How Much Personal Loan Can I Get?

We all know that banks are different, and each has its own way of looking at things. So, how much personal loan can I get from each bank?

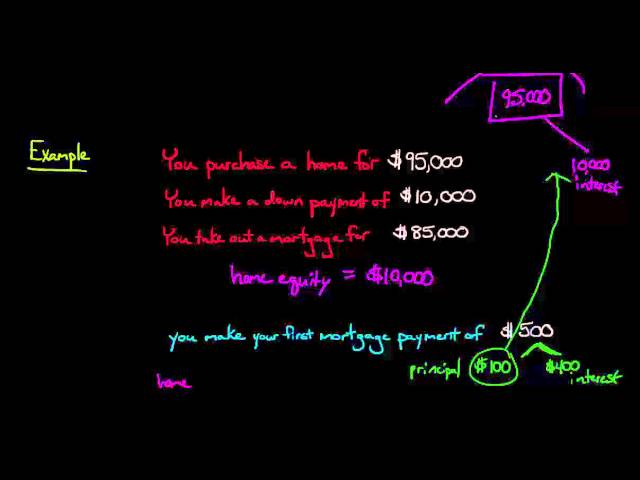

Checkout this video:

How Personal Loans Work

A personal loan is an unsecured loan that you can use for any purpose. You can use a personal loan to consolidate debt, finance a large purchase, or cover unexpected expenses. Personal loans have a fixed interest rate and a fixed monthly payment, so they’re easy to budget for. The biggest question when it comes to personal loans is how much you can borrow.

How interest rates are determined

Interest rates on personal loans vary depending on the individual lender, but there are some general trends that can provide some guidance. Personal loan interest rates tend to be lower than credit card rates, but higher than mortgage rates. The interest rate you’re offered will also depend on your credit score, income, and other factors.

Generally speaking, the higher your credit score, the lower the interest rate you’ll be offered on a personal loan. This is because lenders see borrowers with high credit scores as less of a risk. If you have a low credit score, you may still be able to get a personal loan from some lenders, but you’ll likely pay a higher interest rate.

Your income also plays a role in determining the interest rate you’ll be offered on a personal loan. Lenders want to make sure you’ll be able to repay your loan, so they take your income into account when determining your interest rate. If you have a higher income, you’re seen as less of a risk and may be offered a lower interest rate.

How personal loans are different from other types of loans

Personal loans are a type of loan that can be used for any purpose. Unlike other types of loans, such as auto loans and mortgages, personal loans are not secured by collateral. This means that if you default on the loan, the lender cannot seize your assets to repay the debt.

Personal loans are also different from other types of loans in that they are usually unsecured. This means that the lender does not require you to put up any collateral, such as your home or your car, to secure the loan.

Personal loans are generally given for a specific purpose, such as consolidating debt or making a large purchase. However, you can use the funds from a personal loan for any purpose you choose.

Personal loans come in two main types: fixed-rate and variable-rate. Fixed-rate personal loans have an interest rate that remains the same throughout the life of the loan. Variable-rate personal loans have an interest rate that can fluctuate over time.

How Much You Can Borrow

The amount you can borrow with a personal loan depends on a few factors, such as your credit score, income, and debts. Most personal loans range from $1,000 to $100,000, with the average loan being around $10,000. If you have a good credit score and a steady income, you may be able to qualify for a larger loan amount.

How your credit score affects your loan amount

Your credit score is one of the most important factors in getting approved for a loan and in determining your loan terms.

Generally, the higher your credit score, the lower the interest rate you’ll be offered by lenders. This could lead to significant savings over the life of your loan, so it’s important to understand how your credit score affects both your ability to get a loan and the terms you’re offered.

Here’s a general overview of how different credit scores can impact your loan amounts:

Excellent credit (720+) : You should be able to qualify for loans with competitive interest rates and terms.

Good credit (660-719) : You will likely qualify for loans with favorable interest rates and terms.

Average/fair credit (620-659) : You may still be able to get a personal loan, but you may have to pay higher interest rates and agree to less favorable terms.

Poor credit (580-619) : It may be more difficult to get approved for a personal loan, and if you are approved, you will probably have to pay higher interest rates and agree to less favorable terms.

Bad credit (300-579) : It can be very difficult to get approved for a personal loan if you have bad credit. If you are approved, you will likely have to pay extremely high interest rates and agree to very unfavorable terms.

