How to Calculate the Total Interest on Your Car Loan

Contents

If you’re thinking about taking out a car loan, you’re probably wondering how much interest you’ll end up paying. In this blog post, we’ll show you how to calculate the total interest on your car loan so that you can make an informed decision.

Checkout this video:

Introduction

Most car loans are simple interest loans. That means that the interest you pay each month is based only on the outstanding balance of your loan, not on the full amount you originally borrowed. So, if you make extra payments to principal each month, your loan balance will go down and so will the amount of interest you pay. The result is that you’ll pay less total interest over the life of your loan. Here’s how to calculate the total interest you’ll pay on your car loan.

How to calculate the total interest on your car loan

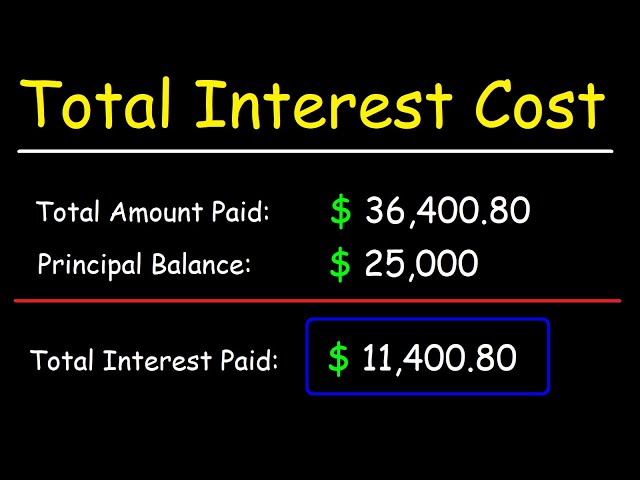

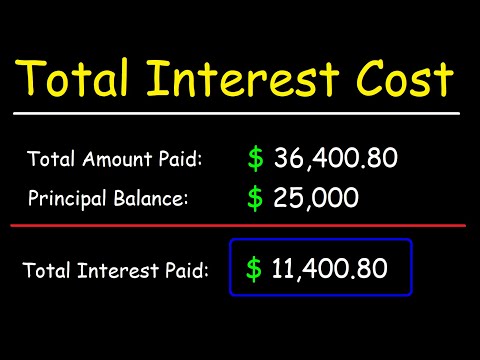

The total interest on your car loan is the amount of money that you will pay in interest over the life of your loan. To calculate the total interest, you will need to know the interest rate, the term of the loan, and the amount of the loan. You can use an online calculator or a simple formula to calculate the total interest.

Find the purchase price of the car

You’ll need to know the purchase price of the car to calculate the total interest on your loan. The purchase price is the sticker price of the car minus any rebates or down payment you made. For example, if you bought a car for $20,000 and made a $2,000 down payment, your purchase price would be $18,000.

Find the APR

The best way to find the APR of your car loan is to look at the loan contract. You should be able to find the APR listed as an annual percentage rate (APR). If you can’t find the APR, you can use our car loan calculator to estimate your monthly payments and total interest.

If you have a good credit score, you might be able to get a lower APR on your loan. Check your credit score for free with Credit Sesame to see where you stand.

Find the loan term

The loan term is the amount of time you have to pay back your loan. In most cases, the loan term is expressed as the number of months you have to make payments. For example, if you have a 60-month loan, that means you will make 60 monthly payments, or 5 years’ worth of payments. The loan term affects the total amount of interest you will pay on your loan. In general, the longer the loan term, the more interest you will pay.

To calculate the total interest on your car loan, you need to know the following information:

-The principal amount of your loan (the amount you are borrowing)

-The annual percentage rate (APR) of your loan

-The length of your loan term (in months)

Use an online calculator

If you’re not comfortable doing the math yourself, or if you want to check your work, there are online calculators that will do the heavy lifting for you. All you need to know is your loan amount, interest rate, and loan term (in months).

One popular online calculator is Bankrate’s “Total Car Cost Calculator.” To use it, enter your loan amount, interest rate, and loan term in months. The calculator will then give you the total interest you will pay over the life of your loan.

Another option is Edmunds’ “True Cost to Own Calculator.” This calculator not only gives you the total interest on your car loan, but it also factors in other costs like depreciation, insurance, taxes, and fuel. This can give you a more accurate picture of what it will really cost to own your car over the long haul.

Conclusion

Assuming you’re happy with your car and don’t plan to trade it in or sell it before the loan is paid off, the easiest way to calculate the total interest you’ll pay on your loan is simply to multiply your loan’s interest rate by the number of months you’ll be making payments. For example, if you have a 60-month loan at an interest rate of 6.5%, your calculation would look like this:

Total Interest = Interest Rate x Number of Months

Total Interest = 0.065 x 60

Total Interest = 3.9%

In this example, the total interest comes to just under 4%. Keep in mind that this is only an estimate, as there are a number of factors that can influence the total amount of interest you’ll actually pay over the life of your loan, including extra payments, fees, etc.