How Much is the Minimum Payment on a Credit Card?

Contents

If you’re wondering how much the minimum payment is on a credit card, the answer may depend on your card issuer. Some credit card companies may require a minimum payment of 4% of your balance, while others may require a minimum payment of $25.

Checkout this video:

The Minimum Payment

What is the minimum payment?

The minimum payment is the lowest amount of money that you can pay on your credit card bill each month without being charged a fee. It is important to remember that making only the minimum payment will not reduce your debt, and it will take much longer to pay off your credit card this way. If you have a lot of debt, you may want to consider other options such as a debt consolidation loan.

How is the minimum payment calculated?

The minimum payment on your credit card is the least amount of money that you are required to pay towards your credit card balance each month. This minimum payment is usually a percentage of your total balance, and may also include any interest or fees that have accrued.

Your credit card issuer will typically set your minimum payment at around 2-5% of your total balance, but it can vary depending on your issuer and other factors. It’s important to remember that even if you make the minimum payment each month, it will take you much longer to pay off your balance in full and you will end up paying more in interest over time.

If you’re having trouble making your minimum payments, contact your credit card issuer as soon as possible to discuss your options. You may be able to negotiate a lower minimum payment, or set up a hardship program that will allow you to make smaller payments for a short period of time.

What are the consequences of making only the minimum payment?

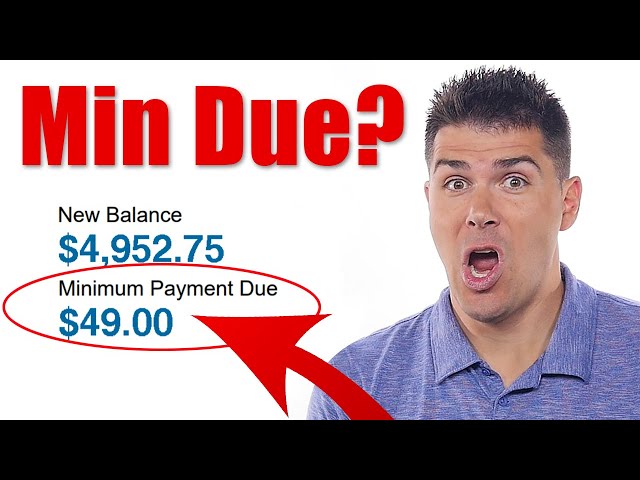

The minimum payment is the lowest amount you can pay on your credit card bill each month. By law, credit card issuers must include the minimum payment on your monthly statement.

The minimum payment may be a fixed amount, such as $25, or a percentage of your balance, such as 2%.

If you only make the minimum payment each month, it will take you longer to pay off your debt and you will end up paying more in interest. For example, if you have a $1,000 balance on your credit card with an 18% annual interest rate and you make the minimum payment of 2% each month, it will take you over 40 years to pay off the debt and you will end up paying more than $5,000 in interest.

If you are having trouble making more than the minimum payment each month, contact your credit card issuer to discuss your options. You may be able to negotiate a lower interest rate or set up a repayment plan.

The Minimum Payment and Interest

The minimum payment is the smallest amount you can pay on your credit card bill each month. Your credit card issuer will set a minimum payment based on your outstanding balance, annual percentage rate (APR), and other factors. By law, issuers must set the minimum payment at a level that will pay off your balance within a reasonable amount of time. For example, if you have a $1,000 balance and an APR of 15%, your minimum payment would be $25.

How does the minimum payment affect interest?

The minimum payment is the lowest amount you can pay on your credit card bill each month. Your credit card issuer will typically set your minimum payment at 2% of your balance, or $10 – whichever is greater.

Paying only the minimum amount each month will not pay off your debt quickly, and can end up costing you a lot in interest charges. In fact, if you make only minimum payments, you may never pay off your debt. That’s because the minimum payment is based on your outstanding balance, which changes every month as interest accrues. As a result, even if you make the same minimum payment each month, you will be paying less and less of your outstanding balance – and more of the payment will go towards paying interest charges.

