How Much Does Collection Affect Credit Score?

Contents

Find out how much your collection account could affect your credit score, and get tips for dealing with collections.

Checkout this video:

The Basics of Credit Scores

What is a credit score?

A credit score is a number that represents your creditworthiness. It is based on information in your credit report, and it is used by lenders to decide whether to give you a loan and at what interest rate.

Your credit score is important because it can affect the interest rate you pay on a loan, and whether you are approved for a loan at all. A high credit score means you are a low-risk borrower, and will likely be offered a low interest rate on a loan. A low credit score means you are a high-risk borrower, and will likely be offered a high interest rate on a loan.

Your credit score can also affect your insurance rates – if you have a low credit score, you may be offered higher insurance rates than someone with a higher credit score.

There are many factors that go into calculating your credit score, including:

-Payment history: This includes whether you have made your payments on time, and how many times you have been late with payments.

-Credit utilization: This is the amount of debt you have compared to the amount of available credit. A high credit utilization ratio can hurt your score.

-Credit history: This is the length of time you have had accounts open and active. A longer credit history can help your score.

-Types of accounts: Having different types of accounts (such as revolving debt like credit cards, and installment debt like student loans) can help your score.

What is a collection?

A collection is a debt that has been placed with a third-party debt collector, typically because it has been unpaid for an extended period of time. When a collection agency contacts you about a debt, they will attempt to collect the full amount of the debt, plus any additional fees and interest. Collection agencies are regulated by state and federal law, and must follow certain rules when contacting consumers about debts.

Collection accounts can have a major negative impact on your credit score, so it’s important to understand how they work and what you can do to protect your credit.

What is a collection?

A collection is a debt that has been placed with a third-party debt collector, typically because it has been unpaid for an extended period of time. When a collection agency contacts you about a debt, they will attempt to collect the full amount of the debt, plus any additional fees and interest. Collection agencies are regulated by state and federal law, and must follow certain rules when contacting consumers about debts.

Collection accounts can have a major negative impact on your credit score, so it’s important to understand how they work and what you can do to protect your credit.

How Much Does Collection Affect Credit Score?

Collection can negatively affect your credit score, but the exact amount depends on a few different factors. One factor is how long ago the debt was incurred. If it just happened, it will have a bigger impact than if it happened a few years ago. Another factor is the type of debt.

Does a collection hurt your credit score?

A collection account on your credit report has the potential to significantly damage your credit score. Depending on the severity of the delinquency and the age of the debt, a collection could lower your score by as many as 100 points. The good news is, there are things you can do to mitigate the damage.

How Does a Collection Affect My Credit Score?

When you have a debt in collections, it’s reported to the credit bureaus as a delinquent account. This is one of the biggest factors that can drag down your credit score. The older the debt, the less impact it will have on your score—but even an old debt can be damaging if it’s for a large amount of money.

Collections also stay on your credit report for seven years, even after you’ve paid them off. So, if you have a collection that you’re trying to improve your credit score—you may just need to wait it out.

What Can I Do About a Collection on My Credit Report?

If you have a collection account on your credit report, there are a few things you can do to try to improve your credit score:

How long does a collection stay on your credit report?

According to Experian, one of the three major credit bureaus, a collection will stay on your credit report for seven years from the date of the original delinquency. This is the amount of time that creditors have to collect on delinquent debt.

What can you do to remove a collection from your credit report?

There are a few things you can do to remove a collection from your credit report. The first is to try to negotiate with the collection agency to have the debt removed in exchange for payment. This is often called a “pay for delete” agreement.

Another option is to dispute the debt with the credit bureau. You can do this by sending a letter to the bureau explaining why you believe the debt is not yours or is inaccurate.

If you are unable to get the debt removed from your credit report, you can try to improve your credit score by paying off other debts and maintaining a good payment history.

The Bottom Line

The impact of collections on your credit score depends on a few different factors, including how much you owe, the number of collections accounts you have and the type of collections accounts.

How to improve your credit score

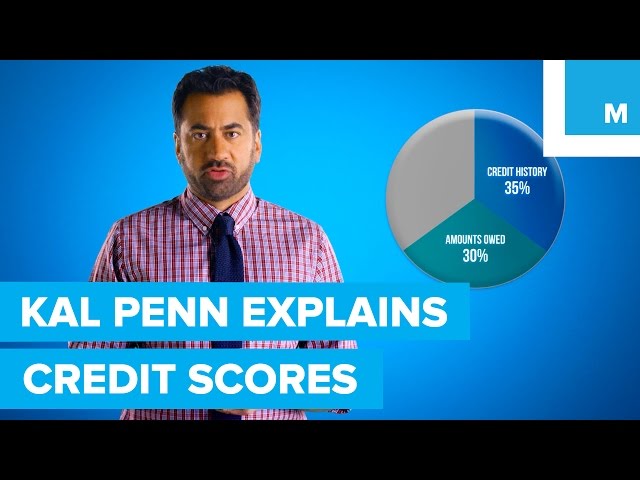

When it comes to your credit score, the biggest factor is your payment history – making up 35% of your FICO score. The second largest factor is credit utilization, which is your debt-to-credit ratio. This measures how much of your available credit you’re using and makes up 30% of your FICO score.

There are a number of other factors that make up your credit score, but these are the two main ones. So, if you’re looking to improve your credit score, the two best things you can do are to make sure you’re keeping up with your payments and to keep your debt-to-credit ratio low.