the APR is greater than the median prime offer rate for first-lien mortgages as published on Freddie Mac’s weekly Primary Mortgage Market Survey.