How to Figure Interest Rates on Loans

Contents

- Introduction

- How to Figure Interest Rates on Loans

- What is the Loan’s Annual Percentage Rate (APR)?

- What is the Loan’s Interest Rate?

- What is the Loan’s Principal?

- How to Figure Interest Rates on Loans

- .1 Step One: Determine the Loan’s APR

- .2 Step Two: Determine the Loan’s Interest Rate

- .3 Step Three: Determine the Loan’s Principal

- Conclusion

You can use this calculator to figure out the monthly payments on a loan. Just enter in the loan amount, interest rate, and term of the loan, and the calculator will do the rest.

Checkout this video:

Introduction

Interest rates can be complex and confusing, but it’s important to understand them if you’re thinking about taking out a loan. The interest rate is the amount of money that the lender charges you for borrowing money, and it can vary depending on the type of loan, the length of the loan, and other factors.

In this article, we’ll explain how to figure out the interest rate on a loan, what factors influence interest rates, and some tips for getting the best interest rate possible.

How to Figure Interest Rates on Loans

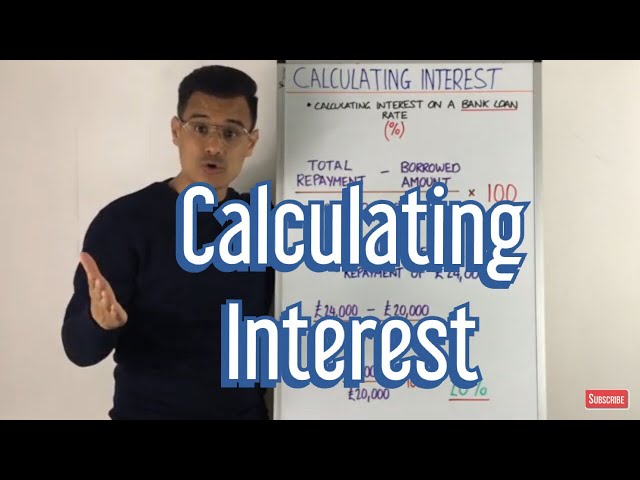

The interest rate on a loan is the cost of borrowing money, expressed as a percentage of the loan amount. The interest rate is usually a percentage of the loan amount, but it can also be a flat fee. You can use this calculator to figure out the interest rate on your loan.

What is the Loan’s Annual Percentage Rate (APR)?

The interest rate is the cost of borrowing the money, and is expressed as a percentage of the total loan amount. The APR includes the interest rate plus any other fees that might be charged, such as an origination fee.

To calculate the APR on a loan, divide the interest rate by the number of payments you’ll make in a year. The resulting number is called the periodic rate. Next, add any additional fees to that number, and multiply it by the number of payments you’ll make in a year. This will give you your APR.

What is the Loan’s Interest Rate?

The interest rate is the amount charged, expressed as a percentage of principal, by a lender to a borrower for the use of assets. The rate is calculated by dividing the interest paid on a loan by the principal amount of the loan. The percentage can be represented in terms of an annual rate (the annualized rate), which reflects the fact that loans generally compound interest monthly or semi-annually.

What is the Loan’s Principal?

The principal is the amount of money you borrow from a lender. The principal is what you’ll need to pay back, plus interest. It’s important to remember that the more money you borrow (the higher the principal), the more interest you’ll have to pay.

How to Figure Interest Rates on Loans

To calculate the interest rate on a loan, you need to know the loan’s principal amount, the length of time it will take you to repay the loan, and the loan’s annual percentage rate (APR). The APR is the yearly cost of borrowing money, including interest and fees, expressed as a percentage.

Here’s how to calculate the interest rate on a loan:

First, divide the APR by 100 to get a decimal figure. For example, if the APR is 5%, then 5 divided by 100 equals 0.05.

Next, add 1 to that figure. In our example, 0.05 plus 1 equals 1.05.

Now, raise that figure to the power of the number of years you’ll be repaying your loan. So if you’re taking out a three-year loan at 5% APR, 1.05 raised to the third power equals 1.157 or 11.57%. That’s your interest rate for three years.

.1 Step One: Determine the Loan’s APR

Annual percentage rate (APR) is a measure that attempts to calculate what percentage of the loan will be paid in interest over the course of a year. It is important for consumers to be aware of this number because it will help them understand the true cost of borrowing money. The APR takes into account not only the interest rate but also other fees and charges associated with the loan, such as points, origination fees, and closing costs.

To calculate the APR on a loan, divide the total amount of interest paid by the total amount borrowed. This will give you the APR as a percentage. For example, if you borrow $100 at an interest rate of 5% and pay $5 in interest over the course of a year, your APR would be 5%.

.2 Step Two: Determine the Loan’s Interest Rate

The interest rate you’ll pay on a loan is determined by a number of different factors. The most important factor is usually the “prime rate,” which is the rate banks charge their best customers. Other factors include the size of the loan, the term of the loan, and your credit history.

To get an idea of what interest rate you might be charged, start by finding out the prime rate. You can do this by checking in the business section of your local newspaper, or by visiting a financial website like Yahoo! Finance or Bankrate.com. Once you know the prime rate, add about 3 percentage points to that number to get a general idea of what kind of interest rate you’ll be charged on a loan.

For example, if the prime rate is 5%, you can expect to pay an interest rate of 8% on a loan. If you have good credit, you might be able to get a lower interest rate; if you have bad credit, you might be charged a higher interest rate.

Once you know what kind of interest rate you’re likely to be charged, you can use that information to compare different loans and choose the one that’s right for you.

.3 Step Three: Determine the Loan’s Principal

The principal of a loan is the initial amount borrowed plus any additional amount that is borrowed later through refinancing or taking out a second mortgage. For example, if you take out a $100,000 loan and later refinance for $150,000, your principal is $250,000. In addition, any fees charged by the lender at closing are added to the principal.

Conclusion

The interest rate on a loan is determined by a number of factors, but the most important factor is the creditworthiness of the borrower. Other factors that can influence the interest rate include the type of loan, the size of the loan, and the term of the loan.