How to Get a Loan from a Credit Union

Contents

Credit unions offer great rates on loans and are a great alternative to banks. Learn how to get a loan from a credit union.

Checkout this video:

Introduction

Credit unions are a great alternative to banks when you’re looking for a loan. Credit unions are usually smaller, community-based organizations that are focused on providing good rates and service to their members. Because credit unions are not-for-profit organizations, they often have lower fees and rates than banks.

Getting a loan from a credit union works pretty much the same as getting a loan from a bank. The first step is to become a member of the credit union. You can do this by opening up a savings account with them. Once you’re a member, you can then apply for a loan.

The process of getting a loan from a credit union is similar to the process of getting a loan from a bank. You’ll need to fill out an application and provide some documentation, such as proof of income and assets. The credit union will then review your application and make a decision about whether or not to approve your loan.

If you’re approved for the loan, you’ll need to sign some paperwork and agree to the terms of the loan. Make sure that you understand all of the terms before you sign anything! Once you’ve signed the paperwork, the money will be deposited into your account and you can start using it right away.

Just like with any other type of loan, it’s important to make your payments on time and in full. If you miss payments or default on the loan, your credit score will suffer and it will be more difficult to get loans in the future. Make sure that you can afford the monthly payments before taking out any loans!

What is a Credit Union?

A credit union is a financial cooperative that is owned and controlled by its members. Credit unions provide a safe place to save and borrow at reasonable rates. They are not-for-profit organizations that exist to serve their members, not to make a profit for outside shareholders. Because credit unions are member-owned, they return earnings to their members in the form of higher dividends on savings, lower loan rates, and exclusive member benefits.

How to Join a Credit Union

A credit union is a nonprofit financial institution that is owned and controlled by its members. Credit unions offer the same financial services as banks, but they are usually much smaller. Because credit unions are nonprofits, they usually have lower fees and rates than banks.

To join a credit union, you must first meet their eligibility requirements. Most credit unions have membership requirements that are based on where you live, work, or go to school. Some credit unions also require that you have a certain amount of money deposited with them before you can join.

Once you have met the eligibility requirements, you can open an account with the credit union. Once your account is open, you will be able to use all of the credit union’s services, including taking out loans.

How to Get a Loan from a Credit Union

Credit unions are a great option if you’re looking for a loan. They are typically more willing to work with you if you have bad credit and they offer competitive rates. Here’s how to get a loan from a credit union:

1. Join the credit union. You will need to become a member of the credit union in order to apply for a loan. This usually requires opening up a savings account with them and making a small deposit.

2. Talk to a loan officer. Once you’re a member, you can speak to a loan officer about your options. They will be able to help you choose the right type of loan for your needs and they will also let you know what the interest rate will be.

3. Apply for the loan. The loan officer will help you fill out the application and they will also pull your credit report.

4. Get approved for the loan. Once you’re approved, you’ll need to sign the loan agreement and then the money will be deposited into your account.

Types of Loans Offered by Credit Unions

Credit unions offer a wide variety of loan products at very competitive rates. Here are some of the most common types of loans offered by credit unions:

-Auto loans: Credit unions offer both new and used auto loans at rates that are typically lower than what you’d find at a bank or other financial institution.

-Personal loans: Personal loans from credit unions are often used for debt consolidation, home repairs, or other major expenses. The interest rates on personal loans from credit unions are usually much lower than those offered by banks.

-Mortgages: Credit unions offer a wide variety of mortgage products, including fixed-rate mortgages, adjustable-rate mortgages, and home equity loans. Credit union mortgage rates are typically lower than those offered by banks.

-Student loans: Credit unions offer student loans at competitive rates to help you pay for college.

Repaying Your Loan

Once you have been approved for a loan from your credit union, you will need to start repaying the loan according to the terms of your agreement. Most loans from credit unions have fixed repayment terms, which means you will make the same payment each month for the duration of the loan.

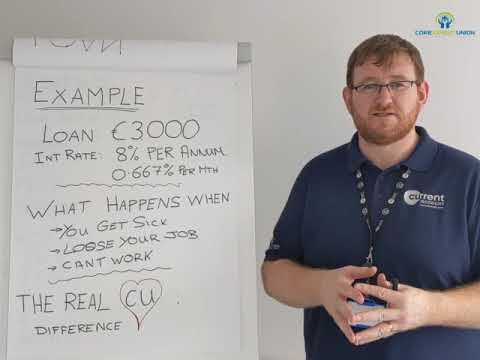

Your monthly payment will be composed of two parts: principal and interest. The principal is the amount of money you borrowed, while the interest is the fee charged by the credit union for lending you the money. Your monthly payment will stay the same until your loan is paid off in full.

If you made a down payment on your loan, your monthly payments will be lower because you will only be repaying the amount you borrowed, minus your down payment. For example, if you borrowed $10,000 for a car and made a $2,000 down payment, your monthly payments would be based on an $8,000 loan balance.

It’s important to make all of your payments on time in order to avoid defaulting on your loan. If you default on your loan, your credit score will suffer and you may have difficulty qualifying for loans in the future. In extreme cases, defaulting on a loan can lead to wage garnishment or seizure of assets.

If you are having trouble making your payments, contact your credit union right away to discuss alternatives such as refinancing or deferring payments. Most credit unions are willing to work with their members to make sure they can meet their financial obligations.