What Does a Soft Credit Check Show?

Contents

Find out what a soft credit check is and what information it may show about you.

Checkout this video:

What is a Soft Credit Check?

A soft credit check is when a company checks your credit report to see if you’re a good candidate for their product or service, but it doesn’t impact your credit score. This is different from a hard credit check, which does impact your score. Soft credit checks are often used when you’re applying for a loan, a credit card, or a new job.

What is a Hard Credit Check?

A hard credit check is when a lender requests a copy of your credit report and scores from the three major credit bureaus.Hard credit checks are also sometimes called “pulls” because the lender “pulls” your credit information from the bureaus. Hard inquiries can stay on your report for up to two years, but they generally only impact your score for the first 12 months.

What Does a Soft Credit Check Show?

A soft credit check is a type of credit check that does not impact your credit score. Soft credit checks are typically used when you are checking your own credit score or when you are applying for a job. If you are applying for a loan, the lender will most likely do a hard credit check, which can impact your credit score.

Personal Information

When you request a soft credit check, the lender will pull your name, address, date of birth, Social Security number and other personal information from the credit bureau. This is the same information that would be included on a hard credit check. The lender may also look at public records to verify your identity and address.

Credit History

A soft credit check is a type of inquiry that does not show up on your credit report and therefore will not affect your credit score. Soft inquiries can be initiated by you or your current creditors and are used to update your account information or to verify your identity. Soft inquiries are also sometimes called soft pulls.

Inquiries

When a lender does a “soft pull” of your credit, it has no effect on your score. Soft inquiries include things like checking your own score, or when you’re rate shopping for a loan.

Hard inquiries occur when you apply for new credit, and they can ding your score slightly. For example, if you’re applying for a new credit card, the issuer will do a hard pull of your report to see if you’re likely to be approved. Hard inquiries stay on your report for two years, but their effect on your score decreases over time.

How Does a Soft Credit Check Differ from a Hard Credit Check?

When you’re applying for a loan or credit card, the lender will almost always do a hard credit check. This type of check will show up on your credit report and can ding your score. A soft credit check, on the other hand, won’t show up on your report and won’t impact your score. So, if you’re just trying to see what kind of credit you may qualify for, a soft credit check is the way to go.

Soft Credit Checks are Not Recorded

A soft credit check is a way to check your creditworthiness without affecting your credit score. Soft inquiries are made when you check your own credit, when a company checks your credit as a part of a pre-approval process, or when you’re rate shopping for a loan. Hard inquiries happen when you actually apply for new credit and the lender requests your full credit report. Applying for several loans or lines of credit in quick succession can hurt your score because it looks like you’re desperately trying to borrow money.

Hard Credit Checks can Affect Your Score

When you apply for a loan or credit card, the lender will likely do a hard credit check, which can ding your score by a few points. But if you’re just shopping around for rates and terms, or you’re preapproved for a loan or credit card, you might encounter a soft credit check instead.

A soft credit check is just like a regular credit check in that it shows your credit history and current standing. The difference is that a soft credit check doesn’t ding your score—so it’s a great way to stay on top of your credit health without affecting your score.

How to Get a Soft Credit Check

A soft credit check, also known as a soft inquiry, is a type of credit check that does not affect your credit score. Soft inquiries are typically used by lenders when they are trying to pre-approve you for a loan or credit card. They can also be used by landlords to check your credit history before approving you for an apartment. So, if you’re wondering how to get a soft credit check, read on.

Free Annual Credit Report

You are entitled to one free annual credit report from each of the three credit reporting bureaus every year. You can request all three reports at once or space them out throughout the year.

AnnualCreditReport.com is the only website that is authorized by federal law to provide you with your free annual credit report.

If you find errors on your credit report, you can disputed them with the credit bureau in charge of your file.

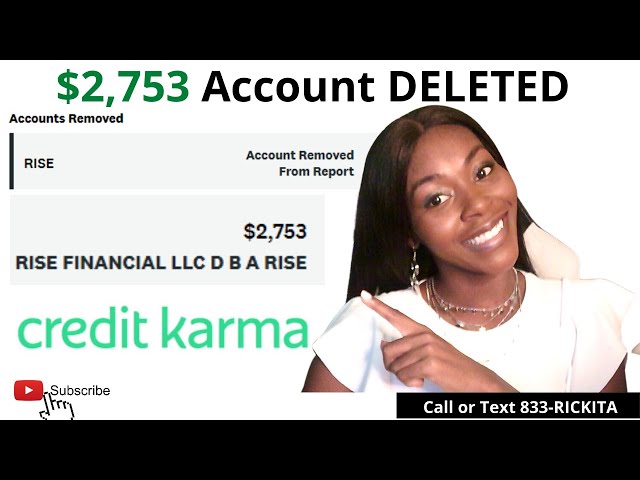

Credit Karma

Credit Karma offers free credit scores, reports and insights. Get the info you need to take control of your credit.

