How to Calculate Interest Payments on a Loan

Contents

Interest payments on a loan can be calculated using the loan’s interest rate, term, and principal. This guide will show you how to calculate interest payments on a loan so that you can make informed financial decisions.

Checkout this video:

Introduction

When you take out a loan, you agree to pay back the principal (the amount you borrow) plus interest. Interest is the cost of borrowing money, and it’s usually expressed as a percentage of the principal.

The amount of interest you pay will depend on the interest rate charged by your lender, the length of your loan, and the amount you borrow. In this article, we’ll show you how to calculate interest payments on a loan.

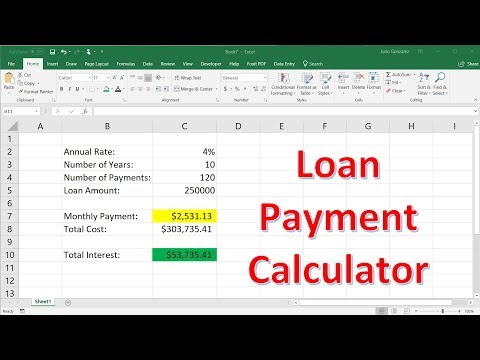

The Basic Formula for Calculating Interest

Interest is calculated based on the amount of money you borrow, the interest rate and the number of days that elapse between interest accruals. To calculate simple interest on a loan, use this formula:

I=Prt

where I equals the interest charged, P equals the principal (the initial amount you borrow), r equals the annual interest rate and t equals the number of years you borrow the money. Note that t is expressed as a decimal in this equation; for example, if you’re borrowing money for two years, use 2.0 as your t value (2 years x 365 days = 730 days).

How to Calculate Interest on a Loan

Interest on a loan is the amount of money that a lender charges a borrower for the use of the money that has been loaned. The interest rate is the percentage of the loan amount that is charged as interest. To calculate the interest payments on a loan, you need to know the loan amount, the interest rate, and the term of the loan.

Simple Interest

Simple interest is the amount of interest paid on a loan, calculated as a percentage of the principal (the amount borrowed).

To calculate simple interest on a loan, you multiply the principal by the annual interest rate, expressed as a decimal. For example, if you take out a $100 loan with a 10% annual interest rate, you would calculate the interest payments as follows:

$100 x 0.10 = $10

This means that you would owe $10 in interest after one year. If you wanted to calculate the total amount you would owe after two years, you would simply multiply the original loan amount by the number of years:

$100 x 2 = $200

With simple interest loans, your monthly payments will only go toward paying off the interest accrued during that month. Principal and interest are not paid down simultaneously as they are with amortizing loans.

Compound Interest

If you take out a loan with compound interest, you’ll pay interest not only on the money you borrowed, but also on the interest that has accumulated so far. That means your total debt will grow bigger, and you’ll end up paying interest on that larger amount of debt. This can add up to a lot of money over time!

To calculate compound interest, start by finding the principal, which is the amount of money you borrowed. Then, find the rate of interest, which is usually presented as a percentage. To make things easier, convert this to a decimal by moving the decimal point two places to the left. For example, if the rate of interest is 5%, you would convert it to 0.05.

Next, find the number of times per year that interest is compounded. This is typically once per year, but it could be more often. Finally, determine the length of time over which the loan will be repaid.

Once you have all of this information, you can use the following formula to calculate compound interest:

Compound Interest = P * (1 + r/n)^(nt) – P

where:

-P = principal

-r = rate

-t = time in years

-n = number of times per year that interest is compounded

Conclusion

Calculating interest payments on a loan can be a tricky process, but it is important to understand how to do it in order to make smart financial decisions. The good news is that there are online calculators and other tools that can make the process easier. With a little time and effort, you can learn how to calculate interest payments on a loan like a pro!