If Your Credit Reports Show Different Scores, What Should You Do?

Contents

If you’re trying to improve your credit score, you might be wondering why you have different scores from different credit reporting agencies. Here’s what you should do.

Checkout this video:

Check your credit reports regularly

Your credit score is a three-digit number that’s used to predict how likely you are to pay back a loan on time. Lenders use it to decide whether to approve you for a credit card or loan, and at what interest rate.

If you have multiple credit scores, it’s important to make sure they’re all in the same ballpark. A difference of just a few points could mean paying hundreds of dollars more in interest over the life of a loan.

The most important thing you can do is to check your credit reports regularly. You’re entitled to a free copy of your report from each of the three major credit bureaus – Experian, Equifax and TransUnion – once every 12 months. Check for errors and dispute any inaccuracies you find.

You can also get free monthly updates to your Experian Credit Score by signing up for Experian Boost. When you add utility and cellphone payments to your credit file, you could see your score go up instantly.

Check for errors on your credit reports

If your credit reports show different scores, the first thing you should do is check for errors on your credit reports. If you find any errors, you should dispute them with the credit bureau. You can do this online, by mail, or by phone.

If there are no errors on your credit reports, the next step is to figure out why your scores are different. There are a few reasons why this could happen:

-Different scoring models: There are dozens of different scoring models out there, and each one weights factors differently. So it’s not surprising that you might get a different score from each model.

-Different credit report information: The information in your credit report can change over time, so it’s possible that one report might have updated information that the other doesn’t yet have.

-Different scoring algorithms: Each credit scoring company has its own proprietary scoring algorithm, so it’s not surprising that you might get a different score from each company.

If you’re not sure why your scores are different, you can try contacting the credit bureau or the company that provided the score. They may be able to give you more information about why your scores are different.

Dispute any errors you find on your credit reports

If you find inaccuracies on your credit reports, dispute them with the credit bureau in question. You can do this online, by mail or over the phone. The credit bureau will then have 30 days to respond to your dispute. If they find that the information is indeed inaccurate, they will correct it and send you an updated copy of your report.

If you have different credit scores, focus on the middle score

If you have different credit scores, it’s important to focus on the middle score. The middle score is the one that lenders are most likely to focus on when they’re making lending decisions. If you have a high score and a low score, focus on the middle score. If you have a low score and a high score, focus on the middle score. If you have three different scores, focus on the one in the middle.

Use credit monitoring services to track your credit scores

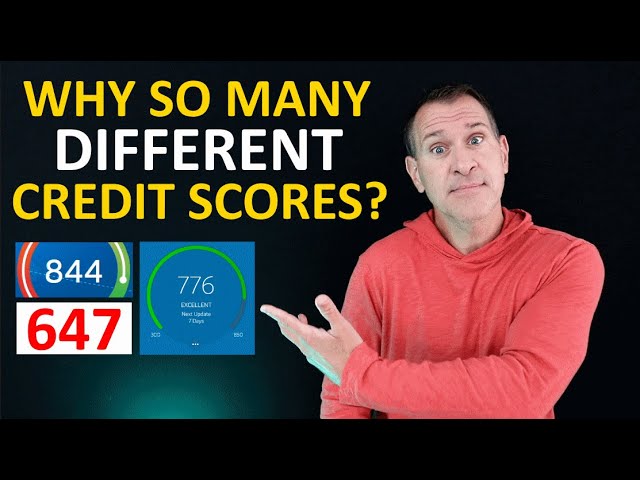

When you check your credit score, you might notice that you have more than one. This is because there are multiple credit reporting agencies, and each one uses a different method to calculate your score.

If your scores are different, don’t panic. There are a few things you can do to figure out why they’re different and what you can do about it.

First, check the date of each report. If one is substantially older than the others, that could be why the scores are different. If that’s the case, you can wait for the older report to be updated before taking any further action.

Second, check the credit utilization on each report. This is the amount of debt you have compared to your available credit, and it’s one of the biggest factors in your credit score. If your utilization is different on each report, that could explain the difference in scores.

If your utilization is high on one report but low on another, you might want to focus on paying down the debt that’s hurting your score the most. On the other hand, if your utilization is low across the board, you might want to consider using a credit monitoring service to track your progress and make sure your scores don’t drop unexpectedly.

Third, check for any errors on your reports. If there are inaccuracies on one or more of your reports, that could explain why your scores are different. You can dispute errors with the credit bureau directly, or you can contact a professional credit repair service to help resolve them for you.

If you notice differences in your scores, don’t panic! There are a few things you can do to figure out why they’re different and what you can do about it. With a little bit of investigation, you should be able to get to the bottom of it and get all of your scores moving in the right direction again.

Take steps to improve your credit scores

If your credit reports show different scores, there are steps you can take to improve your credit scores. Check your credit reports for errors and dispute any errors you find. Also, make sure you’re paying all of your bills on time and keep your balances low. You can also try to get a higher limit on your credit cards, which will help improve your credit utilization ratio. Finally, consider talking to a credit counseling or credit optimization specialist to help you develop a plan to improve your credit scores.