When you check your credit score on Credit Karma, you’ll see information from TransUnion and Equifax, two of the three major credit bureaus. Checking your credit score on Credit Karma is a soft inquiry, which won’t affect your credit score.

A soft inquiry occurs when a company checks your credit report for informational purposes only. Soft inquiries can happen when you check your own credit score or when a company pre-screens you for an offer. Because soft inquiries don’t have any impact on your credit score, you don’t have to worry about them affecting your creditworthiness.

Credit Sesame

A soft credit check is a type of inquiry that does not affect your credit score. Soft inquiries may be generated when you check your own credit, when an employer checks your credit as part of a background check, or when a business checks your credit to pre-qualify you for a service or product. Soft inquiries do not show up on your credit report and are not visible to lenders.

Hard inquiries occur when you apply for new credit and are visible to lenders. Hard inquiries can damage your credit score and too many in a short period of time can indicate to lenders that you are a high-risk borrower.

Soft inquiries will not damage your score, so it’s helpful to know how to generate them. Here are some tips:

Checking Your Own Credit: The best way to generate a soft inquiry is to check your own credit report. You can get a free copy of your report from each of the three major credit reporting agencies (Equifax, Experian and TransUnion) once every 12 months by visiting www.annualcreditreport.com. When you review your report, look for any errors or incorrect information and dispute any inaccuracies with the agency.

Employer Credit Checks: If you consent to an employer checking your credit as part of a background check, this will generate a soft inquiry on your report. Be sure to ask the employer what information they will be looking for and whether they plan to run a hard or soft credit check before giving them permission to access your report.

Pre-Qualifying for Services/Products: Many businesses – including lenders, landlords, cell phone providers and utility companies – will use soft inquiries as part of their pre-qualification process for new customers. For example, if you’re considering applying for a new line of credit, the lender may perform a soft inquiry first to see if you meet their minimum qualifications before asking you to complete a formal application.

How to Interpret a Soft Credit Check

Soft credit checks are a type of credit inquiry that does not impact your credit score. Soft credit checks are often used by lenders to pre-qualify you for a loan or credit card. They can also be used by landlords to check your rental history. A soft credit check will show your credit history, credit score, and any derogatory marks on your report.

Personal Information

When you order a copy of your credit report, you will also receive a score. This is a number that represents your creditworthiness and is used by lenders to determine whether or not to extend you credit. The higher your score, the better your chances of getting approved for a loan or credit card.

A soft credit check is a type of check that does not impact your credit score. Soft checks are typically used for informational purposes, such as when you check your own credit score or when a lender checks your score to pre-qualify you for a loan.

Hard inquiries, on the other hand, are inquiries that do have an impact on your credit score. Hard inquiries can be made by lenders when you apply for a loan or credit card, and they can also be made by landlords, employers, and utility companies.

When you order a copy of your own credit report, it will show both types of inquiries. But if you are just looking at your score, it will only show hard inquiries.

Credit History

There are two types of credit checks — hard and soft. A hard credit check is an inquiry into your credit history that could ding your score, while a soft credit check won’t.

Lenders use information from your credit report to assess your riskiness as a borrower and to set the interest rate they’ll charge on a loan. The report also helps them decide whether to approve you for a loan in the first place. So, when you’re shopping around for a loan, each time a lender does a hard pull on your report, it can cause your score to drop slightly.

Soft pulls are different. They allow lenders to get an idea of your creditworthiness without harming your score. That’s why it’s always best to start your search by doing a few soft pulls on your own report. That way, you can shop around for the best deals without worrying about lowering your score.

It’s important to note that not all inquiries are created equal. Some, like hard pulls for loans or credit cards, can impact your score. Others, like soft pulls made by companies checking your report for pre-screened offers, won’t affect your score at all.

Inquiries

Inquiries are request for your credit report. When you apply for credit, an inquiry is generated. Inquiries remain on your credit report for two years, but only impact your score for the first year. FICO® scoring models count multiple inquiries in a 45-day period as just one inquiry if they’re seeking the same type of loan. So, if you apply for a new car loan and two credit cards within 45 days, FICO® scoring models count all three inquiries as just one when calculating your score.

Inquiries have two types – hard and soft. Hard inquiries occur when you apply for new credit and may lower your score. Soft inquiries occur in other situations, like when you check your own credit or a company checks your credit to pre-qualify you for services. Soft inquiries don’t have an affect on your score but may be seen on your report