How to Get a Lower APR on Your Credit Card

Contents

It’s no secret that credit card companies are making a killing off of high interest rates. If you’re stuck with a high APR , there are a few things you can do to try to get a lower rate. Check out this blog post to learn more.

Checkout this video:

Check your credit score

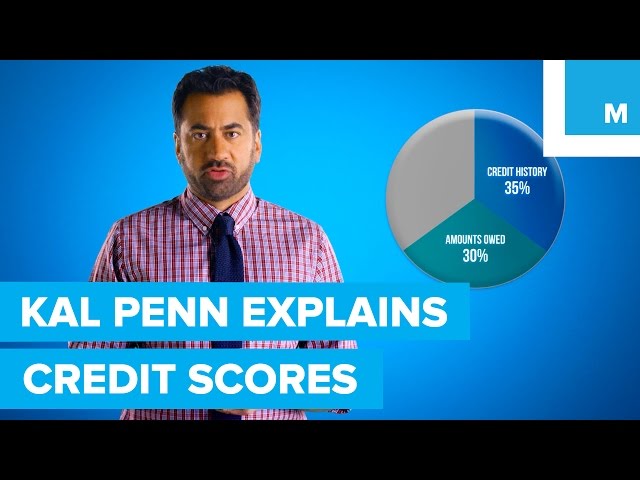

Your credit score is one of the most important factors in determining your APR. If you have a good credit score, you will likely qualify for a lower APR. There are a few things you can do to improve your credit score, such as paying your bills on time, maintaining a good credit history, and using a credit monitoring service.

Get a free credit report

You’re entitled to one free copy of your credit report from each of the three major credit bureaus every 12 months. You can request them all at once, or spread them out over the course of the year. Check your report for accuracy and dispute any errors you find. This is one of the best ways to improve your credit score.

Check for errors

The first step is to check your credit report for errors. You’re entitled to a free copy of your report from each of the three major credit bureaus once every 12 months.

Go through your report line by line to look for any mistakes. If you find errors, dispute them with the credit bureau. It’s important to dispute any errors you find, as they could be lowering your score and costing you money in higher interest rates.

Once you’ve checked for errors, take a look at your credit score and figure out where you stand. If your score is on the lower end, there are still some things you can do to help improve it.

Research your options

If you’re interested in finding a lower APR on your credit card, the first step is to research your options. Start by looking at the offers from your current credit card issuer. You can also look for other credit card issuers that may be willing to offer you a lower APR. Once you’ve found a few options, compare the APRs and choose the one that’s best for you.

Look for cards with 0% APR

There are a few things to consider when looking for a credit card with a low APR. One is the introductory rate, which is the percentage rate you’ll pay on your credit card balance for a certain period of time after you open your account. After that, the APR will usually go up. So it’s important to know how long the introductory period lasts and what the APR will be after that.

Another thing to consider is whether the APR is fixed or variable. A fixed APR means that the rate won’t change during the life of your account. A variable APR means that the rate could go up or down over time, depending on changes in a market index like the prime rate.

If you’re looking for a credit card with a 0% APR, there are a few things to keep in mind. One is that 0% APRs are often only offered for a limited time, typically six to 12 months. After that, the APR will usually go up. So it’s important to know how long the introductory period lasts and what the APR will be after that.

Another thing to consider is whether the 0% APR is for purchases only, balance transfers only, or both. If it’s for purchases only, you’ll still have to pay interest on any balance transfers you make after the intro period ends. And if it’s for balance transfers only, you’ll still have to pay interest on any new purchases you make after the intro period ends.

Finally, keep in mind that most 0% APRs come with balance transfer fees, typically 3% or 5% of the amount transferred. So if you’re thinking about transferring a balance from another card, be sure to factor in these fees when you’re calculating how much money you’ll save with the lower interest rate.

Compare cards with low APRs

When you’re looking for a new credit card, it’s important to compare APRs to find the best deal. The APR is the annual percentage rate charged for borrowing, and it’s one of the most important factors to consider when you’re comparing credit cards. A low APR can save you a lot of money in interest charges, so it’s worth taking the time to find a card with a competitive rate.

You can start by comparing APRs from different issuers to see what kind of rates are available. It’s also important to compare APRs for different types of credit cards, such as balance transfer cards, cash back cards, and rewards cards. You can use our Credit Card Compare tool to see side-by-side comparisons of multiple cards and find the one that offers the lowest APR for your needs.

Once you’ve found a few cards with low APRs, you can start comparing other features to find the best deal. For example, you’ll want to look at annual fees, balance transfer fees, and foreign transaction fees. You should also consider rewards programs and introductory offers when you’re choosing a new credit card. Our tool lets you filter cards by these features so you can find the perfect card for your needs.

getting a lower APR on your credit card is an important way to save money on interest charges. By comparison shopping and looking for cards with low APRs, you can make sure you’re getting the best deal possible.

Consider balance transfer cards

Balance transfer cards can help you save on interest and pay down debt faster. When you open a balance transfer card, you’ll have a set period of time, usually between 3 and 18 months, during which you’ll have a 0% APR on balance transfers. This means you can transfer your existing credit card debt to the new card and pay it off interest-free.

To qualify for a balance transfer card, you’ll need to have good or excellent credit. You’ll also need to have enough available credit on the new card to cover your balance transfer. And remember, even though you won’t be paying interest on your balance during the intro period, you will still be responsible for any fees associated with the balance transfer, so be sure to read the fine print before applying.

Negotiate with your card issuer

Call your card issuer

Calling your card issuer is the best way to try to negotiate a lower APR on your credit card. You’ll want to prepare what you’re going to say before you call, and it’s helpful to have all of your account information in front of you.

Some things you might want to mention to the customer service representative include:

-How long you’ve been a customer

-Whether you’ve always paid your bill on time

-Any recent changes in your financial situation

-Any competitors’ rates that are lower than yours

-What rate you would like them to give you

It can also be helpful to explain why a lower APR would be beneficial for you. For example, if you’re carrying a balance on your card, a lower APR would save you money in interest charges. Or, if you plan on making a large purchase soon, a lower APR would help you keep your payments manageable.

If the customer service representative is not able to lower your APR, they may be able to offer other options, such as a fixed rate for a period of time or an introductory rate for balance transfers. It’s always worth asking about other options even if you don’t think they will be ideal for your needs.

Explain your situation

One way to potentially lower your credit card’s APR is to simply call your issuer and ask. It doesn’t hurt to ask, and you may be surprised at how willing they are to work with you.

When you call, be prepared to explain your current financial situation and why you are struggling to make your payments. If you have a history of making on-time payments, be sure to mention that. The goal is to show the issuer that you are a good customer who is struggling right now and that a lower APR would help you get back on track.

If the issuer agrees to lower your APR, be sure to get the agreement in writing before you make any more payments on your account. This will protect you if there is ever any dispute about the terms of your agreement.

Ask for a lower APR

If you have a good history with your credit card issuer, you may be able to get a lower APR by asking. The worst that can happen is that they say no, so it’s worth a try.

You can also try negotiating your APR if you’ve been late on a payment or gone over your credit limit. In these cases, the issuer may be more willing to work with you because they don’t want to lose your business.

If you have good credit, you may be able to transfer your balance to a card with a lower APR. This only makes sense if you’ll be able to pay off the balance before the intro period ends, otherwise you’ll just end up paying more in interest.