How to Calculate Your Loan Payment in Excel

Contents

If you’re taking out a loan, it’s important to know how much your monthly payments will be. You can use Excel to calculate your loan payment easily. Just follow these steps:

Checkout this video:

Introduction

If you’re planning to take out a loan, you’ll need to know how to calculate your loan payment. Fortunately, this is easy to do in Microsoft Excel. With just a few clicks of the mouse, you can easily calculate your loan payment using Excel’s built-in PAX function. Here’s how:

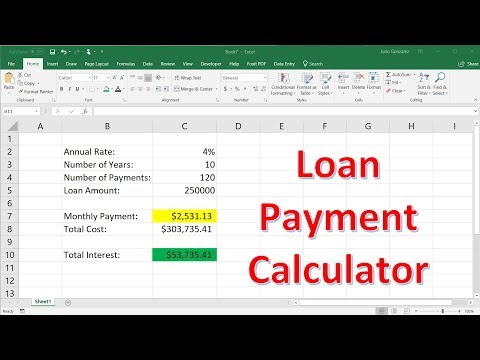

First, open up a new workbook in Excel. Then, enter the following information into cells A1 through A6:

A1: Loan amount

A2: Annual interest rate

A3: Loan term (in years)

A4: Monthly payment

A5: Total interest paid

A6: Total payments made

Now, in cell A4, enter the following formula: =PMT(A2/12,A3,-A1) This will calculate your monthly loan payment. Be sure to replace “A2” with the appropriate cell number for your annual interest rate, and “A3” with the appropriate cell number for your loan term. Finally, replace “A1” with the appropriate cell number for your loan amount. Once you’ve entered the formula, press Enter and your monthly loan payment will be displayed in cell A4.

The basics of loan payments

Principal

Your loan payment consists of both principal and interest, and the amount of each may vary throughout the life of your loan. Principal is the sum of money you borrowed from your lender that forms the basis of your loan. Interest is the fee charged by your lender for borrowing money.

To begin, enter the following formula into any blank cell:

=pmt(rate, nper, pv, [fv], [type])

This function will calculate your monthly loan payment. Here is a breakdown of each component in this function:

rate: The interest rate per period for this loan. To calculate monthly interest rate, divide your annual interest rate by 12 (the number twelve).

nper: The total number of payments for this loan. To calculate the number of payments you will make on a loan, multiply the number of years by 12 (the number twelve).

pv: The present value or principal balance of your loan. This is the amount you borrowed from your lender. To calculate the present value of a loan, simply subtract any upfront fees or charges from the total amount you borrowed.

fv: The future value or payoff amount for this loan. This is optional because most loans are paid off in full by the end of their term. If you do include it in your calculation, be sure to enter “0” (zero) if you would like to pay off your loan in full at the end of its term.

type: The number 0 (zero) or 1 (one). This indicates when payments are due. Type 0 means that payments are due at the beginning of each period (this is also called a “balloon” payment). Type 1 means that payments are due at the end of each period.

Interest

Interest is the cost of borrowing money, and it is typically expressed as a percentage of the total loan amount. The interest rate is the rate at which interest accrues on the outstanding balance of the loan. The effect of compounding interest is that the borrower pays not only on the principal loan amount, but also on the accumulated interest from previous periods.

Compounding can occur daily, monthly, quarterly, or yearly, and it can have a significant impact on the total amount of interest that is paid over the life of the loan. For example, if you have a $1,000 loan with a 5% annual interest rate and monthly compounding, you will pay $50 in interest during the first year. In the second year, you will pay interest on both the original principal and on the $50 in accumulated interest from the first year, for a total of $52.50 in interest.

To calculate your monthly loan payment in Excel, you can use either the PMT function or the IPMT function. The PMT function calculates the payment for a loan based on constant payments and a constant interest rate, whereas IPMT calculates the payment for an installment loan that has periodic payments (such as a mortgage or car loan).

The PMT function takes the following arguments:

-The rate argument is the annual interest rate divided by 12 (the number of months in a year). For example, if you have a 5% annual interest rate, your monthly rate would be 0.05/12 or 0.004167.

-The nper argument is he number of payments over the life of he loan. For example, if you have a 30-year mortgage with monthly payments, your nper would be 360 (30 years x 12 months). , To calculate your mortgage payment using Excel’s PMT function:

In cell A1 enter: =PMT(A2/12,A3,-A4)

In cell A2 enter: your mortgage’s annual percentage rate (APR)

In cell A3 enter: 360 (the number of payments over 30 years) ÷ 12 =30 years x 12 months in a year =360 payments

In cell A4 enter: -100000 (the negative value of your home’s purchase price)

Loan terms

Loan terms are the conditions under which a borrower agrees to repay a loan. They include the length of the loan (the number of payments), the interest rate, and whether the interest will be simple or compound. Loan terms also include any fees or penalties associated with early repayment, such as a prepayment fee.

How to calculate your loan payment in Excel

If you’re like most people, you probably don’t want to think about how much money you’re spending on your loan payments each month. But if you’re trying to get a handle on your finances, it’s important to be aware of all your expenses. That’s where Excel comes in. With a few simple steps, you can easily calculate your loan payment in Excel.

Entering the loan information

To calculate your loan payment in Excel, you will need to enter some information about the loan into the spreadsheet. The most important piece of information is the loan amount, which is the total amount that you borrowed from the lender. You will also need to enter the interest rate on the loan, which is the percentage of the loan that you will be charged in interest each year. finally, you will need to enter the term of the loan, which is the number of years that you have to pay back the loan.

Calculating the principal and interest

The following formula can be used to calculate the monthly principal and interest payment for a loan:

Principal + Interest Rate / Number of Payments = Payment Amount

For example, if you have a loan with a principal of $1,000 and an interest rate of 5%, and you make 12 payments per year, your monthly payment would be calculated as follows:

$1,000 + 5% / 12 = $83.33

Calculating the loan payment

Formula for calculating the monthly payment on a loan:

A = L * P * (1 + P)^N / ((1 + P)^N – 1)

Where:

A = Monthly payment

L = Loan amount

P = Interest rate (as a decimal)

N = Total number of payments

For example, if you have a $1000 loan at an annual interest rate of 10%, and you want to know what your monthly payments would be over the course of 3 years, you would use the following formula:

A = 1000 * 0.1 * (1 + 0.1)^36 / ((1 + 0.1)^36 – 1)

To calculate this in Excel, you can use the “PMT” function as follows:

=PMT(0.1/12, 36, 1000)

Conclusion

Assuming that you make all of your payments on time, you will eventually pay off your loan. The length of time it takes to pay off your loan depends on the interest rate, the amount you borrowed, and the frequency of your payments.

You can use Excel to calculate your loan payment. To do so, you’ll need to input the following information into separate cells:

-The amount you borrowed (the principal)

-The annual interest rate on your loan

-The number of years you have to repay your loan

-The number of payments you make per year