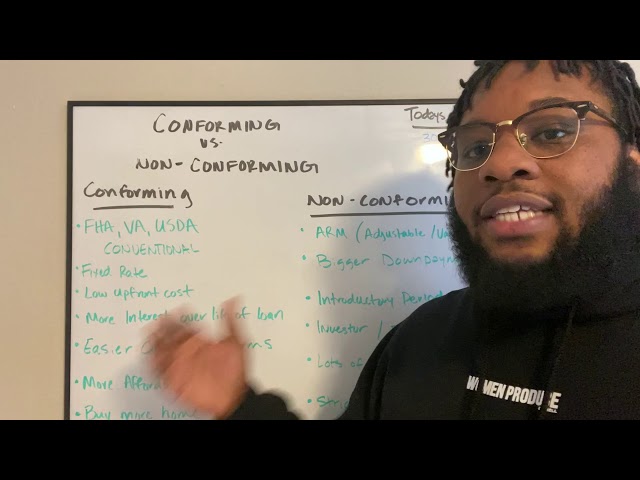

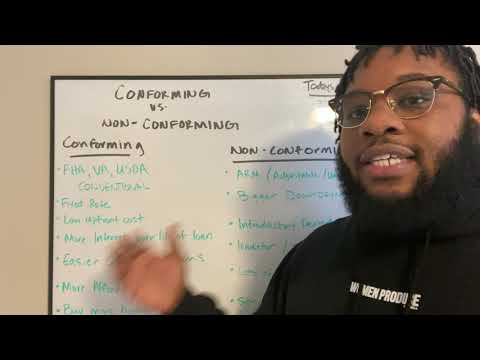

What is a Conforming Fixed Loan?

A Conforming Fixed Loan is a mortgage loan that follows the guidelines set by Freddie Mac and Fannie Mae. These two government-sponsored enterprises purchase loans from lenders, so that they can provide more financing options for homebuyers. Conforming Fixed Loans can be used to purchase a primary residence, a second home, or an investment property.

Checkout this video:

What is a conforming fixed loan?

A conforming fixed loan is a mortgage that follows the guidelines set by the Federal National Mortgage Association (FNMA) or the Federal Home Loan Mortgage Corporation (FHLMC). These guidelines include the loan amount, the loan-to-value ratio, the debt-to-income ratio, the credit score of the borrower, and the type of property.

What are the benefits of a conforming fixed loan?

A conforming fixed loan is a mortgage loan that conforms to the underwriting guidelines set forth by the government-sponsored enterprises Freddie Mac and Fannie Mae. These two organizations purchase the majority of mortgages in the United States, and they set the standards for what types of loans qualify for secondary market purchases. In order to conform to these standards, lenders must adhere to specific guidelines with regard to loan amount, borrower creditworthiness, and other factors.

The benefits of a conforming fixed loan include:

-Loan amounts that are within the maximum limits set by Freddie Mac and Fannie Mae. In most parts of the country, this limit is $417,000 for a single-family home. In high-cost areas, the limit is higher.

-More flexibility with regard to credit score requirements than with non-conforming loans. For a conforming fixed loan, you may be able to qualify with a credit score as low as 620.

-Potentially lower interest rates than with non-conforming loans. Because Freddie Mac and Fannie Mae purchase such a large percentage of mortgages in the United States, lenders can offer lower interest rates on conforming loans in an effort to compete for business.

What are the eligibility requirements for a conforming fixed loan?

To be eligible for a conforming fixed loan, you’ll need to meet certain requirements set by Fannie Mae and Freddie Mac, the government-sponsored enterprises (GSEs) that provide liquidity for the mortgage market. In general, you’ll need to:

-Have a satisfactory credit history

-Show proof of income and employment history

-Demonstrate your ability to repay the loan through a debt-to-income ratio that doesn’t exceed a maximum limit

What are the interest rates for a conforming fixed loan?

A conforming fixed loan is a mortgage where the interest rate does not change over the life of the loan. The monthly payment amount is fixed for the life of the loan, making it easy to budget your monthly expenses. A conforming fixed loan is a good option if you plan to stay in your home for a long period of time.

The interest rates for a conforming fixed loan are typically lower than rates for other types of loans, such as adjustable-rate loans or jumbo loans. This makes a conforming fixed loan a good choice if you are looking for a lower monthly payment.

How to apply for a conforming fixed loan

A Conforming Fixed Loan is a mortgage that is offered by private lenders and banks. The loan is available for those who are looking to buy a home and have a good credit score. This type of loan is perfect for those who are looking for a low interest rate and a fixed monthly payment.

How to find a lender for a conforming fixed loan

A conforming fixed loan is a mortgage loan that follows the guidelines set by Freddie Mac and Fannie Mae. These two government-sponsored enterprises (GSEs) purchase loans that fit their guidelines in order to provide stability to the mortgage industry and make loans more accessible to consumers.

To find a lender for a conforming fixed loan, you can:

-Search for lenders online: There are many online tools that can help you compare lenders and find the best option for you.

-Get referrals from friends or family: Ask people you trust for recommendations of lenders they have used in the past.

-Contact your local housing finance agency: Some state and local governments offer programs to help consumers with their home financing. Contacting your local housing finance agency can help you learn about these programs and connect with participating lenders.

How to compare lenders for a conforming fixed loan

Obtaining a conforming fixed loan is simpler than you may think. Follow these steps to get started.

1) Check your credit score and report.

2) Shop around for the best rates and terms from multiple lenders.

3) Compare offers and choose the loan that best suits your needs.

4) Apply for the loan and provide supporting documentation.

5) Close on the loan and start making payments.

How to apply for a conforming fixed loan

A conforming fixed loan is a mortgage loan that follows guidelines set by government-sponsored enterprises Freddie Mac and Fannie Mae. These guidelines include the size of the loan and its terms and conditions. For example, a typical conforming fixed loan would be for $417,000 and have a 30-year term with a fixed interest rate.

Applying for a conforming fixed loan is similar to applying for any other kind of mortgage loan. The first step is to shop around for a lender that offers this type of loan. Once you’ve found a lender, you’ll need to fill out a loan application and provide the lender with your financial information, including your income, debts, and assets. The lender will then underwrite the loan to determine whether or not you qualify. If you do qualify, you’ll need to pay any associated fees and closing costs and then sign the mortgage documents.