How your income affects your loan amount

Your income is one of the main factors that lenders look at when determining how much money to lend you. Lenders want to make sure that you’ll be able to repay your loan, and they use your income as one way to gauge your ability to do so.

There’s no set rule for how much you can borrow, but generally speaking, the higher your income, the more money you’ll be able to borrow. This is because lenders feel confident that you’ll be able to make your loan payments if you have a high income.

Of course, there are other factors that lenders also look at when making lending decisions, such as your credit history and debt-to-income ratio. But if you have a high income, it’s likely that you’ll be able to borrow more money.

How your debts affect your loan amount

How your debts affect your loan amount

Your outstanding debts play a big role in how much you can borrow. Lenders use a debt-to-income ratio (DTI) to determine how much you can afford to pay each month, and ultimately, how much you can borrow.

The DTI is calculated by adding up all of your monthly debt payments and dividing them by your gross monthly income. For example, if your monthly debts are $1,000 and your monthly income is $4,000, your DTI would be 25%.

Most lenders prefer a DTI of 36% or less, but some may go as high as 50%. The lower your DTI, the better chance you have of being approved for a loan and getting a lower interest rate.

How to Get the Best Personal Loan Rate

When you’re looking for a personal loan, it’s important to compare personal loan rates from multiple lenders to ensure you’re getting the best deal. But how do you know what the best personal loan rate is? The answer may be different for each person, but there are some general things to keep in mind when you’re comparing personal loan rates.

How to improve your credit score

A good credit score is key to getting a great rate on a personal loan. Here are five tips to help you improve your credit score and get the best personal loan rate possible.

1. Check your credit report for errors.

2. Pay down your debts.

3. Limit your applications for new credit.

4. Build up a good payment history.

5. Get help from a credit counseling service if you need it.

How to compare personal loan rates

When comparing personal loan rates, it’s important to consider the amount of money you need to borrow, the repayment period, and whether you want a fixed or variable interest rate.

You should also compare personal loan rates from multiple lenders to ensure you’re getting the best deal possible. Keep in mind that the lowest personal loan rate may not always be the best deal, as some lenders may charge higher fees or require a higher credit score than others.

To compare personal loan rates, start by:

1. Checking your credit score: Your credit score is one of the factors lenders will consider when determining your personal loan rate. If you have a good credit score, you’re more likely to qualify for a lower interest rate.

2. Researching interest rates: Once you know your credit score, you can start researching personal loan interest rates from multiple lenders. Be sure to compare both fixed and variable Interest rates to find the best deal for you.

3. Calculating your monthly payment: Once you’ve found a few personal loan offers with competitive interest rates, use a personal loan calculator to estimate your monthly payments. This will help you compare loans and choose the one that fits your budget.

How to negotiate a personal loan rate

You don’t have to accept the first offer you receive on a personal loan. In fact, you shouldn’t. Just as you would when buying a car, it’s important to compare rates and terms from multiple lenders before deciding on a personal loan.

When you’re looking for a personal loan, your credit score will play a big role in the interest rate you’re offered. The higher your score, the lower your rate will be. If you have good or excellent credit, you should have no problem qualifying for a competitive rate. But if your credit is fair or poor, you’ll likely pay a higher interest rate.

That’s why it’s so important to compare rates from multiple lenders before accepting a personal loan. By shopping around, you could save hundreds or even thousands of dollars in interest over the life of your loan.

Once you’ve found a Personal Loan with a competitive interest rate, it’s time to start negotiating. Here are a few tips to keep in mind:

1) Get multiple quotes: As we mentioned above, it’s important to compare rates from multiple lenders before signing any loan agreement. This will give you leverage when negotiating with individual lenders.

2) Know your credit score: As we also mentioned above, your credit score has a big impact on the interest rate you’re offered on a Personal Loan. The higher your score, the more negotiating power you’ll have. Be sure to check your score and report for any errors before starting the Personal Loan process. You can get free copies of your credit report from AnnualCreditReport.com or by contacting one of the three major credit bureaus (Experian, TransUnion or Equifax).

3) Don’t be afraid to negotiate: Lenders expect borrowers to negotiate on Personal Loan rates and terms. It’s part of the process. So don’t be afraid to ask for a lower interest rate or better terms. Remember, the worst they can say is no!

4) Take your time: There’s no rush when it comes to taking out a Personal Loan. If one lender offers you an unfavorable rate or term, simply thank them for their time and move on to another lender who may be more willing to work with you.