What is a HELOC Loan and How Does it Work?

Contents

A home equity line of credit (HELOC) loan is a type of loan that uses the equity in your home as collateral. If you have equity in your home, you can use it as collateral for a HELOC loan.

Checkout this video:

What is a HELOC Loan?

A HELOC loan is a home equity line of credit. It is a loan that is secured by your home equity, and it works similarly to a credit card. You can borrow up to a certain amount, and you only have to pay interest on the amount that you borrow. HELOC loans can be a great way to get access to cash, but they can also be a financial trap if you’re not careful.

What is a HELOC?

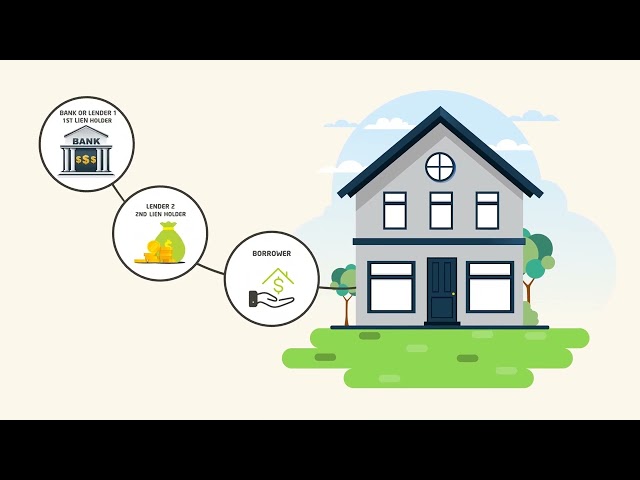

A HELOC is a home equity line of credit. A HELOC is a loan that uses your home’s equity as collateral. Equity is the portion of your home’s value that you own outright, free and clear of any loans. A HELOC allows you to borrow against that value and then pay it back over time, usually in equal monthly payments.

You can think of a HELOC like a credit card: you have a certain amount of money available to you that you can borrow against, and then pay back over time, with interest. The main difference between a HELOC and a credit card is that the interest rate on a HELOC is usually lower than the interest rate on a credit card, and the payments on a HELOC are often tax-deductible (consult your tax advisor to be sure).

Another difference between a HELOC and a credit card is that with a HELOC, you usually have a set period of time (the “draw period”) during which you can borrow money, after which time the loan enters the “repayment period.” With most HELOCs, you can re-borrow money (“re-draw”) after you have repaid some of the loan, up to your credit limit.

How Does a HELOC Work?

A home equity line of credit, or HELOC loan, works much like a credit card. You’re given a line of credit that you can borrow from as needed, up to a certain limit. As you pay back the loan, the line of credit is replenished so you can continue to borrow against it.

The interest rate on a HELOC loan is variable, which means it can go up or down over time. The rate is often based on the prime lending rate, which is the rate banks charge their best customers.

HELOC loans are secured by your home equity, so if you default on the loan, the lender could foreclose on your home. That’s why it’s important to make sure you can afford the payments before you take out a HELOC loan.

If you’re thinking about taking out a HELOC loan, here are a few things to keep in mind:

-HELOC loans can be used for anything – including debt consolidation, home improvement projects, and major purchases like a car or boat.

-HELOC loans typically have lower interest rates than unsecured loans like personal loans and credit cards.

-HELOC loans are flexible – you can borrowed as little or as much as you need, up to your credit limit.

-HELOC loans have repayment terms of 5-20 years.

-HELOC loans are secured by your home equity, so if you default on the loan, the lender could foreclose on your home.

Advantages of a HELOC Loan

A HELOC loan is a home equity line of credit. It is a loan that is secured by the equity in your home. A HELOC loan can be used for a variety of purposes, including home improvements, debt consolidation, and education expenses. There are many advantages of a HELOC loan, which we will discuss in detail.

Lower Interest Rates

HELOC loans typically have lower interest rates than credit cards, personal loans, and other types of loans. This is because the loan is secured by your home equity, which the lender can use to recoup their losses if you default on the loan. The interest rate on a HELOC loan may be fixed or variable, but it will almost always be lower than the interest rate on an unsecured loan.

Access to Home Equity

A home equity line of credit (HELOC) is a type of loan that uses the value of your home as collateral. A HELOC functions as a second mortgage and gives you access to cash based on the equity you have in your home. Equity is the difference between what your home is worth and what you still owe on it.

You can use a HELOC for almost anything, including consolidating debt, paying for home improvements, or covering unexpected expenses. The amount of money you can borrow with a HELOC depends on the appraised value of your home, how much you still owe on your first mortgage, and the loan-to-value ratio (LTV), which is the percentage of your home’s appraised value that a lender will allow you to borrow.

A HELOC typically has a lower interest rate than other types of loans, making it a good choice for borrowers who need to access extra cash but are unable to get a traditional loan. HELOCs also offer flexibility in how you use the funds since you can borrow only what you need, when you need it.

No Closing Costs

One of the main advantages of a HELOC loan is that there are no closing costs. This can save you a significant amount of money, especially if you are taking out a large loan.

Disadvantages of a HELOC Loan

A HELOC loan can be a great way to get the money you need for a home improvement project. However, there are some disadvantages to taking out a HELOC loan. One of the biggest disadvantages is that you could end up owing more money than your home is worth if your home decreases in value.

Higher Interest Rates

HELOCs usually have adjust able rates, which means your payments could go up or down over time. If interest rates rise, your payments could become unaffordable, and you could end up owing more than your home is worth.

Limited Loan Amount

A HELOC loan may have a limited loan amount. This is because the loan is based on the value of your home equity, and your home equity may not be high enough to qualify for a large loan.

Variable Interest Rates

A HELOC loan typically has a variable interest rate, which means that your monthly payments can fluctuate up or down over the course of your repayment period. This can make budgeting for your monthly payments more difficult, as you may not be able to predict exactly how much you’ll need to set aside each month.