Say you have a $3,000 balance on a credit card with an 18% annual percentage rate (APR). If your minimum payment is 2% of the balance, or $10 – whichever is greater, your minimum payment would be $60 ($3,000 x 0.02 = $60).

If you made only the minimum payments on this debt, it would take nearly 25 years to pay it off, and you would end up paying more than $6,700 in interest charges – that’s more than twice the original debt!

To avoid paying a lot of interest, it’s important to pay more than the minimum amount due each month. The more you can pay towards your outstanding balance each month, the less interest you will accrue and the quicker you will be able to pay off your debt.

What is the minimum payment if you want to avoid paying interest?

To avoid paying interest, you must make a minimum payment that includes both the interest charge and any required fees. Your credit card company must tell you the minimum payment due each month. The minimum payment is usually a percentage of your total balance, plus any fees. For example, if your balance is $1,000 and your monthly interest rate is 1%, your minimum payment would be $10 ($1,000 x 1% = $10).

The Minimum Payment and Your Credit Score

Your credit score is important. It’s a number that lenders look at to determine whether or not to give you a loan and at what interest rate. A high credit score means you’re a low-risk borrower, which equals a lower interest rate for you. A low credit score could lead to a higher interest rate and could mean you won’t be approved for a loan at all. So, what does your minimum payment have to do with your credit score?

How does the minimum payment affect your credit score?

Your credit score is a number that represents your creditworthiness. It is used by lenders to determine whether you are a good candidate for a loan and, if so, what interest rate they will charge you. Your credit score is also used by landlords, utility companies, and cell phone providers to determine whether to approve your application for service.

The higher your credit score, the better the terms of the loan or service you will be offered. A lower score may mean you will have to pay a higher interest rate or may not be approved for the loan or service at all.

One factor that is used to calculate your credit score is your payment history. This includes whether you have made your minimum payments on time. Making your minimum payment on time each month is important to maintaining a good credit score.

The minimum payment is the smallest amount of money you can pay on your credit card bill each month. The minimum payment is calculated as a percentage of your balance, typically 2-3%. For example, if your balance is $1,000 and the minimum payment is 3%, you would owe at least $30 each month.

If you only make the minimum payment each month, it will take you longer to pay off your debt and you will end up paying more in interest over time. However, making at least the minimum payment on time each month will help you maintain a good credit score.

What is the minimum payment if you want to avoid damaging your credit score?

The answer to this question depends on your situation and your credit score.

If you have a high credit score, you can afford to make a lower minimum payment without damaging your credit score.

However, if you have a low credit score, making a low minimum payment could damage your credit score. In this case, you would need to make a higher minimum payment in order to avoid damage to your credit score.

The Bottom Line

If you have credit card debt, you may be wondering how much you should pay each month to whittle down that balance. Unfortunately, there’s no one-size-fits-all answer to that question. The amount you should pay depends on several factors, including the interest rate on your card, the size of your debt, and your financial goals. However, there are some general guidelines you can follow to help you figure out how much to pay.

The pros and cons of making the minimum payment

There are pros and cons to making the minimum payment on a credit card. On the one hand, it can help you stay current on your debt and avoid late fees. On the other hand, it will take longer to pay off your debt if you only make the minimum payment, and you will end up paying more in interest over time.

If you are struggling to make ends meet, making the minimum payment may be the best option for you. But if you can swing it, paying more than the minimum each month will save you money in the long run.

When you should make more than the minimum payment

There are a few key scenarios where you should aim to pay more than the minimum payment on your credit card bill.

If you’re carrying a balance from month to month: You’ll want to focus on paying down your debt as quickly as possible to save on interest charges. Making the minimum payment each month will keep you in debt for a long time, so aim to pay at least double the minimum.

If you want to improve your credit score: Credit utilization is one of the key factors that determines your credit score. If you’re using a high percentage of your available credit, it can drag down your score. By paying more than the minimum each month, you can lower your credit utilization and give your score a boost.

If you’re trying to save money: It may seem counterintuitive, but making larger payments can actually save you money in the long run. The less interest you have to pay, the more money you’ll keep in your pocket. So, if you can afford it, paying more than the minimum each month is always the best choice.