How to Qualify for a Home Loan with Bad Credit

Contents

It is possible to get a home loan with bad credit . There are a few things you can do to improve your chances of qualifying for a home loan.

Checkout this video:

Know Your Score

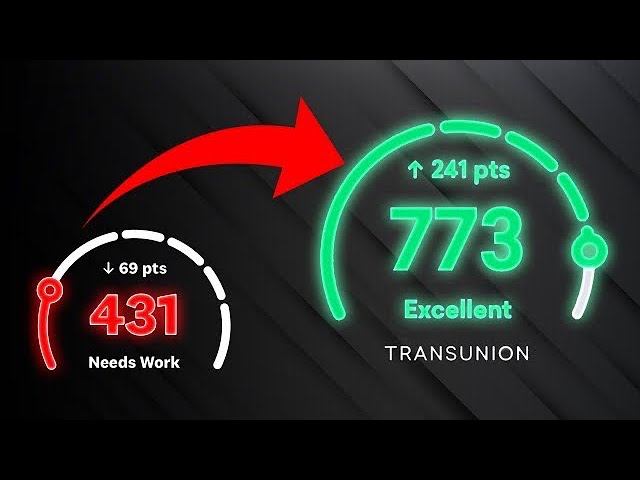

The first thing you need to do is get a sense of where your credit stands. You can get a free credit report from each of the three credit reporting agencies—Equifax, Experian and TransUnion—once a year at AnnualCreditReport.com. Your credit score is a three-digit number that tells lenders how likely you are to repay debt on time. It’s important to know your score because it will affect the interest rate you’re offered on a loan. A higher score indicates to lenders that you’re a lower-risk borrower, which could mean access to better loan terms.

Get a free credit report from Experian

If you’re not sure where your credit stands, the first step is to get a copy of your credit report. You can do this for free once every 12 months from each of the three main credit bureaus—Experian, Equifax, and TransUnion—at AnnualCreditReport.com. Be sure to review your reports carefully for any errors, which can drag down your score. If you spot any inaccuracies, you can file a dispute with the credit bureau.

Check your credit score

If you’re not sure what your credit score is, you can check it for free with Credit Sesame. They will also give you personalized advice on how to improve your credit score. Just sign up for a free account.

Once you know your credit score, you can start taking steps to improve it. If your score is on the lower end, there are still home loan options available to you. The most important thing is to work with a mortgage specialist who can help you understand your options and work with you to get the best loan for your situation.

Find the Right Lender

There are a few key things you can do to help you find the right lender when you have bad credit. One of the most important is to make sure that you are looking for a lender who specializes in helping people with bad credit. This will give you the best chance of getting approved for a loan. Another thing you can do is to make sure that you are looking at all of your options. There are a number of different lenders out there who may be able to help you.

Look for a lender that specializes in bad credit home loans

If your credit score is so low that you’re having trouble qualifying for a conventional mortgage, you may need to look for a lender that specializes in bad credit home loans. These lenders are used to dealing with borrowers with lower credit scores and may be more willing to work with you. You’ll likely pay a higher interest rate if you borrow from one of these lenders, but it may be worth it if you can get a loan that you otherwise wouldn’t qualify for.

Compare interest rates and fees

The first step is to comparison shop among lenders for the best interest rate and fees. Even a small difference in these can add up to a big difference in the amount you’ll ultimately pay for your home loan.

Be sure to compare not just the interest rate but also the Annual Percentage Rate (APR). The APR includes not just the interest rate but also other costs of borrowing, such as points, and is expressed as a percentage of the total loan amount.

You can use an online calculator to compare mortgage APRs. Remember, the lower the APR, the less you’ll pay over time.

You should also compare fees. Some lenders charge origination fees, application fees, or both. Others charge for private mortgage insurance (PMI) if you make a down payment of less than 20%.

Some lenders credit all or part of these fees back to you at closing, but others don’t. So be sure to ask each lender whether they credit fees and how much they credit.

Get Pre-Approved

The first step to qualifying for a home loan with bad credit is to get pre-approved. A pre-approval means that a lender has looked at your credit score and credit history and has determined that you are a good candidate for a loan. This can give you a leg up when you are ready to apply for a loan.

Gather the required documentation

The first step in applying for a home loan is to gather all of the required documentation. This includes your credit reports from all three credit reporting agencies, your bank statements, tax returns for the past two years, pay stubs for the past three months, and any other documentation that may be required by the lender.

Once you have all of the required documentation, you will need to fill out a loan application. Be sure to include all of the required information, such as your social security number, date of birth, employment history, and income.

After you have submitted your loan application, a lender will review it and determine whether or not you qualify for a home loan. If you have bad credit, you may still be able to qualify for a home loan if you have a cosigner or if you are willing to make a larger down payment.

Submit a loan application

A mortgage loan application typically contains detailed information about the applicant, including employment history, income, debts and assets. The loan application is then submitted to one or more lenders in an effort to obtain a loan commitment. The loan commitment is a binding agreement between the lender and the borrower that outlines the terms of the loan.

Improve Your Credit Score

Your credit score is one of the most important factors lenders look at when you apply for a home loan. A high credit score shows lenders that you’re a low-risk borrower, which makes them more likely to approve your loan. If your credit score is low, there are a few things you can do to improve it.

Make all payments on time

One of the most important things you can do to improve your credit score is to make all of your payments on time. This includes credit card payments, utility bills, student loans, and any other type of recurring debt you might have.Missing even one payment can negatively impact your credit score, so it’s important to stay on top of all of your bills. You can set up automatic payments for some debts, which can help you make sure you never miss a payment.

Pay down your debts

One of the best things you can do to improve your credit score is to pay down your debts. This includes both revolving debts, such as credit cards, and installment debts, such as car loans. A good rule of thumb is to keep your credit utilization ratio below 30%. This means that you shouldn’t be using more than 30% of your available credit at any given time.

Another way to improve your credit score is to make sure you always make your payments on time. This includes not only credit card and loan payments, but also utility bills, cellphone bills, and any other type of recurring bill. If you can set up automatic payments for all of your bills, that’s even better.

Shop for Your Home

You can still get a mortgage with bad credit, but you will have to do some shopping around to find the right lender. There are many lenders who are willing to work with people who have bad credit, but they may not offer the best terms. It is important to compare offers from a few different lenders to make sure you are getting the best deal possible.

Find a real estate agent

Start by finding a real estate agent who is familiar with the area where you want to live and with the type of property you are interested in. A good agent will help you focus your search and make sure you don’t waste your time looking at properties that don’t meet your needs.

Next, get pre-qualified for a loan. This will give you an idea of how much house you can afford and also let sellers know that you are a serious buyer. To get pre-qualified, you will need to provide some basic financial information to a lender, such as your income, employment history and current debts.

If you have bad credit, there are still plenty of options for financing your home purchase. You may need to look into special bad credit home loans or work with a mortgage broker who has experience helping borrowers with challenged credit. Either way, it’s important to compare interest rates, fees and terms from multiple lenders before choosing a loan.

Start shopping for your home

Start shopping for your home by looking online and contacting a real estate agent. You should also start working on repairing your credit so that you can get a better interest rate on your loan. You can do this by paying your bills on time, disputing errors on your credit report, and using a credit monitoring service.

If you have bad credit, you may still be able to qualify for a home loan by using a cosigner or applying for a government-backed loan. You can also increase your chances of qualifying by making a larger down payment or having a higher income.