How Your Credit Score is Calculated

Contents

A credit score is a numerical expression based on a statistical analysis of a person’s credit files, to represent the creditworthiness of that person. A person’s credit score is the foundation of their financial health, and it’s important to understand how it’s calculated.

Checkout this video:

What is a credit score?

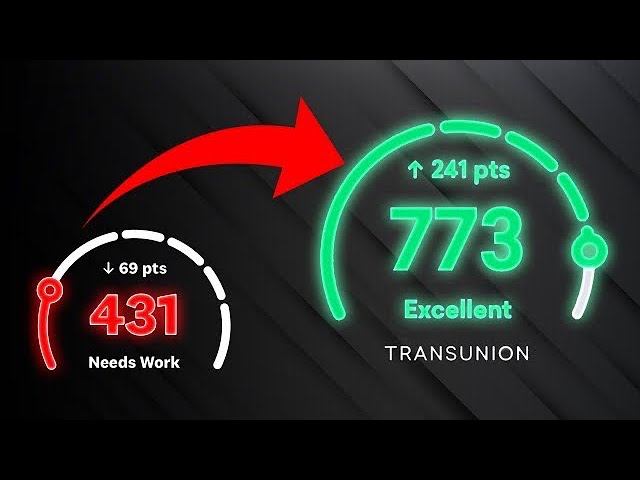

Your credit score is a number that represents your creditworthiness – the higher your score, the more likely you are to be approved for loans and credit cards. A good credit score means you’re a low-risk borrower, which is important to lenders who are considering loaning you money.

There are many different factors that go into calculating your credit score, but the most important ones are your payment history, credit utilization, length of credit history, and types of credit.

How is your credit score calculated?

When you hear the term credit score, you might automatically think of the three-digit number that lenders use to decide whether to give you a loan and how much interest to charge. Your credit score is actually a lot more than that. It’s a mathematical formula that determines your level of financial risk. In other words, it’s a snapshot of your financial health. So, how is your credit score calculated?

Payment history

One of the most important factors in your credit score is your payment history. Your payment history is a record of whether you pay your bills on time. It counts for about 35% of your credit score.

If you have missed payments, it will negatively affect your credit score. It is important to make all of your payments on time, even if you can only afford the minimum payment. Once you have established a good payment history, you can begin to improve your credit score by paying more than the minimum each month.

Credit utilization

Your credit utilization is one of the most important factors in your credit score—it accounts for 30% of your FICO® Score☉ calculation. Credit utilization is the ratio of your credit card balances to your credit limits. It’s important to keep your credit utilization low, because it shows that you’re using a manageable amount of credit and you’re not overextended.

You can calculate your credit utilization by adding up the balances on all of your revolving (credit card) accounts and dividing that number by the sum of your credit limits. For example, say you have two credit cards—one with a $5,000 limit and one with a $3,000 limit. If you carry a balance of $1,000 on the first card and $500 on the second card, your total credit utilization would be:

($1,000 + $500) / ($5,000 + $3,000) = 0.40 or 40%

Ideally, you want to keep your credit utilization below 30%.

Length of credit history

One of the things that affects your credit score is the length of your credit history — that is, how long you’ve been borrowing money and paying it back. Obviously, the longer your history, the better. But if you’re just starting out, don’t worry. As long as you borrowed responsibly in the past and you’re continuing to do so now, your score will gradually improve as your credit history lengthens.

Types of credit

Credit scores are based on the information in your credit reports. Lenders report information to the credit reporting agencies (Equifax, Experian and TransUnion) every month, and that information is used to calculate your credit scores.

There are five categories of information that are used to calculate your credit score:

Payment History: This is the most important factor in your credit score, and even one late payment can negatively impact your score. Your payment history makes up 35% of your FICO score, so it’s important to pay all of your bills on time, every time.

Credit Utilization: This is the second most important factor in your credit score, and it measures how much of your available credit you’re using at any given time. Credit utilization makes up 30% of your FICO score, so it’s important to keep balances low and limits high.

Credit History: This factor measures the length of time you’ve been using credit, and it makes up 15% of your FICO score. So even if you have a low credit utilization ratio, a long history of responsible credit use will help improve your score.

Credit Mix: This factor measures the variety of types of credit you have (credit cards, retail accounts, installment loans, etc.), and it makes up 10% of your FICO score. So having a good mix of different types of Credit accounts is helpful in maintaining a high score.

New Credit: Finally, this factor measures how many new accounts you’ve opened recently, and it makes up 10% of your FICO score. So while it’s good to have a mix of different types of Credit accounts, you don’t want to open too many new accounts at once because that could be interpreted as being desperate for Credit.

How to improve your credit score

Your credit score is important because it is used by lenders to determine whether or not you are a good candidate for a loan. A high credit score means you are a low-risk borrower, which could lead to a lower interest rate on a loan. There are a few things you can do to improve your credit score, such as paying your bills on time, maintaining a good credit history, and using a credit monitoring service.

Make your payments on time

One of the most important things you can do to improve your credit score is to make all your payments on time, every time. A late payment can stay on your credit report for up to seven years and will significantly damage your score. If you’re having trouble making ends meet, contact your creditors as soon as possible and explain your situation. They may be willing to work with you to develop a payment plan that doesn’t strain your budget.

Keep your credit utilization low

Credit utilization is the percentage of your credit limit that you use. It’s important to keep your credit utilization low — under 30% is ideal — because it shows lenders that you’re using a manageable amount of your available credit and are therefore less likely to miss payments or default on your loan.

A good way to keep your credit utilization low is to use your credit card for regular expenses like gas and groceries, but then pay off the balance in full every month. This way, you’re using your credit card regularly but not racking up a lot of debt.

Use a mix of different types of credit

One way to help improve your credit score is by using a mix of different types of credit, such as revolving credit (such as credit cards) and installment loans (such as auto loans). This is because lenders like to see that you can manage different types of credit responsibly. So, if you have both revolving and installment loans, make sure you’re making all your payments on time and keeping your balances low.

Don’t close old credit accounts

One factor that is taken into account when calculating your credit score is the length of your credit history — in other words, how long you have been using credit. Therefore, closing an old credit card account (particularly one that you have had for a long time) can actually hurt your score.