How to Calculate a Home Equity Loan

Contents

Home equity loans are a great way to get extra cash when you need it. But how do you know how much you can borrow? This quick and easy guide will show you how to calculate a home equity loan so you can get the money you need.

Checkout this video:

Home Equity Loan Basics

A home equity loan is a type of loan in which the borrower uses the value of their home as collateral. The loan amount is determined by the value of the home, the borrower’s creditworthiness, and the loan-to-value ratio. A home equity loan can be a great way to finance a major purchase or home improvement project.

What is a home equity loan?

A home equity loan is a loan in which the borrower uses the equity of his or her home as collateral. The loan amount is determined by the value of the property, and the value of the property is determined by an appraiser from the lending institution. Equity is the difference between the appraised value of the property and the amount still owed on the mortgage. For example, if your home is worth $250,000 and you owe $150,000 on your mortgage, you have $100,000 in equity.

How does a home equity loan work?

A home equity loan is a type of second mortgage. Your first mortgage is the one you used to purchase your home, but you can place additional loans against the property as well known as a home equity loan in most cases. Home equity loans allow you to borrow against your home’s value over the amount of any outstanding mortgages against the property.

This type of loan is often used to finance major expenses such as home repairs, medical bills, or college education. A home equity loan is a good choice if you have a substantial amount of equity in your home and you need a large lump sum of cash. With this type of loan, you can borrow up to 85% of your home’s value, minus any outstanding mortgage balances.

Assuming your credit is good, you can usually qualify for a competitive fixed interest rate, and you could even take advantage of tax-deductible interest payments. Keep in mind that since a home equity loan places a second mortgage on your home, it’s important to be sure that you can afford the monthly payments in addition to any other debts or financial obligations you may have

What are the benefits of a home equity loan?

A home equity loan is a great way to finance major expenses. Homeowners can use home equity loans to pay for renovations, repairs, or even college tuition.

There are several benefits of taking out a home equity loan, including:

-Home equity loans usually have lower interest rates than other types of loans.

-Home equity loans can be used for a variety of purposes, including home improvements, consolidating debt, or paying for college tuition.

-Home equity loans can be used as emergency funds in case of financial hardship.

-The interest paid on a home equity loan may be tax deductible (consult your tax advisor to see if you qualify).

How to Calculate a Home Equity Loan

A home equity loan is a great way to get the money you need for a home improvement project, consolidate debt, or anything else. But how do you know how much you can borrow? The answer is to calculate your home equity loan. In this article, we’ll show you how to do just that.

Determine the value of your home

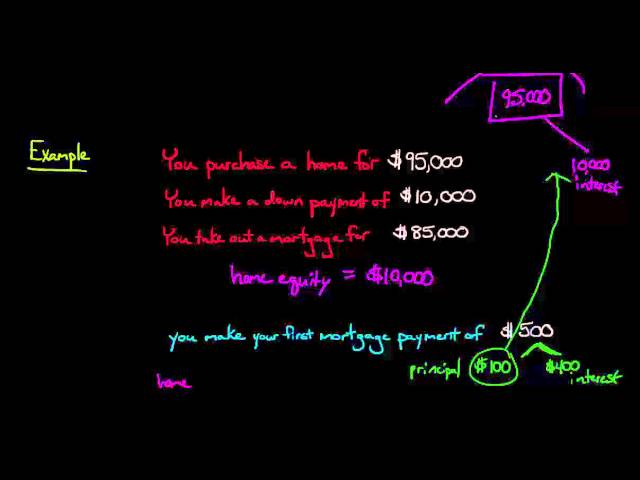

To calculate a home equity loan, you first need to determine the value of your home. Subtract any outstanding mortgage or lien balance from the appraised value or market value of your home to determine your equity.

For example, let’s say your home is worth $250,000 and you have an outstanding mortgage balance of $150,000. This would leave you with $100,000 in home equity.

Once you know how much equity you have available, you can begin to compare loan options and estimate how much money you could borrow.

Determine the amount of equity you have in your home

To calculate your home equity, you will need to know the current appraised value of your home and the outstanding balance on your mortgage. You can find this information on your most recent mortgage statement or by contacting your mortgage lender.

Once you have this information, you can use a home equity calculator to determine the amount of equity you have in your home. There are a number of online calculators that you can use for this purpose.

Once you know the amount of equity you have in your home, you can proceed to the next step in calculating a home equity loan.

Calculate the loan-to-value ratio

The loan-to-value ratio is the loan amount divided by the appraised value of the property. For example, if your home is worth $150,000 and you owe $120,000 on your mortgage, your home equity would be $30,000. To calculate the loan-to-value ratio, divide the loan amount by the appraised value of the property. In this example, you would get a LTV ratio of 80%.

Determine the loan amount you can qualify for

Before you begin shopping for a home equity loan, you need to know how much money you can realistically afford to borrow. This number is generally 60% to 80% of your home’s appraised value, less any outstanding home equity loan balances.

For example, if your home is appraised at $300,000 and you owe $100,000 on your first mortgage, you have $200,000 in equity. Subtracting 10% ($20,000) for closing costs leaves you with a maximum loan amount of $180,000.

Tips for Applying for a Home Equity Loan

A home equity loan is a great way to get the money you need for a major purchase, such as a home renovation. But how do you know if you qualify for one? And what’s the process for applying for a home equity loan? Let’s take a look at some tips to help you get started.

Shop around for the best rates and terms

When you’re ready to apply for a home equity loan, remember to:

– Shop around for the best rates and terms.

– Check your credit score and history. You may need to improve your credit before you can qualify for the best rates and terms.

– Know how much equity you have. This is the value of your home minus any outstanding mortgage debt.

– Consider a fixed-rate loan. With a fixed-rate loan, your interest rate will stay the same for the life of the loan.

– Choose a term that’s right for you. Home equity loans typically have shorter terms than first mortgages, so they may be repaid more quickly.

– Understand the fees associated with your loan. Home equity loans usually have closing costs, which can add to the overall cost of your loan.

Consider a HELOC instead of a home equity loan

Comparing a home equity loan vs line of credit, the biggest difference is how the money is received. A home equity loan gives borrowers a lump sum of cash up front that is then paid back over a fixed period of time, typically five to 15 years. A home equity line of credit (HELOC), on the other hand, acts more like a credit card. Borrowers are approved for a specific amount and given a credit line that they can tap into as needed. This allows homeowners to borrow only what they need at any given time, making interest payments only on the portion of the HELOC that is used.

Know the risks of a home equity loan

Many people take out home equity loans to make improvements on their home, but there are some risks involved. If you default on the loan, the lender can foreclose on your home. This means they will take possession of your home and sell it in order to recoup the money you owe them. You could also end up owing more money than your home is worth if the value of your home decreases.

Home equity loans can be a great way to finance improvements on your home, but it’s important to understand the risks involved. Be sure to talk to a financial advisor before taking out a loan to make sure it’s the right choice for you.